Recent Search

Popular Searches

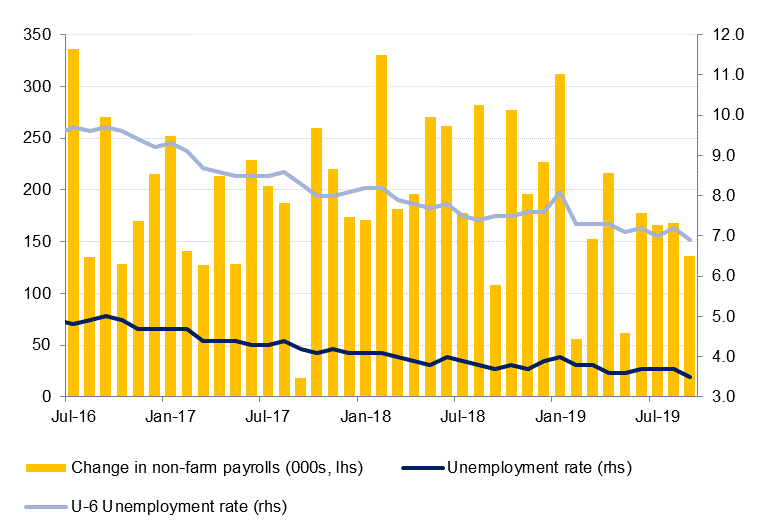

US payrolls data for June provided some relief for equity markets. While the figures indicated that growth was slowing in the US, they did not point to an imminent recession. Non-farm payrolls rose by 136k in September, lower than the 145k that the market had expected, but the August reading was revised higher to 168k from 130k previously. Encouragingly, the unemployment rate declined to a 50-year low of 3.5%. However, average hourly earnings growth was the slowest in fourteen months at 0% m/m and 2.9% y/y. The September jobs numbers partly offset disappointing manufacturing and services data that was released earlier last week. The minutes from the Fed’s last meeting will be released on Wednesday, and Chairman Powell and other members of the FOMC are all due to speak this week. The market will be closely watching these comments for clues about the timing of the Fed’s next rate cut, following the latest payrolls data. The market is pricing a 73% probability of a cut in October but the last DOT plot indicated a wide range of views among FOMC members about the future direction of monetary policy.

The Reserve Bank of India (RBI) cut repo rates by 25 bps to 5.15% at its meeting over the weekend. The latest cut takes the cumulative easing to 135 bps in 2019 with interest rates at the lowest level since May 2010. The central bank maintained an accommodative stance and indicated that it was willing to do ‘whatever it takes’ to revive growth. With inflation remaining benign and the RBI sharply lowering its GDP growth forecasts, we expect the central bank to continue to ease monetary policy further. The RBI lowered its GDP growth forecast for FY 2020 to 6.1% from 6.9% and Q1 FY 2021 growth forecast to 7.2% from 7.4%.

The value of Dubai’s non-oil foreign trade grew 5% y/y in H1 2019, with exports rising 17%. However re-export growth slowed sharply to 3% y/y, compared with 14% growth in H1 2018, likely reflecting the impact of increased tariffs and slower global growth on international trade. Non-oil imports to Dubai rose 4% in H1 2019 after contracting in 2018.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Fixed Income

Treasuries closed higher as economic data took a turn for worse. The non-ISM manufacturing index reading of 52.6 for September 2019 was the lowest since August 2016. However, a modest increase of 136k in non-farm payrolls data and unemployment rate dropping to 3.5% did soothe some of the early-week worries. Having said that, the market expectation of a another rate cut by the Federal Reserve at its next meeting in October increased to 72.9% from 42.9% at the end of last week.

Yields led by the front end dropped sharply with 2y UST, 5y UST and 10y UST yielding 1.40% (-23 bps w-o-w), 1.34% (-22 bps w-o-w) and 1.53% (-15 bps w-o-w) respectively.

Regional bonds closed higher. However, the move was much shallow compared to change in benchmark yields as sharp correction in oil prices weighed. Brent oil prices dropped -5.7% 5d. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped -2 bps w-o-w to 3.23% and credit spreads widened 15 bps w-o-w to 175 bps. The credit spreads are at the widest level since June 2019.

According to reports, Saudi Aramco is in talks with banks to refinance USD 2.2bn of debt held by its joint venture with Total. The company is seeking to lower interest rates on both SAR and USD borrowings.

FX

Over the last week, EURUSD gained 0.36% to close at 1.0979. Despite this move, the first gain in three weeks, the price remains below the 23.6% one-year Fibonacci retracement (1.1054) and 50-day moving average (1.1061). While the price remains below these levels, there is the risk of a retest of the 2019 low of 1.0879. It is also noteworthy that the increases of this week have taken the cross back above the supportive 23.6% five-year Fibonacci retracement (1.0942). Should there be a weekly close below this level, it may catalyze a more significant decline towards 1.05.

Finding support at the 23.6% one-year Fibonacci retracement (1.2295), GBPUSD rose by 0.34% last week, to close at 1.2333. Of technical significance is that throughout the week, support was found at the 50-day moving average (1.2252). While the price continues to close above this level on a daily basis, a test of the 100-day moving average (1.2429) remains a possibility.

Equities

Most regional equities started the week on a positive note following a rebound in global risk sentiment over the weekend. The DFM index (+0.7%) was led higher by strength in mid-cap stocks. Deyaar Development and Amlak Finance rallied +8.9% and +14.5% respectively. Arabtec was another major gainer after the company said it won a USD 75mn order from Saudi Aramco.

Commodities

Oil prices extended their losses last week as markets remain caught up in the negative sentiment affecting nearly all markets. Brent futures fell 5.7% last week to settle at USD 58.37/b while WTI closed down 5.5% at USD 52.81/b. Both contracts are now more than 3% below their pre-Aramco attack levels as markets have fixated on a poor outlook for the global economy and how it will feed into demand for oil.

Investors have continued to cut long oil positions with total net length in WTI declining by more than 60k lots last week, the largest single-week decline since August 2017. Demand concerns and a diminishing backwardation in the WTI curve are cutting the economic incentives to be long oil. The front of the WTI curve flattened significantly in the last fortnight, ending at USD 0.07/b in backwardation in the 1-2month spread.

Aditya Pugalia

Aditya Pugalia