Recent Search

Popular Searches

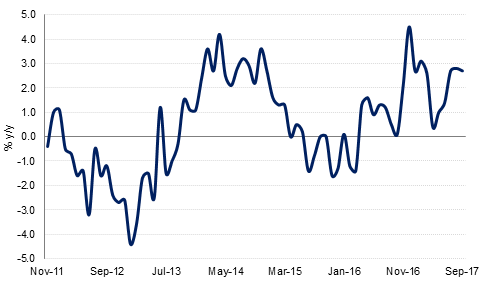

The IMF has completed the second review of Egypt’s Stand By Arrangement, opening the way for a further USD 2bn to be released, once the Fund’s executive board has approved the review. This would bring the total funds disbursed under the current facility to USD 6bn (out of a total of USD 12bn available). The IMF statement “reaffirms the authorities’ commitment to their reform program” and noted that the reforms that have already been implemented are supporting macro stabilisation and increased confidence. The IMF highlighted faster than expected growth in the last fiscal year, a narrowing of the current account deficit and higher foreign portfolio and foreign direct investment into Egypt.

This week will likely be dominated with headlines around President Trump’s Asia visit, US tax reform and increasing political uncertainty in the UK. While Republicans would like to see the tax reform bill signed before the end of the year, there is still a lot of work to be done to reconcile the drafts from the House of Representatives and the Senate. US equity markets didn’t respond well last week to the Senate’s proposal to delay corporate tax cuts unti 2019. UK data on Friday was better than expected with both industrial production and manufacturing production rising by more than forecast in September. The trade deficit was also much narrower than expected in September. However the pound is under pressure again this morning on reports that 40 Conservative MPs have agreed to sign a letter of no-confidence in PM May, and the EU has ratcheted up pressure on Brexit negotiations, saying the UK needs to clarify its position on the financial settlement in two weeks in order to start trade talks. Chief EU negotiator Michel Barnier also said that the EU was making contingency plans for a scenario in which no deal with the UK was reached before March 2019.

Key economic data this week includes inflation data in the US, UK and Eurozone as will retail sales and industrial production in the former. We also get Germany’s ZEW survey and Eurozone GDP for Q3. Speeches by Fed officials will also draw attention now that Yellen’s successor Jerome Powell is known, with Yellen herself speaking at an ECB sponsored event on Tuesday alongside Mario Draghi, the BoJ’s Kuroda and the BOE’s Mark Carney.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

US Treasury curve recorded bear steepening during the week as expectations of higher inflation from continued economic growth and pending tax reforms gained momentum. Yields on 2yr, 5yr, 10yr and 30yr treasuries rose to 1.65% (+3bps), 2.05% (+7bps), 2.40% (+8bps) and 2.88% (+9bps) respectively. Synchronized global growth led to yields across the Atlantic also increase with 10yr Gilts and Bunds closing at 1.34% (+9bps) and 0.41% (+7bps) respectively. With little catalyst for change in the credit spreads, cash corporate bonds in the developed world moved down in price in sync with the higher benchmark yields. US corporate bonds were down by nearly 1% though YTD return still remains at a healthy 5.01%.

Despite oil prices stablising at higher levels, GCC bonds suffered from uncertainties surrounding the corruption purge in Saudi Arabia and increasing geopolitical tension in the region. And rising benchmark yields added to the woes. Barclays GCC bonds index closed the week with yield at 3.58% (+11bps) and option adjusted credit spread at 140bps, 3bps higher on the week. CDS levels on GCC sovereigns increased by an average 3bps to 14bps during the week. 5yr CDS spreads on Abu Dhabi, Kuwait and KSA closed at 67bps (+4bps), 71bps (+4bps) and 105bps (+14bps w/w) respectively.

The Dollar Index (DXY) declined by 0.58% last week to close at 94.391, snapping three consecutive weeks of gains. Despite this decline, inspection of both the daily and weekly candle charts reveals that the reversal of the former 2017 YTD downtrend remains in effect. Also of note is that the index has remained above the 200 week moving average (93.221) for seven consecutive weeks now. While the index continues to trade above this level, the medium term risks are for further gains.

Following three weeks of consecutive declines, GBPUSD rose 0.87% last week to close at 1.3196, taking the price back between the 50 and 100 day moving averages (1.3246 and 1.3107 respectively). Further gains in the week ahead are likely to be severely hindered as just ahead lie many zones of resistance. These include resistance at the 76.4% one year Fibonacci retracement (1.3263), the 200 week moving average 1.3217 and the 50 day moving average (1.3246).

Global equities indices lost ground across the board, barring some gains in Asia this morning. US equities reacted negatively to hurdles in the way of tax reforms with S&P 500 and Dow Jones closing down by -0.1% and -0.2% respectively on Friday. European bourses were also in the red with FTSE 100 and DAX down by -0.7% and -0.4% respectively.

In the region, barring the stability in Dubai and Oman stock exchanges, shares continued their week long fall in most other exchanges. Tadawul led the losses, closing down by -0.81% yesterday followed by weakness in Qatar and Bahrain. DFMGI gained 0.43%, driven by gain in property shares, particularly the recovery in Emaar Properties.

Oil markets extended their gains last week, rallying five weeks in a row. Brent futures closed the week up 2.3% at USD 63.52/b and WTI added just under 2% to close at USD 56.74/b. The week’s gains were somewhat tempered on Friday on a sizeable increase in the US drilling rig count, up 9 rigs week on week and up 286 on a year ago. Political risk in the Middle East will act as a near term support for oil prices, even if there is no direct risk to production or expected change in oil policies.

Market structures softened over the course of the week. The 1-2 month Brent time spread closed at its tightest level since mid-October at just USD 0.11/b (compared with a backwardation of over USD 0.4/b at the end of last month). Meanwhile the contango in WTI widened again to USD 0.24/b, a slow but steady progress to a steepening of the curve.

On a technical basis, benchmark futures are looking both supported (by short-term averages moving above long-term averages) but also flashing signs of being overbought on momentum indicators; the 14-day RSI for Brent and WTI is holding near overbought. The tentative balance between the indicators suggests that fundamental push one way or the other could be quite sharp and see volatility spike in short order.