Recent Search

Popular Searches

US President Donald Trump agreed to reopen the government after signing a deal to keep operations running until mid-February despite not winning any concessions from Democrats to finance his US-Mexico border wall project. Coming only a few days after a White House adviser indicated the shutdown would mean no growth in Q1, the overall impact of the government shutdown should be relatively muted. The reopening of the government hasn’t eliminated tension between the President and Congress and there is a risk that no spending bill can be agreed upon by mid-February, resulting in another government shutdown. However, public sentiment appeared strongly against the president in relation to the shutdown and Trump may be wary of using the same tactics again. The resumption of government services will allow for data to published once again, providing markets with a clearer understanding of the performance of the US economy.

The ECB cautioned on the outlook for monetary policy in the Eurozone as economic indicators point to more softness ahead. The ECB’s statement at the end of last week indicated it would keep rates unchanged until at least Q3 and in the press conference following the monetary policy decision, ECB policymakers said that any withdrawal of monetary stimulus would be ‘progressive’ and depend on the performance of the economy. ECB governor Mario Draghi appeared to accept the market’s view that rate hikes wouldn’t happen this year and could be delayed until 2020.

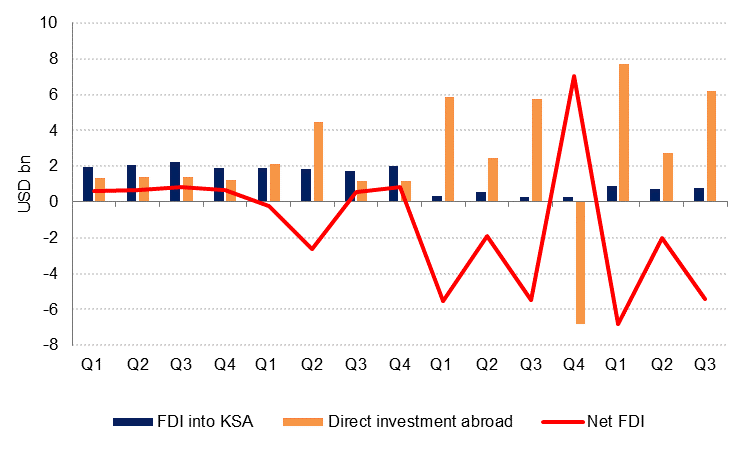

Saudi Arabia is expected to launch a new industrial development project on Monday. Around SAR 200bn (USD 53bn) worth of projects could be announced today, focused on boosting growth in industry, mining, energy and logistics. This would be the first phase of a 10-year programme totalling SAR 1.6trn (USD 427bn) of investment. The projects will involve both foreign and domestic private sector investment as well as public funds. Inward FDI to the Kingdom did rise in 2018, but was dwarfed by outflows of FDI and Saudi entities acquired assets abroad, resulting a new outflow of FDI for most of last year.

Source: Haver, Emirates NBD Research.

Source: Haver, Emirates NBD Research.

Treasuries ended the week higher. However, it pared some of its gains after an agreement was reached to temporarily reopen the US government. Yields on the 2y UST, 5y UST and 10y UST closed at 2.60% (-1 bps w-o-w), 2.60% (-2 bps w-o-w) and 2.76% (-2 bps w-o-w) respectively.

Ahead of the Federal Reserve meeting, there were reports over the weekend that suggested that policymakers are weighing earlier than expected end to the Balance Sheet wind down.

Regional bonds continued their positive run as they benefitted from subdued moves in benchmark yields and continued technical inflow from inclusion of bonds in the JP Morgan EM index. The YTW on the Bloomberg Barclays GCC Credit and High Yield index dropped -6 bps w-o-w to 4.46% and credit spreads tightened 4 bps w-o-w to 183 bps.

There were comments from the Saudi Finance Minister that the Kingdom may issue non-USD bonds this year.

GBP gained sharply over the course of last week as markets priced in more expectation that parliament would have greater control over Brexit and potentially rule out a no-deal outcome. Sterling closed the week above 1.32, its highest level since October last year. The Euro also managed a week of gains as the ECB’s patience on policy was largely expected.

The lack of a final agreement between the US Congress and President Trump over a comprehensive spending bill has kept the dollar on the back foot. The broader DXY index lost 0.56% over the week.

Regional equity markets made a mixed start to the week as earnings dominated flows. Zain Saudi traded higher after the company reported 2018 net profit of SAR 332mn relative to consensus expectations of a loss. Elsewhere, the DFM index was dragged higher by strength in market heavyweights. All Emaar-related names closed higher.

Commodities

Crude oil futures declined last week, their first weekly loss in 2019 after three consecutive gains. Brent futures fell 1.69% to close the week at USD 61.64/b while WTI was marginally down (-0.2%) at USD 53.69/b. Both contracts managed to gain in the final day of trading as the political crisis in Venezuela escalated and pressure on the Maduro government increases. There is as of yet no apparent direct impact on flows of crude out of Venezuela; production there had fallen so precipitously in the past two years that markets have been pricing in steady declines in output so the increased political risk is having only a limited impact.

Forward curves lost some strength last week. The 1-2 month spread in Brent futures ended the week in a backwardation of just USD 0.05/b having started the week closer to USD 0.2/b in backwardation. The Venezuela news helped to compress the contango in the WTI curve though; the 1-2 month spread closed at USD 0.29/b after having dipped to USD 0.44/b mid-week. Longer-dated spreads also weakened; the Dec 18/19 spreads in both WTI and Brent are in backwardation but they fell over the course of last week.

Click here to Download Full article

Edward Bell

Edward Bell