Recent Search

Popular Searches

A promise by North Korea to close its nuclear test site in May was the highlight of the historic meeting between North Korea’s Kim Jung Un and South Korea’s president Moon Jae-in over the weekend. There are suggestions that Kim could meet with Donald Trump now within a month, which should help to keep risk appetite underpinned. In addition to signs of US wage inflation and an expected surge in US debt issuance this should help to keep US bond yields and the dollar biased higher.

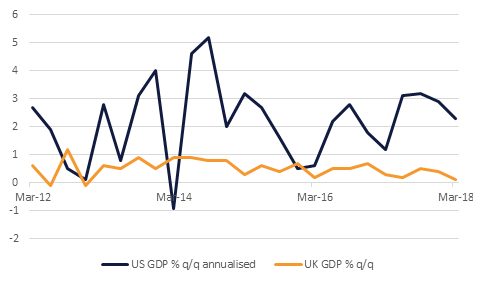

Last week ended with contrasting fortunes in the US and the UK economies. The US economy grew by 2.3% (annualized) in Q1, whilst the UK economy barely grew at all improving by just 0.1% q/q. The combination continued to cause GBPUSD to suffer, dropping to below 1.38 currently, as expectations of a Bank of England interest rate increase in May receded. Overnight the resignation of Home Secretary Amber Rudd from the UK government has also delivered another political blow to the Theresa May government, maintaining pressure on the Prime Minister herself and keeping alive speculation about the government’s future in view of its very narrow parliamentary majority.

Issues for the coming week include the US FOMC meeting and whether or not the US allows an extension to the EU’s exemption on steel tariffs. The Fed is unlikely to change monetary policy at this week’s Fed meeting, but the focus on wages will remain firmly in place in view of the 2.9% rise in wages recorded in the Q1 employment cost index. The US employment report on Friday is expected to show a bounce back in non-farm payroll jobs to around 195k, with wages likely to be the main focus within the report. The ECB left interest rates and policy guidance unchanged at its Council meeting last week, with the ECB likely to hold-off from signalling its tightening intentions until later in the summer following a loss of growth momentum in Q1.

Source:Markit, Bloomberg, Emirates NBD Research

Source:Markit, Bloomberg, Emirates NBD Research

Mixed global data and no sign of troublesome inflation left the UST curve back in its flattening mode. Yields on 2yr, 5yr, 10yr and 30yr treasuries closed the week at 2.48% (+1bp w/w), 2.80% (-2bps w/w), 2.96% (-2bps w/w) and 3.12% (-2bps w/w) respectively. 10yr Bund Yields followed suite with the UST, closing down by 2bps during the week to 0.57% while those on 10yr Gilts fell 6bps to 1.44% on the back of weaker than expected 1Q GDP growth. Weekly change in credit spreads was minimal with CDS levels on US IG and Euro Main closing at 61bps (-2bps) and 55bps (-1bp) respectively.

Bulk of the tightening of yields on long term USTs happened on Friday. Its positive impact on GCC bonds will only get to play out this week. Last week, GCC bonds generally fell in price on the back of high new supply and rising geopolitical risks. Yield on Barclays GCC bond index rose 8bps to 4.52%, led by a 7bps increase in credit spreads to 177bps.

Material increase in 10yr UST yields in the first half of the last week left 7-10yr maturity bonds as the worst hit segment in the GCC region. OMAN 27s, OILGAS 27s, EQPTRC 26s, INVCOR 27s etc all fell by more than a point last week, without any idiosyncratic news to justify the weakness.

Breaking from seasonal norms, the dollar has appreciated in April for the first time since 2010. Over the course of the month, the Dollar Index has gained 1.51% to reach 91.51, levels not seen since January. The index had climbed as high as 91.990 before finding resistance at the 200 day moving average, a level which it needs to surmount in order to maintain and build on the gains of the previous month. Also of note is that the index has broken above the 100 day moving average for the first time in 2018 and this level (90.646) is now likely to act as a support level.

Despite these developments, the weekly downtrend that has been in effect since January 2017 remains intact as is evident by analysis of the weekly candle charts. In order to confirm reversal and break out of this downtrend, the index needs to realize a firm end of week close above the 50 week moving average (92.810).

Regional equity markets closed mixed with the DFM index adding +0.2% and the Tadawul losing

-0.3%.

Drake & Scull said that the board has approved the proposal to issue a 5-year convertible sukuk up to a maximum of AED 1bn or equivalent in any other currency through a private offer. The company sees conversion at a price of AED 2.7 per share and the final structure and conditions depends on market sentiment and investor appetite. The stock was suspended from trading yesterday pending this announcement.

First Abu Dhabi Bank announced Q1 2018 results after markets closed. The bank announced Q1 2018 net profit of AED 3bn, beating consensus estimates of AED 2.78bn by 8%. The stock ended the day -0.4% lower.

Oil prices recorded a mixed performance last week but overall moves were relatively muted. Brent futures added 0.8% over five days while WTI slipped by 0.4%. The improvement in Brent is likely down to shifting expectations in the market that US president Donald Trump will walk away from the Iran nuclear deal when it is due for review in mid-May.

Investors are taking this differences into account, adding nearly 10k short positions in WTI and cutting long positions. Overall net length fell by 17k contracts last week while in Brent some profit taking was likely behind a decline in long positions. However, no short positions in Brent have been added in the past two weeks, suggesting investors believe the Iran risk will keep Brent on the boil.

The US drilling rig count expanded again last week, up by five weeks. A total of 28 rigs were added in April and 78 have been added so far this year. The pace of oil production accelerated last week to more than 1.3m b/d year on year according to the EIA. On average in 2018, US production growth is up 1.16m b/d so far this year compared with an EIA projection of 1.37m b/d in its last STEO.

Click here to Download Full article