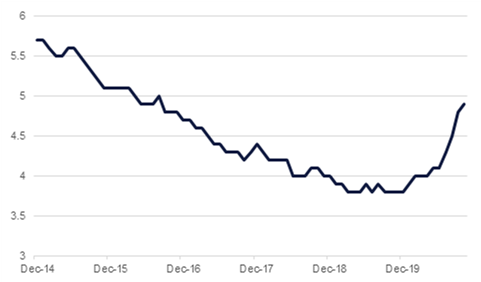

- UK labour data was released yesterday, and while the headline unemployment figure was modestly lower than projected – the actual figure was 4.9%, compared to consensus projections of 5.1% – job cuts hit a record high over the three-month period to October, preceding the last-minute extension of the furlough scheme which had been scheduled to come to an end that month. Redundancies rose by 217,000 to a record high of 370,000. The UK government is coming under increasing pressure to extend support schemes, but with public debt back at 1960s levels it is increasingly reluctant to do so. However, given that the government’s own figures project unemployment to rise to 7.5%, a failure to support households could hold back the economic recovery.

- Data released in the US yesterday underscored the ongoing challenges posed by the Covid-19 pandemic. The New York Fed Empire manufacturing survey for December came in at just 4.9, compared to expectations that the index would match November’s 6.3. Given that the city is facing a potential renewed lockdown, there could be a further slowdown in the coming months. Meanwhile, industrial production data for November showed that a slowdown in growth was already in play last month. Production expanded by 0.4% m/m, and while this just exceeded expectations of 0.3%, it was down from 1.1% in October.

- The Saudi Arabian budget projects a -7.3% cut in spending by the finance ministry next year as it looks to balance its books in the wake of the 2020 pandemic crisis and its effect on oil markets. However, officials maintain that this will be more than compensated by an increase in domestic investment by sovereign wealth funds.

- Morocco’s central bank held its benchmark interest rate at 1.5% following its MPC meeting yesterday. Having held rates at 2.25% since March 2016, Bank al-Maghrib was forced to ease policy as the pandemic crisis began in March of this year, cutting by a cumulative 75bps.

Further to rise? UK ILO unemployment rate, %

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Fixed Income

- Treasury markets are holding in a relatively narrow range as the Fed deliberates in its December FOMC. In an almost complete mirror image of the prior days trading treasuries fell toward the end of trading in line with a strong risk-on move in equities. Yields on the 10yr UST ended higher at 0.9080% while the 2yr was essentially unchanged.

- Bond markets were generally quiet in anticipating of the Fed meeting and also optimism that US politicians were nearing consensus on a support package.

- Egypt has reportedly contacts banks for a new Eurobond issue with the potential to raise up to USD 7bn in 2021.

FX

- Sterling was again the main mover in currency markets, rallying 1% to push above 1.34 overnight as markets continue to price in a Brexit deal. While the pressure of the impending Dec 31 deadline should help to firm negotiators’ minds over the severity of the issue, sterling has witnessed many ‘a deal is near’ head fakes in the past and a failure to reach an agreement could open substantial downside volatility.

- Elsewhere the sell-off in the greenback remain entrenched with USDJPY slipping below 104 while commodity currencies were all higher against the USD overnight.

Equities

- A more positive political outlook spurred risk-on tone in equity markets yesterday. The expectation of a relatively smooth transition to a Joe Biden presidency in the US saw all three major indices close higher, with the Dow Jones gaining 1.1%, while the NASDAQ and the S&P 500 closed up 1.3%.

- European equities also had a broadly positive day as the DAX gained 1.1%. The FTSE 100 closed down -0.3%, but this is more a reflection of the positive moves in sterling on the back of trade deal hopes hitting multinationals, and UK-focused firms largely ended the day higher.

Commodities

- Oil markets recorded another healthy day of gains with Brent and WTI futures up either side of 1% in overnight trading. Brent closed at USD 50.76/b, a gain of 0.9%, while WTI was up more than 1.3% to settle at USD 47.62/b.

- The gains came despite a modest increase in US stockpiles reported by the API and a downbeat assessment from the IEA over the demand outlook for 2021. Much like OPEC earlier in the week the IEA lowered its 2021 demand growth forecast and noted that markets will be very fragile, particularly in H1, with the risk of pushing back into surplus.

Click here to Download Full article

Daniel Richards

Daniel Richards