Recent Search

Popular Searches

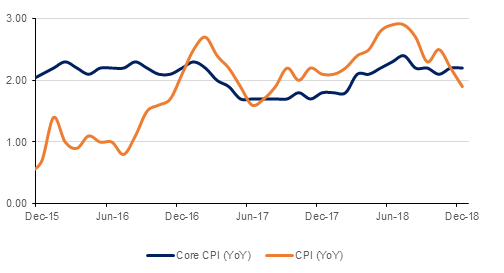

U.S. inflation eased in December according to a report from the Bureau of Labor Statistics which showed that while core inflation remained at 2.2% y/y, headline inflation crawled back to 1.9%y/y compared with 2.2% the previous month. With the FOMC minutes revealing that policy makers were eager to take a patient and data dependent approach to adjusting monetary policy, this fall back in inflation below the central bank’s 2% target, accompanied by pull backs in PMIs have lowered market expectations for further rate hikes in 2019. Currently the markets are relatively evenly balanced as to whether there will be a hike or a cut in U.S. interest rates by the end of the year.

In the UK, production fell yet again in November, with industrial production showing a 0.4% m/m decline, following October’s 0.5% decline and manufacturing production falling 0.3% m/m following October’s 0.6% contraction. However, GDP accelerated to 0.2% m/m in November, up from 0.1%. Investors have largely overlooked the economic data, however, instead focusing their attention on Brexit developments, the latest being mounting conjecture that the UK departure from the EU is likely to get delayed should Theresa May lose the vote on her Brexit deal on Tuesday, and with EU officials thought to be open to a 3 months extension to the Brexit schedule. The pound has rallied ahead of the vote and with Theresa May now claiming that no Brexit is more likely than no deal, hedge funds are apparently throwing in the towel on short GBP positions.

On a more positive note, equity and commodity markets performed well for most of the second week of 2019, the S&P GSCI Index posting a 4.17% gain over the week while the MSCI World Index recorded a 2.78% gain. Corporate earnings results will now becoming of increasing significance from this week onwards, especially as the U.S. economic data calendar will remain negatively affected by the government shutdown. Meanwhile any developments regarding the US-China trade dispute will also be closely watched.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

The UST curve shifted slightly higher last week despite dovish comments from Fed officials. Positive trade talks with China and inflation data reflecting core CPI at above the 2% mark build the case for higher UST yields. Yields on the 2y USTs, 5y USTs and 10y USTs closed at 2.54% (+5 bps w-o-w), 2.53% (+3 bps w-o-w) and 2.70% (+4 bps w-o-w) respectively.

Notwithstanding the higher UST benchmark yields, GCC bonds received a boost from tightening credit spreads on the back of rising oil prices. The YTW on the Bloomberg Barclays GCC Credit and High Yield index dropped -4 bps w-o-w to 4.58% and credit spreads tightened 10 bps to 200 bps.

The primary market got off to a solid start with Saudi Arabia raising USD 7.5bn in two tranches including region’s first bond maturing beyond 2050. The pipeline looks strong with Dubai Islamic Bank and Al Hilal Bank expected to price in the near term.

Over the last week, EURUSD posted a 0.65% gain to close at 1.1469. Over the course of the week, the cross was able to break above the 100-day moving average (1.1475) and reach highs of 1.1570 on Thursday, before paring its gains on Friday. In the week ahead additional breaks of the 100-day moving average are likely to result in further gains towards the 23.6% one-year Fibonacci retracement (1.1532).

GBPUSD climbed by 0.92% last week to close at 1.2840 on Friday. The move has resulted in a firm break of the 50-day moving average (1.2764) for the first time since November 2018. While the price stays above this level, the next move is likely to be within the 1.2893-1.2898 zone which includes both the 100-day moving average and the 23.6% one year Fibonacci retracement.

USDJPY was almost unchanged last week, posting a 0.02% rise and closing at 108.53. This is the third consecutive weekly close of below the 50-week moving average (110.25). However, once again, support was found at the 38.2% one year Fibonacci retracement (108.38). While this level continues to provide support, a reprieve for USDJPY is likely.

Regional markets closed mixed amid strength in Saudi Arabian and Egyptian equities and weakness in Dubai stocks. Aramex dropped -1.5% after the company said it acquired Saudi TAL for Commerce & Contract Co for about USD 80mn. Emaar Malls was another notable loser with losses of -3.4%.

Oil prices continued their positive run with Brent and WTI contracts rising +6.0% 5d and +7.6% 5d to close above key levels of USD 60/bbl and USD 50/bbl respectively.

Saudi Arabia’s oil minister said that he remains confident that the cuts initiated by OPEC+ will help to balance the market. He added that the group will work towards curbing the volatility in oil prices. The UAE Energy Minister also expressed similar sentiment and said that ‘we will do whatever is right decision to balance market’.