Recent Search

Popular Searches

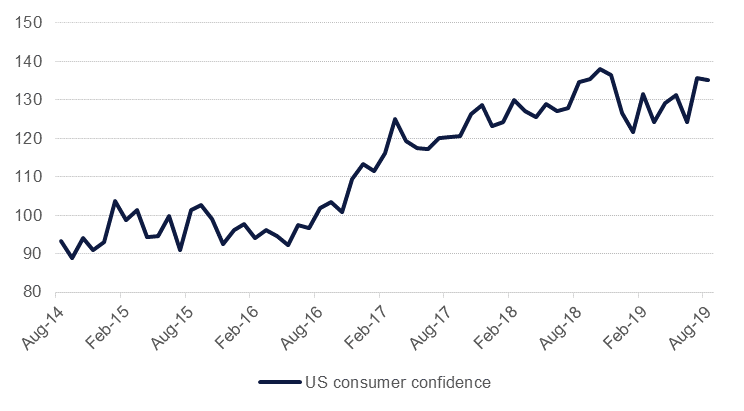

US consumer confidence continues to remain robust even as trade war hostility has escalated in recent weeks. Data released overnight showed consumer confidence for August dipping by just 0.7pts to 135.1, far better than the market had been expecting. Consumers’ assessment of the labour market, whether jobs are plentiful or not, actually increased to 39.4 in August from 33.1 a month earlier, suggesting healthy jobs numbers from the US are still in place. Market expectation of a rate cut next month remains all but certain even as the good consumer data offsets disappointing figures from industry.

The US yield curve moved further into inverted territory with the 2yr10yr UST spread at -4bps and 3mth paper against the 10yr UST at more than 50bps. Despite the better than expected consumer confidence data from the US, markets are still pricing in substantial weakness in the US economy. Markets remain in consolidation after a volatile few days around the G7 meeting but with few headlines or announcements out overnight, the overall bias in markets appears to be looking for more downside risks.

The US Federal Reserve shot back at pressure from President Donald Trump to cut rates, saying that its decisions are guided “solely by its congressional mandate” and that “political considerations” weren’t taken into account during rate setting. Fed Chair Jerome Powell has come under intense personal scrutiny by the President for not lowering rates. The Fed has struggled to come up with an effective way to communicate forward policy while the economic outlook remains leveraged on the political whims of the President which has led to the market pricing in perhaps more negativity than is warranted.

Italy moved closer to a new government overnight as the 5-Star and Democratic Party try to find consensus. A deal needs to be presented to Italy’s president by mid-day today otherwise new elections need to be held which could result in the right wing populist League winning and leading to another crisis in a core Eurozone economy. The possibility that a deal could be reached helped to bring Italian yields lower overnight and narrowed their spread over benchmark bunds.

Source: Emirates NBD Research

Source: Emirates NBD Research

Treasuries recouped most of their early week losses as caution returned to markets. Yields on the 2y UST, 5y UST and 10y UST closed at 1.52% (-1 bp), 1.37% (-4 bps) and 1.47% (-6 bps) respectively.

Regional bonds continued to track moves in benchmark yields. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped -3 bps to 3.12% while credit spreads remained flat at 162 bps.

AUDUSD is trading 0.22% lower this morning following weaker than expected construction data. Following a 2.2% q/q contraction in construction work during Q1 2019, construction work declined by a further 3.2% q/q in the second quarter. The AUDUSD has most recently been a victim of escalating trade tensions between the U.S. and China and is currently trading at 0.6766. While the price continues to see daily closes below the 0.6820 level, there is a risk of a retest of 2019’s low of 0.667. A break of this level could result in a further decline towards the 0.65 level, an outcome that will become more likely if there are any further escalations in global trade tensions.

China’s central bank continued to try and stem the depreciation of the RMB by setting the official midpoint at a stronger level than the market had been expecting. Nevertheless, at 7.0835 the official rate is still the lowest level since March 2008. The RMB has weakened for the last nine days against the dollar and is trading at 7.156 this morning.

Developed market equities closed mixed as optimism over trade talks faded following lack of follow-up by China. The S&P 500 index dropped -0.3% while the Euro Stoxx 600 index gained +0.6%.

Regional equities closed higher ahead of second phase of Saudi stocks inclusion in the MSCI EM index. The Tadawul added +0.3% in what was a rather volatile day of trading. Large caps weighed on the broader index with Al Rajhi Bank and Saudi Telecom losing -1.2% and -2.1% respectively.

Elsewhere, the Qatar Exchange and ADSMI gained +2.5% and +2.7% respectively. Most stocks on those markets closed higher.

Oil prices reversed some of the losses from earlier in the week thanks to an enormous draw in crude stocks reported by the API. Brent futures ended the day at USD 59.51/b, up 1.4%, while WTI closed just shy of USD 55/b, having gained 2.4%. The API reported a drop in crude stocks of 11m bbl last week, far higher than market expectations. EIA data will be released later tonight which may give a sign as to how healthy this year’s driving season has been in the US.

Gold added 1% overnight as investors continue to fret over the outlook for rates and the broader health of the US economy. The gain in the yellow metal helped to drag the rest of the precious metals higher with silver gaining 3%.

Edward Bell

Edward Bell