Recent Search

Popular Searches

Figures from the Office for National Statistics showed the UK economy tentatively recovered from the coronavirus slump, with gross domestic product (GDP) rising by 1.8% in May. This is less than many economists have expected and has dashed hopes of a swift rebound, with government forecasters saying the economy was on course for its worst performance this year since pre-industrial times. The growth in May comes on the heels of a record 20.3% slump in April when the lockdown was at its tightest. Tuesday's data has raised doubts over how much of a recovery the UK will see after businesses were allowed to reopen in June and July as the coronavirus outbreak eased. Of note was activity in the key services sector which did not recover as expected in May, barely eking out 0.9% growth. The government's Office for Budget Responsibility said on Tuesday that unemployment was likely to surge to 11.9% this year under its central scenario, and exceed 13% in a worst case scenario. The government forecasters said output in 2020 was likely to be 12.4%-14.3% lower in the two scenarios, this marks the biggest drop in more than three centuries for the UK.

The US Labor Department said the consumer price index (CPI) increased 0.6% in June, after easing 0.1% in May. The increase ended three straight months of declines, which was largely led by a 12.3% jump in gasoline prices after declining for the first five months of the year. Food prices rose 0.6% against 0.7% in May. A spike in new COVID-19 cases however suggests a moderation in demand that could keep inflation muted, as densely populated states in the South and West regions of the country were pulling back or pausing reopening businesses.

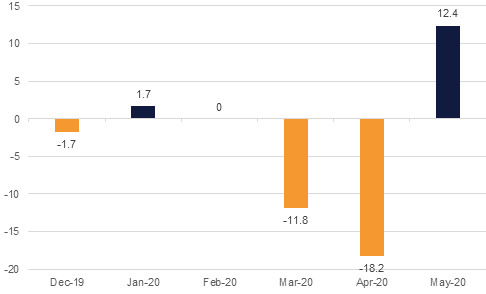

Eurozone industrial production rose by 12.4% (m/m) in May but was still down by 20.9% (y/y), compared with April’s 28.7% (y/y) drop. This was mostly driven by a surge in production of durable consumer goods. While most economists had called for a 15% (m/m) increase, the figures fared much better than 8.2% (m/m) decline in April, and 11.8% (m/m) drop in March. In Germany, the ZEW economic research institute said investor sentiment dropped slightly in July, slipping to 59.3 points, down from 63.4 points the previous month. The ZEW’s assessment of the current situation improved slightly for the second time since January 2020. The current conditions index rose to -80.9 from -83.1 in the previous month.

Source: Eurostat, Emirates NBD Research

Source: Eurostat, Emirates NBD Research

Treasury markets closed lower overnight with moves held in a narrow range. Yields on the 10yr UST did touch 0.6% but managed to close nearly unchanged at 0.62%. A rebound in inflation in the US should help to provide some near-term support for yields; however, should lockdowns again be re-introduced en masse across the country then some of the price recovery may prove fleeting. European markets all saw bond prices push higher with yields on 10yr gilts down almost 4bps and bunds by almost 3bps.

Emerging market bonds closed lower, showing some signs of resistance around their current levels. UAE USD-denominated bonds closed essentially unchanged with a slight downward bias. The resurgence of virus cases across the world as well as escalating China-US tensions will hardly be providing emerging market assets with much comfort and the strong gains for the EM bond index over the past few months may be showing signs of running out of steam.

The government of Sharjah sold USD 1bn in 30yr Formosa bonds on Tuesday at 4%, this comes on the heel of a USD 1bn of sukuk that the emirate sold last month. The Formosa bond is Sharjah’s first non-Islamic benchmark bond, and is a type of debt sold in Taiwan by foreign borrowers and denominated in currencies other than the Taiwanese dollar. Sharjah received around USD 3.7bn in orders for the bond and tightened the yield after it began marketing at around 4.375% earlier on Tuesday.

Not much changed for the dollar on Tuesday. The DXY index experienced a downside key reversal after touching highs of 96.701 in the afternoon. CPI data out of the U.S. was slightly better than expected but market mood remains unchanged. The currency stands at 96.190. USDJPY struggled to make a decisive move either way, trading mostly sideways for the day and has consolidated minor losses at 107.20.

The euro surged to highs of 1.1423 this morning, its highest point since early March. Broad-based dollar weakness has proven beneficial for the euro which looks to continue its upward trend and remains above the 1.1400 level. Poor GDP data out of the U.K. drove Sterling to lows of 1.2480 in the afternoon, but it has since reversed all of these losses to trade at 1.2570. The AUD recorded gains of over 0.80% and reached the 0.6995 handle while the NZD experienced minor losses to trade at 0.6530.

Equity markets in the US fixated on the possibility of a new coronavirus vaccine being developed and reversed much of the prior day’s losses. The S&P 500 closed up 1.3% while the Dow added more than 2%. Asian equities are more mixed this morning with gains in the Nikkei being offset by a drop in Shanghai.

Local markets were on the backfoot with declines of 0.7% on the DFM and 0.45% on the ADX. Financials brought the DFM lower while Emaar Malls fell more than 2%. The Tadawul also closed lower, down by 0.4%.

Oil prices recovered their weakness early in the day to close higher overnight with WTI pushing back above USD 40/b and closing up by nearly 0.5%. Brent futures closed up 0.4% at USD 42.90/b. OPEC+ will decide whether to extend the deep level of cuts at its JMMC today and will also consider whether to ask countries that failed to hit their targets earlier in the deal to make additional cutbacks.

OPEC’s own assessment of oil markets shows demand recovering in 2021 by 7m b/d, even though it will still be left at levels below 2019 or 2018 demand. However, the share of the market that OPEC will control will be greater thanks to stable or declining production in other producers, particularly the US.

Click here to Download Full article

Daniel Richards

Daniel Richards