Recent Search

Popular Searches

Saudi Arabia's state budget deficit shrank 9.5% from a year earlier in the third quarter of 2017, as the government sticks to meeting its full-year target for strengthening its finances. Revenue climbed 11% to 142.1 billion riyals in the quarter while spending increased 5% to 190.9 billion riyals. Non-oil revenue jumped 80% year-on-year to 47.8 billion riyals in the third quarter, with some of the gains probably attrricbuted to government taxes on tobacco and sugary drinks applied in June.

Markets have been focused on developments around the ability of US Republicans to pass legislation on tax cuts, in what would be the biggest tax-code overhaul since 1986. The House of Represenatives approved a broad package of cuts, shifting the debate to the Senate, where passing the legislation is looking more tricky as Republicans currently have only a 52-48 majority. Republicans have long promised tax cuts and see them as critical to retaining power in the November 2018 elections. However Republicans can lose no more than two votes, if Democrats remain united in opposition. Four Republican Senators are rumoured to be opposing the cuts, over issue ranging from the ballooning deficit to tax deductions.Should those Senators vote against it, this would be more than enough to derail to proposals, making it a barren first year for President Trump, with no significant campaign promise delivered.

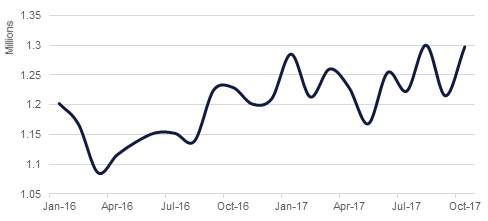

US Industrial Production hit a six month high of 0.9% in October. Industrial Production has seen activity weighed on over the last two months, impacted by both Hurricanes Irma and Harvey. US Housing Starts rebounded to one year highs in October, also suffering from Hurricane induced falls in the previous month. New housing starts climbed 13.7% in October from the prior month to a annulaized rate of 1.29mn units, as rebuilding activity contributes to an already robust pre-hurricane housing market.

Moody’s upgraded India’s long term sovereign rating to Baa2 from Baa3 and changed outlook on the rating to stable from positive. The last rating upgrade for India was in 2004. The rating agency attributed the upgrade to – 1. Reforms by the government to strengthen institutional framework, 2. Government’s support to public sector banks and 3. Government’s adherence to fiscal deficit framework. The rating action confirms our view that India remains one of the bright spots within emerging markets. Having said that, near term concerns do remain over low credit offtake, rising inflation trajectory and stabilization of the GST system.

Source: EIKON, Emirates NBD Research

Source: EIKON, Emirates NBD Research

US treasury curve continued its flattening trend with the gap between the longer-term and shorter-term yields narrowing further during the week. Yields on 2yr, 10yr and 30yr closed the week at 1.72% (+4bps), 2.34% (-6bps) and 2.78% (-9bps) respectively. 2yr10yr spread is now at 62bps, its lowest level since the financial crisis of 2008/2009.

GCC bonds were mostly stable as investors sat on the sidelines, having little catalyst to induce trading. In line with lower longer term UST benchmark yields, the Barclays GCC index closed the week at average yield of 3.55% (-2bps) on unchanged credit spreads at 138bps.

EA Partners I and EA Partners II said they expect to pay December bond coupons if non-defaulted companies keep contributing to the liquidity pool that funds the interest payments. In response, EAPART 20s rose more than a point in price to $74.52 and yield of 18.58% (-61bps). Last month, Fitch had downgraded EAPART bonds to CC, merely two notches above default.

UK Court upheld the legality of the contracts in the Dana Gas sukuk case, though final judgement on the issue and further clarity will take more time until the UAE court has had the hearing on 25th December. Holders of DANAGS sukuk were comforted with the defaulted DANAGS 9% rising five points toc lsoe the week at $82.62, yield of 10.89% (-75bps).

The dollar fell last week as global equities unwound, with anxiety over political events dominating sentiment. The coming week will be a holiday shortened one in the US, with Thanksgiving approaching on Thursday, leaving markets to ponder the possibility of tax reform being passed before the end of the year.

The Bloomberg Dollar index dropped -0.8% last week with safe haven currencies such as the JPY (+1.28% 5d) and the CHF (+0.7% 5d) outperforming.

Regional equity markets started the week on a negative note as political developments continued to remain an overhang. The DFM index and the Tadawul dropped -1.1% and –0.6% respectively.

In terms of stocks, real estate stocks dragged the DFM lower while banking sector stocks on the Tadawul continued to outperform the broader index. Emaar Properties dropped -1.2% while Al Rajhi gained +1.3%.

Oil prices rebounded the at the end of last week following comments from Saudi Arabia’s Energy Minister Khalid Al Falih that OPEC should announce an extension of the cuts at its next meeting scheduled for end of November 2017. This is in contrast to reports that Russia is hesitant to commit to cuts so soon preferring to wait closer to the deal expiration at the end of March 2018. The Brent and WTI gained +2.2% and +2.6% to pare weekly losses to -0.3% and -1.3% respectively.