Recent Search

Popular Searches

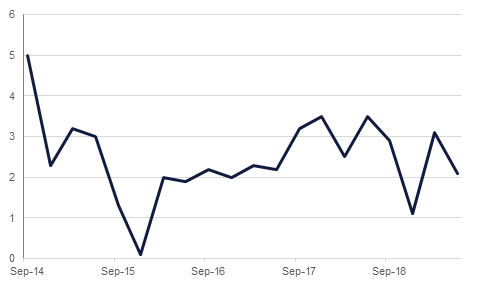

.jpg?la=en&h=457&w=800&hash=F7AEDE2C5F0D5D38E572AD6F04022F36)

The global turn towards more dovish monetary policy was confirmed over the weekend, following a number of central bank meetings and US growth data which indicated a slowing economy. The Q2 growth print came in at 2.1% y/y, and while this exceeded expectations of 1.8%, it was markedly slower than the 3.1% seen in Q1. Private consumption growth held up well at 4.1%, but non-residential investment declined by -0.6%, perhaps an indication that trade tensions are weighing on sentiment. In light of this slowdown, a rate cut at the upcoming Fed meeting this week appears all but guaranteed. However, the fact that growth moderately exceeded expectations makes a 25bps cut the most likely scenario, rather than the potential 50bps that some observers had been hoping for. US representatives Robert Lighthizer and Steven Mnuchin are in China for talks today.

In Europe, the ECB meeting on Thursday confirmed expectations of a more dovish turn, albeit one not yet implemented. The central bank left rates on hold, but boss Mario Draghi painted a gloomy picture with regards to growth, and hinted heavily towards looser policy hereafter, saying that interest rates were ‘to remain at present or lower levels at least through the first half of 2020.’ A resumption of quantitative easing is also back on the table. The next decision is scheduled for September, and with data out of Europe increasingly weak, Draghi will likely implement some proactive policy for his last meeting in charge.

It is not only developed markets that are loosening policy; a couple of major EMs cut rates at the close of the week also. In Turkey, the TCMB cut rates by 425 basis points on Thursday, under new governor Murat Uysal’s first meeting in charge. This exceeded consensus predictions of 250 bps of cuts, and met with approval by Turkish President Recep Tayyip Erdogan – although the president did call for still further cuts. In Russia meanwhile, the central bank cut rates from 7.50% to 7.25%, and signalled further rate cuts to come.

Central banks will remain in the spotlight over the next week, as aside from the Fed there are also upcoming decisions from the Bank of Japan, the Bank of England, and the Central Bank of Brazil.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Economic data in the US was generally better than expected, pointing to GDP growth remaining well above 2% in the last quarter. Consequently, the UST yield curve shifted slightly upwards even though the chance of a rate cut at FOMC’s meeting on 31st July remains intact at 100%. Yield on 2yr, 5yr and 10yr US treasuries closed the week at 1.85% (+4bps), 1.85% (+4bps) and 2.07% (+2bps) respectively. Across the pond, the dovish ECB meeting last week pushed European sovereign bonds higher with yield on 10yr Bunds and Gilts declining 3bps to -0.38% and 2bps to 0.69% respectively. Solid quarterly result announcement supported credit default protection costs to remain low with 5yr CDS levels on US IG and Euro Main closing the week lower at 51bps (-3bps) and 47bps (-2bps) respectively. Oil prices during the week were largely unchanged at around USD 63 / b.

Against this backdrop, GCC bonds had a constructive week. With more than USD 13 trillion worth of global bonds trading at negative yields, emerging market bonds are benefiting from investors’ hunt for yield. Adding to the bid ensuing from index inclusion, bid for GCC bonds was high facilitating average yield on Bloomberg Barclays GCC bond index to drop 4bps to 3.40% last week as credit spreads tightened 9bps to 143bps.

Oman raised USD 3bn in two tranches of bonds. The tranch maturing in 2025 (USD 750mn) was priced at 4.95% while the tranch (USD 2.25bn) maturing in 2029 was priced at 6%. The size of the order book was more than USD 9.25bn.

The dollar rose on Friday, supported by slightly firmer than expected U.S. GDP data. Comments from White House adviser Kudlow, that the U.S. would not intervene to depress the USD also helped to underpin it. Cable meanwhile, fell to 27-month lows below 1.24 on renewed concerns about the possibility of a no-deal Brexit. EURUSD also gave back gains that followed the ECB meeting on Thursday.

Regional equities closed largely lower amid weak corporate earnings. The DFM index and the Qatar Exchange lost -0.2% and -0.6% respectively.

Sabic closed lower after the company reported a sharp decline in Q2 2019 net profit to SAR 2.12bn compared to SAR 6.7bn last year. The company said that new capacities in key product lines that pressured product prices and margins in H1 2019 are expected to continue in H2 2019 as well.

Oil prices showed relatively little change last week as fundamentals and policy from agencies such as OPEC+ kept to the sidelines. Brent futures managed a gain of 1.6% over the week, closing just shy of USD 63.50/b, while WTI added a little more than 1% to end the week at USD 56.20/b. The front-end of the Brent curve stood out in weakening considerably last week with 1-2 month time spreads closing at just USD 0.09/b in backwardation, their lowest weekly close since early March.

Investors unwound some of last week’s build in net length thanks to new short positions added in both Brent and WTI. Net length in Brent futures and options fell more than 24k contracts while net long WTI positions declined by 28.8k lots.

Daniel Richards

Daniel Richards