Recent Search

Popular Searches

.jpg?h=600&w=800&la=en&hash=C0F5CEE5D0E3E10A8570451CAC8EBFD4)

Source: Bloomberg, Emirates NBD Research

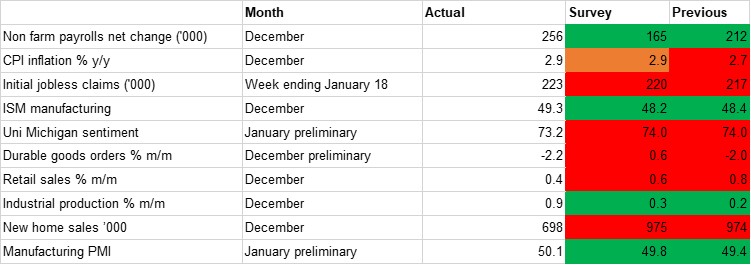

Source: Bloomberg, Emirates NBD ResearchOur macro scorecard for the US has more red than green this month in a suggestion that the US economy started to see some cooling at the close of 2024 and start of 2025, and indeed, the consensus forecast for the Q4 GDP print due tomorrow is for annualised q/q growth of 2.7%, down from 3.1% previously. Any slowdown this year will likely only be moderate however, and the IMF has recently revised up its 2025 growth forecast from 2.2% to 2.7%, down only modestly on the 2.8% estimated for last year.

Interestingly, it was the demand side indicators that were largely the weaker ones over the past month while data points related to production outperformed, bucking the trend of the past year or more where the reverse was more often the case. There is nothing in the data that appears indicative of a sharp slowdown in US activity, and with inflation ticking up modestly in recent prints we expect the FOMC to remain on hold at its first rate-setting meeting of the year today. Nevertheless, we still hold to our expectation of three 25bps cuts over the year as the Fed looks to move to a less restrictive policy stance.

There was a notable uptick in the results from manufacturing surveys over the past month, and the S&P Global manufacturing PMI survey turned positive in January, albeit marginally, as it came in at 50.1. This was the first expansionary reading for the index since June 2024. And while the ISM manufacturing survey was still in contractionary territory in December, it surprised to the upside at 49.3. This was the highest reading since March with new orders driving the improvement as the subcomponent rose to 52.5, up from 50.4 previously. Industrial production also saw a marked improvement as it expanded by 0.9% m/m in December, far greater than the predicted 0.2% gain, while November’s print was revised up to 0.2% growth from a 0.1% contraction initially. The December growth was the strongest expansion logged since February as the resolution of a strike at Boeing helped manufacturing see a 0.6% increase. Mining was up 1.8% and utilities 2.1%. Falling interest rates are likely contributing to the uptick in production over the past month or two, though there remain question marks over many of the Trump administration policies going forward.

On the other hand, there was a broad weakening in demand-side indicators over the past month, though that is on a relative basis and by and large the US consumer continues to look strong. Retail sales expanded by 0.4% m/m in December, down from 0.8% in November and missing the predicted 0.6% expansion, but this remains a fairly robust expansion and control-group sales expanded 0.7% m/m, the fastest advance in three months. Meanwhile, the University of Michigan sentiment index fell to 73.2 on the preliminary reading for January, down from 74.0 previously and was subsequently revised lower still, to 71.1. While the view on the current situation improved there was a notable worsening in expectations, perhaps reflecting uncertainty around upcoming tariff policies and their potential inflationary effects.

With regards inflation, there was further stalling in the disinflationary trend in December as y/y CPI inflation ticked up to 2.9%, from 2.7% previously, though this was in line with expectations. Other indicators also suggest mounting price pressures once again, with the prices paid subcomponent of the ISM survey accelerating to 52.5 in December, up from 50.3 in November, with these higher costs for businesses potentially passed on to consumers down the line. The University of Michigan survey showed that responders are already anticipating this as one-year ahead inflation expectations rose to 3.3% in January, up from 2.8% in the December survey.

On the other side of the Fed’s dual mandate, the labour market appears to still be in good health and while there have been complicating factors around recent NFP prints related to weather events and industrial action, the 256,000 net gain in December was a particularly strong reading. Job creation was still concentrated in the services sector so it remains to be seen if the recent improvement in production indicators translates into jobs, or indeed if President Trump’s policies specifically aimed at creating manufacturing jobs bear fruit. In any event, the case for the Fed cutting rates at its January meeting looks fairly weak.

Daniel Richards

Daniel Richards