Recent Search

Popular Searches

.jpg?la=en&h=600&w=800&hash=447CBCCE71EC4FEB08D481D44DAC8E7B)

Source: Bloomberg, Emirates NBD Research

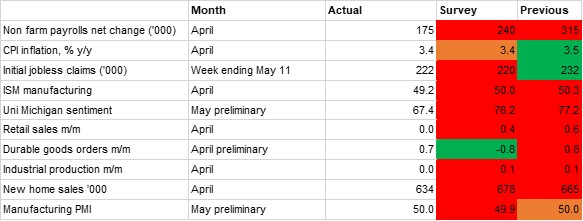

Source: Bloomberg, Emirates NBD ResearchThe past month has been a weaker one for US data releases, with our monthly macroeconomic scorecard almost completely red for data over the month to May 24, indicating both that data deteriorated on the previous month, and that it came in lower than the market consensus had predicted. That being said, the data has not yet indicated enough of a slowdown in either price growth or the labour market to see Fed officials soften their stance, and commentary over recent weeks has still tended towards the more hawkish side of the debate, citing a need to see a more sustainable softening in inflation before rate cutting can begin. As such, we maintain our expectation that the first rate cut from the FOMC will not come until September, with a total of two 25bps cuts pencilled in through the end of the year. The Fed kept rates on hold again at its early May meeting, with Jerome Powell indicating that rates were likely to be higher for longer given a ‘lack of further progress’ in bringing inflation down to target, and the messaging is little changed in the subsequent weeks.

There has been some progress on the inflation front, but it has remained stickier than expected and is still well above the target 2% level. Headline CPI slowed to 3.4% y/y in April, down from 3.5% in March and in line with expectations, and this marked the first slowdown in the measure since January. Core inflation, stripping out food and energy, was at 3.6% y/y, down from 3.8% previously, and 0.3% m/m, down from 0.4%. The Fed’s preferred measure of underlying inflation, PCE, was at 2.8% y/y in March, unchanged from the previous month but marginally higher than the predicted 2.7%. Notably, personal spending was up 0.5% m/m in March, faster than the predicted 0.3% rise, as consumer strength endured.

It does appear that that consumer strength could now be starting to ebb, as retail sales came in weaker than expected in April. Sales were flat on the previous month, considerably short of the predicted 0.4% gain and a significant slowdown from the 0.6% expansion realised in March. The core measure was an even weaker result, as stripping out automotives and petrol, sales were down 0.1% m/m, down from 0.7% in March and missing the predicted 0.2% growth. The slowdown was broad based across the categories, but a slowdown in online sales in particular suggests that the longstanding resilience of the US consumer could be starting to weaken.

There were other signs that high interest rates are taking their toll, as new home sales declined to 634,000 in April, down from 665,000 the previous months, while existing home sales are if anything even more sluggish this year as homeowners are reluctant to give up on low, and lengthy, fixed mortgage rates in the current high interest rate environment. Durable goods orders was a relative bright spot on the face of it, expanding 0.7% m/m in April according to the preliminary data. However, stripping out transportation the growth was a much weaker 0.1%, slower than the predicted 0.4%. March’s figure meanwhile was revised down to a flat 0.0%, from 0.2% on the initial print.

Perhaps the most significant slowdown in the data over the past month was the NFP report for April, which saw a net gain of just 175,000, missing the predicted 240,000, and down from 315,000 the previous month. This marked the softest monthly gain in jobs since March 2023, with a slowdown across key sectors including construction, leisure and hospitality, and government. Meanwhile, the March JOLTS report showed a fall in the number of job openings, to 8.5mn, from 8.8mn the previous month. However, while there is evidence of softening, there has yet to be severe enough deterioration in the labour market that would likely shift the Fed’s focus on the inflation side of its dual mandate to the other.

Daniel Richards

Daniel Richards