Recent Search

Popular Searches

Producer prices in China slowed in December to a 13 month low of 4.9% y/y, compared with 5.8% a month earlier. Government efforts to crack down on excess industrial production in sectors like steel and aluminium has been weighing on demand for raw materials. A slowdown in China’s economy at the end of 2017 and to start 2018 has been widely expected as the government manages a transition to consumption-led growth. Consumer price growth edged up to 1.8% y/y from 1.7% previously, slower than the market had expected.

Job openings in the US for November fell for the second month in a row according to data out from the Labor department. The JOLTS survey measured 5.88m job openings and judging from the recent NFP data which showed a steady unemployment rate of 4.1% we would expect to see some levelling off of job openings in the US. The quits rate, a measure of workers voluntarily leaving their roles, stayed unchanged at 2.2% for the third consecutive month. Even as the labour market tightens a flat quits rate suggests workers aren’t confident that better wages can necessarily be found in new roles, taking some pressure off employers to raise salaires.

German industrial production rebounded by 3.4% m/m in November, following a 1.2% contraction the previous month and surpassing market expectations for a 1.8% increase. This figure helped take up annual growth to 5.6% compared with 2.8% the previous month. In addition, the German Federal Statistical Office confirmed the survey optimism of exports, with exports increasing 4.1% m/m in November compared to market consensus for 1.2% growth, while imports grew by 2.3%. This helped widen Germany’s trade surplus to EUR 23.7bn form EUR 18.9bn the previous month.

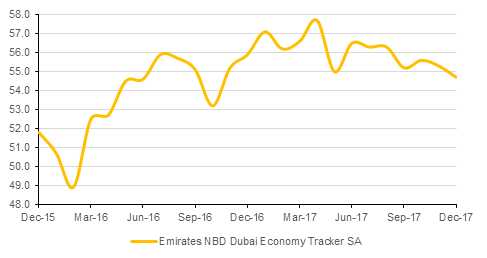

The Dubai Economy Tracker Index slipped to a 14-month low in December on weaker output growth. However, on an annual basis, the data indicates that Dubai’s economy grew faster in 2017 than the previous two years. Although business activity and new orders saw strong growth last year, employment gains were the weakest in the survey history. Separately, an official at the UAE’s ministry of economy said he expected growth to accelerate to 3.9% in 2018, higher than our own 3.4% forecast for this year.

Source: Emirates NBD Research

Source: Emirates NBD Research

US Treasuries closed lower as the turn of the year is marked by newer supply across Europe, Asia and the US. However, much of the impact was on the long end of the curve with yield on the 30y USTs rising 8 bps to 2.89%. The move on the short end was more subdued with yield on 2y USTs rising 1 bps to 1.96% and 5 bps on 5y USTs to 2.33%.

The move in benchmark yield had limited impact on regional bonds with YTW on the Bloomberg Barclays GCC Credit and High Yield index rising 1 bps to 3.73% and credit spreads tightening by 3 bps to 144 bps.

Despite constructive data out of Germany (see marco), the Euro underperformed against most of the other major currencies on Tuesday with EURUSD falling for a third consecutive day. Despite these declines, the daily uptrend remains intact and strong support near the 50 and 100 day moving averages (1.1821 and 1.1829 respectively) are likely to limit further declines. However, should there be a break of this level, a decline towards 1.1705 (the 76.4% one year Fibonacci retracement) cannot be ruled out.

JPY was Tuesday’s outperformer, gaining after the Bank of Japans weekly bond purchases cast doubts over the longervity of lose monetary policy. The BOJ reduced its puchases of debt maturing in 10-25 and over 25 years triggering speculation that tapering may come sooner than anticipated.

Developed market equities continued their positive run as investors remain optimistic over the upcoming earnings season. The continued rise in commodity prices also helped investor sentiment. The S&P 500 index and the Euro Stoxx 600 index added +0.1% and +0.4% respectively.

Regional stocks were mixed with the Tadawul closing -0.3% lower following renewed speculation over domestic politics. Elsewhere, the Qatar Exchange gained +0.3% to close above 9,000 levels for the first time since August 2017. In terms of stocks, Emaar Development gained +1.8% to continue its rally since the start of 2018.

Oil prices continued their march upward overnight, putting Brent futures within sight of USD 70/b. WTI gained nearly 2% on the day and Brent added 1.5% despite an estimate from the US government’s EIA that oil production there would exceed 10m b/d as early as next month. The US last produced 10m b/d in 1970 and an extremely comfortable pricing and hedging environment should allow US oil and gas companies to continue investing and see higher output.

Market structures for both Brent and WTI are holding onto what look to be confident positions, with the backwardation in WTI at nearly USD 0.10/b and in Brent holding onto USD 0.5/b.

Edward Bell

Edward Bell