Recent Search

Popular Searches

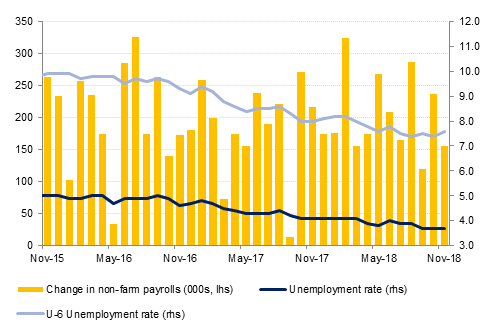

.jpg?la=en&h=457&w=800&hash=3592918562581DA0BA23DB47DFC1A3E3)

November’s U.S. nonfarm payrolls were softer than expected on Friday, showing that 155,000 new jobs were added in November, compared with expectations for 200,000.

This weaker than expected reading was accompanied by a downward revision to October’s headline from 250,000 jobs to 237,000 jobs. This slowdown in job growth however was also accompanied by evidence of continued wage pressures. Hourly earnings remained at 3.1% y/y and as a result, the Federal Reserve is still expected to raise interest rates at their December meeting. However, with this outcome already priced in, the market will be looking for cues on the expected rate of tightening in 2019, with any hints of a slowdown likely to result in further dollar weakness. Overnight Japanese GDP growth in Q3 was revised lower to -0.6% q/q and to -2.5% on an annualised basis, hurt by a big fall in business spending as well as by a series of natural disaster. Going forward any recovery may be hampered by the US-China trade tensions.

The OPEC agreement to cut oil production over the weekend, was clearly more than the markets were expecting, with crude oil prices rallying 5% on the week. OPEC and its partners, most critically Russia, will cut production by 1.2m b/d for six months, with OPEC countries taking 0.8m b/d of the cuts. The agreement effectively unwinds the increase in production that OPEC instituted at its last meeting in May. Since then production has increased steadily from producers that had the capacity to do so—Saudi Arabia, the UAE, Iraq and Russia.

In the coming week the highlight will be the UK Parliament’s vote on Theresa’s May’s Brexit agreement with the EU on Tuesday. The chances of it being passed on the first attempt are very low, so it will be the scale of any defeat that will matter to markets. This morning there are reports that May could actually postpone the vote amidst rumours that she has made an emergency call to EU Council President Donald Tusk to discuss options.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

Treasuries ended the week sharply higher amid a sharp sell-off in risk assets and paring back of rate hike expectations in the US. The market is currently pricing only one rate hike in 2019 compared to three in Federal Reserve’s dot plot from last meeting. Yields on the 2y UST, 5y UST and 10y UST ended the week at 2.71% (-7 bps w-o-w), 2.68% (-13 bps w-o-w) and 2.84% (-14 bps w-o-w).

Regional bonds benefitted from the move in benchmark yields. The YTW on the Bloomberg Barclays GCC Credit and High Yield index dropped -9 bps w-o-w to 4.63% while credit spreads widened +5 bps w-o-w to 191 bps.

S&P revised its outlook on Qatar to stable from negative and affirmed the ratings at AA-. The rating agency expects economic growth to accelerate and external accounts to remain in surplus from 2018-2021.

Commercial Bank of Qatar raised USD 750mn from a syndicated loan to refinance and for general funding requirements. The three-year senior unsecured term-loan facility paid a margin of 100 bps over Libor.

EURUSD rose by 0.64% last week, closing at 1.1390 on Friday. Of note is that throughout the week, gains were continually kept in check by the 50-day moving average (1.1416), while for a 6th consecutive week, support was found at the 200-week moving average (1.1313).

USDJPY declined by 0.77% over the last five days to close at 112.70. Over the course of the week, the price broke below the formerly supporting 50-day moving average (113.07) which is now acting as a resistance level. Further declines during the week here halted when a new support level was found at the 100-day moving average (112.27).

Last week’s 0.17% decline took GBPUSD to 1.2728, a level at which the price is vulnerable to further losses. A break and daily close below the one year low of 1.2659 is likely to expose the cross to further declines towards 1.25, a level which remains our short term forecast.

Regional markets started the week on a negative note amid weak cues from developed markets over the weekend. The DFM index lost -1.2% amid continued weakness in market heavyweights. Elsewhere, Egyptian equities remained under pressure. Sodic announced a settlement of EGP 800mn with the government over a dispute involving one of its subsidiaries. Medinet Nasr said in a statement that the settlement will have no impact on the company and that it still remains interested in deal with Sodic.

OPEC+’s decision to cut output by 1.2m b/d help reverse crude futures persistent decline last week. WTI added 3.3% over the week while Brent gained more than 5%, with much of the gains coming on Friday. The gains so far haven’t been enough to affect the forward curve for either contract, both of which remain in contango. The cuts will take effect in January but there had previously been indicators from Saudi Arabia and other producers that they would cut exports this month on lower demand from refiners, helping to keep a near term bid under crude prices.