Recent Search

Popular Searches

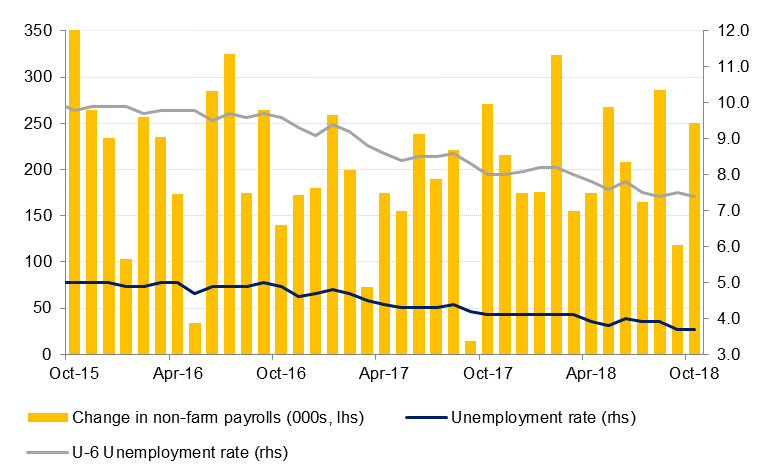

The US added 250k jobs in October according to the latest non-farm payrolls report, a sharp rebound from the 118k jobs added in September when Hurricane Florence disrupted the economy in south-eastern states. The unemployment rate is holding steady at 3.7%, the same level for past two months as more than 700k people entered the labour force. As the economy remains on a solid footing and more workers are drawn back into the labour force then we would expect the headline unemployment rate to be relatively steady or perhaps nudge upwards. Among the most positive signals from the NFP report was an increase in average hourly earnings to more than 3% year on year, the fastest level since April 2009. Overall the NFP should be more than enough to call a 25 bps increase in Fed rates this December as a done deal, even with an uncertain outlook for US politics following this week’s mid-term elections.

The Bank of England left policy on hold last week but cautioned that rates could be moving faster than the market currently expects. There was no dissension on keeping rates at 0.75% as there is still no clear outcome from Brexit negotiations. The bank’s MPC lowered its projections for growth in 2018 and 2019 despite an anticipated boost to growth from looser fiscal policy while it expects that inflation will be above the bank’s 2% target for the next several years, implying the bank could adopt a more hawkish trajectory for rates, particularly if a Brexit deal is achieved.

European data released at the end of last week was more negative. The final Eurozone manufacturing PMI for October fell to 52 compared with 53 a month earlier. The manufacturing data was the weakest since August of 2016 and may weigh on the composite figure due out later this week. There were few signs of an imminent turnaround in Eurozone manufacturing according to the PMI survey which showed that backlogs have been cut down while finished products increased for the first time since January.

US Treasury yields gained on the back of a strong NFP (see macro) and closed the week at 2.91% on the 2yr and back above 3.2% on the 10yr. The Fed meets later this week with no change in rates is expected but the strong jobs data have essentially cemented in a December move. We expect the market will increasingly be watching Fed commentary for any inkling that trade disputes are weighing on the outlook for the US economy. The 2yr-10yr spread widened on the back of the data, hitting 30bps as longer dated bonds saw more of a move.

Rising benchmark yields saw average yield on GCC bond index close higher at 4.68% even though credit spreads reduced by 2bps to 166bps.

Emaar Malls reported quarterly result reflecting 29% increase in revenue and 10% increase in profit in Q3 to AED 1.1 bn and AED 537 millions respectively which is unlikely to impact bond prices materially.

The dollar posted modest gains last week with the Dollar Index climbing 0.15% to close at 96.500. The index had reached a 2018 high of 97.200 on Wednesday, the highest level since June 2017, before surrendering these gains. Regardless of this the dip at the end of the week key technical levels have been breached. Analysis of the weekly candle chart shows that for a second week, the index has closed above the 200-week moving average (95.821). Since this key level had proven a vital resistance for the duration of Q3 2018, this is quite a noteworthy development. In the short term, further gains are likely if the index continues to close above this level. However, the US mid-term elections and the potential of a divided Congress can result in a reversal of the USD’s fortunes.

The move in US bond yields weighed on US equities with the major indices falling at the end of the week. The S&P 500 lost 0.6% while the Dow gave up more than 4%. The FTSE ended the day down 0.29%, likely on the back of shifting market expectations that the BoE will move sooner than anticipated.

Regional equities were largely negative to start the week. Both the DFM and Abu Dhabi exchanges closed lower while the Tadawul gave up 0.4%.

Benchmark oil futures fell for the fourth consecutive week, unwinding nearly all of the gains the market experienced from the end of August. Brent futures fell 6.2% to close at USD 72.83/b while WTI lost 6.6% to end the week at USD 63.14/b. On a year to date basis, Brent futures are up 8.9% since the start of 2018 compared with gains of nearly 30% ytd one month ago while WTI is now up just 4.5%ytd after having been up 26% a month ago.

At the end of the week the US state department indicated that it would be giving eight countries waivers from sanctions to continue importing crude from Iran. There has been no official list yet but the market is expecting that at least India, South Korea and possibly Turkey and Iraq will be exempt. Waivers will only last for 180 days and importers would still be expected to cut back on their lifting of Iranian barrels. US sanctions on Iran’s energy trade come into effect from November 5th and Iranian exports and production had been declining steadily in advance. Market surveys of Iranian exports show a decline of more than 1m b/d as of October from May, when the US withdrew from the JCPOA (the Iran nuclear deal).

Investors have surrendered on long positions in both Brent and WTI. Net length in both contracts has fallen five weeks in a row and is near their lowest in the last year. Bearish positions on Brent have been expanding, more than 24k shorts were added last week, while overall open interest in speculative WTI positions declined last week. With both curves threatening to stay in contango more longs could exit the market and add to selling pressure, a self-fulfilling trend that usually requires a significant shift in fundamentals in order to come to an end.

Edward Bell

Edward Bell