Recent Search

Popular Searches

.jpg?h=457&w=800&la=en&hash=9DBD0B3CD1C1A2B0110E4E2A24F173CA)

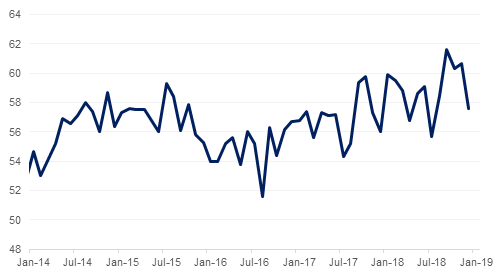

Delegates from the US and China began the crucial face-to-face negotiations in Beijing yesterday to ease the ongoing trade tensions. Both sides have much to lose if no reasonable agreement can be signed within the 90days truce period that ends on March 1. China has sent some very senior officials for these talks and is working towards presenting a plan to meet Trump's demands to cut down the USD 375 billion trade deficit. Ahead of the talks, China had also softened its stand by offering a mix of concessions by resuming purchases of US soybeans, suspend punitive tariffs on imports of US cars and toning down its “Made in China 2025” hi-tech policy. It has also proposed clear bans on forced technology transfer in new draft foreign investment legislation. While the outlook of the trade talks still hangs in balance, the negative impact of the trade tensions have begun to show its effect. The ISM Non-Manufacturing Index in the US in December fell to 57.6 from 60.7 in the prior month.

In the UK, though the Prime Minister, Ms Theresa May’s Brexit deal looks set to be defeated in a vote in the House of Commons, she confirmed that the vote on it will go ahead around January 15. If Parliament rejects May’s deal in the vote, she says the country could be forced out of the EU with no agreement in place. On Sunday, May restated her position that no deal is better than a bad deal and has stepped up contingency planning in case negotiators fail to reach an accord in time for exit day on March 29.

Within the EU, new factory orders in Germany fell by 4.3% y/y in November vs estimate of fall of only 2.7%. The fall was mainly due to fall in the airplane and consumer goods orders. That said, German retail sales increased 1.4% MoM in November vs the estimate of 0.4%, validating the fact that the largest economy in the EU block remains on solid footing. For the wider Eurozone Aggregate retail sales in November registered YoY growth of 1.1% - higher than the estimate of 0 .4% gain but worse than the 1.7% recorded in the previous month.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

The full impact of the robust US employment report released on last Friday and the positivity ensuing from the current ongoing trade talks in Beijing was felt by the UST treasury curve yesterday which shifted noticeably upwards. Yields on 2yr, 5yr and 10yr closed at 2.54% (+5bps), 2.54% (+4bps) and 2.70% (+3bps) respectively. The rising hopes of a credible plan to address trade tensions between the US and China helped reducing credit spreads. CDS levels on US IG and Euro Main closed 2bps lower each at 82bps and 86bps respectively.

Average yield on local GCC bonds reduced 3bps to 4.59% mainly as a result of six bps decline in average credit spreads from 210bps to 204bps on the Bloomberg Barclays GCC bond index.

EURUSD rose 0.69% on Monday to close at 1.1474 in a move that was mainly driven by stronger than expected Eurozone retail sales supporting the common currency, while a softer than expected ISM Composite PMI weighed on the dollar. Analysis of the daily candle chart shows that further gains were halted by resistance at the 100-day moving average (1.1477) which continues to provide resistance in the current Asia session.

This morning, AUD is trading mildly softer against the other major currencies following softer than expected economic data. Following a decline in consumer confidence during the first week of January (from 117.8 to 115.2), a decline in iron ore and coal exports in November accompanied with a narrowing trade balance during the same period (AUD 1925Mn vs AUD 2013Mn), AUDUSD has fallen 0.32% to 0.71256. Despite this decline, AUDUSD still looks likely to test the 0.7180 region (100-day moving average) and 0.7186 level (50-day moving average). A break and daily close above this level is likely to catalyse a larger move towards 0.73.

Developed market equities closed mixed with the S&P 500 index adding +0.7% and the Euro Stoxx 600 index losing -0.2%. Strength in technology stocks helped broad US indices.

Regional markets continued their positive run. The DFM index and the Tadawul added +0.1% and +1.5% respectively. Banking sector stocks continued their gains with Al Rajhi adding +2.2% and Samba gaining +4.3%. Elsewhere, QNB and FAB gained +1.0% each.

Commodity markets generally began the first full trading week of 2019 on a positive footing. The start of a new round of trade talks between the US and China has helped improve sentiment even if the risk of no deal materializing from this round still remains high. Oil futures ended the day up 1.2% for WTI at USD 48.52/b while Brent gained just short of 0.5% to close at USD 57.33. Both contracts had edged up more than 3% at one point during trading before tempering off later in the day.

Industrial metals ended the day higher as well, largely on the back of the resumption of China-US trade talks. Copper closed the day essentially flat with a positive bias at USD 5,923/tonne on the LME while iron ore added more than 1.4%.

As to be expected on a risk on day precious metals gave up some ground with silver, platinum and palladium all falling. Gold managed to gain about 0.3% to close at USD 1,288.63/troy oz. Precious metals markets will still be reeling from Fed Chair Jerome Powell’s commentary last week that rate hikes in the US would be more attuned to market conditions.

Click here to Download Full article