Recent Search

Popular Searches

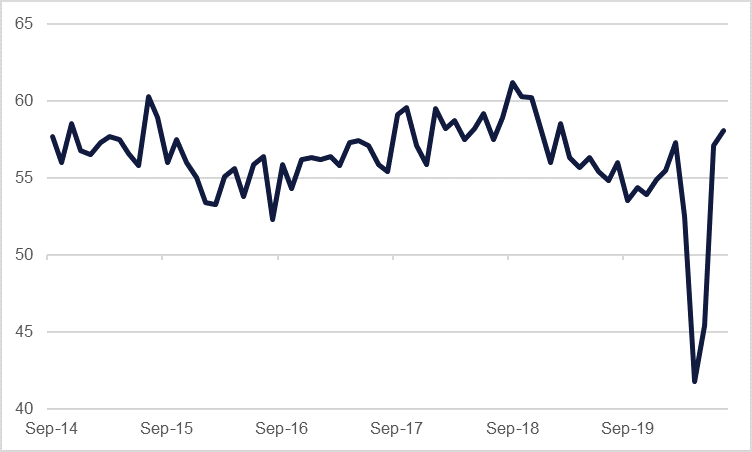

Following on from the strong manufacturing survey earlier in the week, the ISM services PMI released yesterday also exceeded expectations in July, coming in at 58.1, compared to consensus of 55.0 and up from June’s 57.1. New orders hit a series high of 67.7, up from 61.6 in June. Indications suggest, however, that while business is starting to pick up, firms remain wary of the risk to profits in a new operating environment, and this is reflected in the employment sub-index, which fell deeper into contractionary territory at 42.1, from 43.1 the previous month. In this environment, the disappointing ADP employment report released yesterday fits the pattern, as the 167,000 increase in private payrolls was far off the consensus estimate of 1.2mn. Whether or not this will chime with the official non-farm payroll report due this week, these indicators do suggest that there remains a residual risk to US consumer demand, especially following on from two consecutive weekly rises in initial jobless claims.

In Europe retail sales disappointed in June, expanding by 5.7% m/m and missing consensus estimates of 6.1%. May’s figure was revised up to 20.3% however, from 17.8% previously, and the y/y growth figure for June was also positive, at 1.3%.

There have been pledges of support for Lebanon in the wake of the huge explosion which destroyed parts of Beirut this week. The World Bank has said that it stands ready to help, the UK has pledged GBP 5mn, Denmark DKK 12mn, and many countries have promised food and emergency assistance. The city’s governor has warned that the devastation caused by the disaster may cause collective losses of as much as USD 15bn, at a time when Lebanon was already undergoing a massive economic crisis which has seen the currency collapse on the parallel market and inflation hit near 90% y/y.

The UAE said it would provide a three-phase package of measures to support investment and the labour market in an official statement yesterday, but no further details on the planned measures were provided.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Fixed Income

Optimism that a new fiscal stimulus deal in the US could be reached soon helped to sink US Treasuries overnight. Officials in the administration and Democratic party have set Friday as a deadline to reach a deal, when combined with the release of July’s non-farm payrolls could set markets up for some wide two way moves. Yields on the front end of the curve were marginally higher while the 10yr yield added 4bps.

European bond markets were also weaker overnight with gilt yields up more than 5bps and bund yields moving up by 4.5bps. High yield and emerging market debt closed higher in anticipation of a new US stimulus deal.

FX

It was another day of dollar selling overnight with the DXY index down 0.55% at 92.87. Euro was the main gainer overnight, closing at 1.19 (up 0.5%), its strongest levels since May 2018. The single currency’s rapid rise in July and August has pushed it well into over-bought territory. The economic recovery looks to be well underway in the Eurozone—retail sales in the bloc have returned to pre-coronavirus levels—but the resurgence of virus cases in countries like Spain shows that the Eurozone is nowhere near to being back to normal and the Euro exuberance may need to wane to match economic performance.

Sterling closed up 0.33% at 1.31 while there were also strong moves in favour of the commodity currencies. USDCAD closed at 1.33, its lowest level since February.

Equities

Global equities maintained positive momentum yesterday as services PMI surveys surprised to the upside, even despite the concerning indications for the labour market. In the US, the S&P 500 closed up 0.6%, cementing its ytd gains to 3.0%, while the Dow gained 1.4% yesterday. In Europe, the FTSE 100 was the big gainer, climbing 1.1%, largely driven by mining and travel firms, while the DAX and CAC added 0.5% and 0.9% respectively.

Regional equities were broadly flat, as the DFM added 0.3% and the Tadawul 0.2%.

Commodities

Oil prices added another day of gains with both Brent and WTI rising. Brent futures settled at USD 45.17/b, their highest level since March while WTI was up by 1.2% at USD 42.19/b. Data from the EIA showed a 7.4m bbl draw in US crude stocks with modest gain across much of the rest of the barrel allowing total petroleum inventories to decline. Crude output in the US was down by 100k b/d but product supplied (a demand proxy) fell by 1.2m b/d.

Gold prices settled up nearly 1% at USD 2,038/troy oz. The odds are for the yellow metal to continue hitting new record levels until there is a clearer picture on the shape of economic recovery that will take place globally. However, the upward moves in gold are occurring in tandem with gains in equity markets: indeed the 90 day correlation between daily returns in gold and the S&P 500 is at near its strongest positive level in the past five years. Should a clearer picture for the pace of economic recovery emerge funds may choose to liquidate their gold positions to fund equities, sparking a major correction.

Daniel Richards

Daniel Richards