Recent Search

Popular Searches

Escalating unrest in the United States over the weekend has dominated the headlines, with curfews imposed in several cities and the National Guard deployed in at least 12 states. Data released on Friday showed US personal spending declining by more than expected in April, down -13.2% y/y. This was despite a 10.5% y/y rise in personal income as government stimulus cheques helped to offset the impact of job losses and furloughing of employees due the coronavirus restrictions. Initial jobless claims for the week of 23 May were broadly in line with expectations at 2.123mn, down from 2.446mn the week before. All eyes will be on the May non-farm payrolls data due this Friday, with consensus estimates anticipating a contraction of -8000 jobs last month and the unemployment rate rising to 19.6%.

Eurozone inflation eased to 0.1% y/y from 0.4% in April as demand remained soft and energy prices low. The key event in Europe this week is the ECB monetary policy meeting on Thursday where the ECB is expected to boost the size of its asset purchases by another EUR 500bn and extend the PEPP programme into next year. The ECB will also update its forecasts for Eurozone growth and inflation.

China’s manufacturing PMI softened to 50.6 in May from 50.8 in April, coming in below consensus expectations. However, the non-manufacturing PMI improved to 53.6 last month from 53.2 in April. The data highlights the slow pace of recovery, particulary in manufacturing. Weak global demand weighed on new export orders, while both manufacturing and non-manufacturing jobs declined last month, according to the survey.

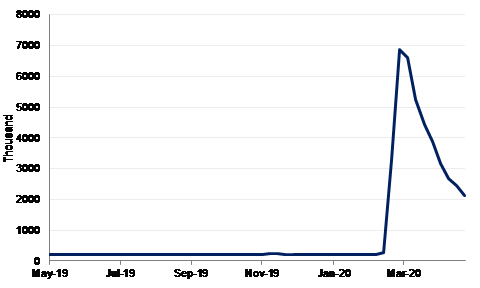

Saudi Arabia’s finance minister said on Friday that SAR 150bn (USD40bn) had been transferred from the government accounts at the central bank to the Public Investment Fund (PIF) in March and April to “strengthen the investment capacity of the fund”. Monetary statistics for April have yet to be released, but government deposits at the central bank declined by about USD 9bn in March.

Source: Emirates NBD Research

Source: Emirates NBD Research

Fixed Income

Treasuries sustained their divergence from risk assets amid flight to safety syndrome following comments from the US President on relationship with China. The curve flattened with yields on the 2y UST ending the week at 0.16% (-1 bp w-o-w) and 0.65% (-1 bp w-o-w).

The Fed Chairman in comments last week said that the central bank has crossed a lot of red lines and that he remained comfortable with measures taken so far.

Regional bond markets saw some profit booking last week following relentless gains over the past month. The YTW on Bloomberg Barclays GCC Credit and High Yield index ended the week flat at 3.50% while credit spreads widened marginally to 288 bps.

The Emirate of Sharjah has hired banks to raise as much as USD 1bn with proposed sale scheduled for as early as this week..

FX

Last week saw the dollar decline substantially amid rising global risk appetite. The DXY index, a measure of the dollar against a basket of major currencies declined by over -1.50%, to finish the week at 98.291, well below the 200-day moving average (98.516). U.S. President Trump has continued his tough rhetoric against China for their handling of the coronavirus at its initial stages and has also moved to strip Hong Kong of its special treatment. Despite some choppy movement the JPY was largely unchanged from last week's closing price at 107.83 (+0.18%).

Subsequently major currencies paired against the dollar strengthened significantly. The euro increased over 1.85% to reach 1.1103, close to a two month high for the currency. An ambitious fiscal stimulus package of up to €750billion has supported markets in the region. Sterling advanced by 1.47% from last week's closing price to reach 1.2351, bolstered by the news that the U.K. is set to gradually ease some lockdown restrictions. However, UK-EU trade negotiations still hang over it, impeding its upside for the time being. The AUD and NZD both soared last week, with the former increasing by over 2% to reach 0.6670 and the latter increasing over 1.80% to trade at 0.6204.

Equities

Regional markets started the new week on a mixed note. However, the Tadawul was a notable outlier with gains of +2.3% as it caught up with broad based euphoria of last week. The decision of local governments to ease restrictions also helped investor sentiment. Gains were led by banking sector stocks with NCB and Al Rajhi Bank adding +7.0% and +2.7% respectively.

Commodities

The improvement in oil prices in the last month has been nothing short of dramatic. WTI front month futures ended May at USD 35.49/b, an 88% gain in a single month and the largest improvement in data going back to 1990. The increase in oil prices is all the more significant given then just barely one month ago oil futures closed negative for the first time ever. Brent’s rise has been less eye-watering than WTI but Brent front month futures still managed a near 40% gain for May.

The improvement in spot prices was matched by steady gains in the structure of the forward market. The excessive contango of the last few months appear to be behind the market thanks to a considerable drop in production—both from OPEC+ and others—and sentiment improving toward demand for the rest of the year. Oil consumption is in no way going to return to pre-coronavirus levels but the scale of demand destruction may be far less than the market initially feared. December time spreads continue to narrow their contango, if not necessarily in a straight line back to neutral.

Aditya Pugalia

Aditya Pugalia