Recent Search

Popular Searches

UK foreign secretary Boris Johnson resigned yesterday, in opposition to the Prime Minister’s softer Brexit strategy. He was replaced by health & social care secretary Jeremy Hunt. Dominic Raab, a pro-Brexit MP and formerly a minister of housing, was appointed as Brexit Secretary, replacing David Davis who resigned on Sunday. With two senior cabinet resignations within 24 hours, there is a risk that Theresa May could face a vote of no confidence called by Tory MPs, but this does not appear to be imminent at this stage. GBP weakened slightly following Boris Johnson’s resignation but remains relatively resilient, perhaps reflecting the increased likelihood of a “soft” Brexit, which businesses and markets would favour. There is a raft of economic data due in the UK today including industrial production, construction output, services index and a new monthly GDP release.

Chinese CPI was in line with market expectations in June, rising 1.9% y/y from 1.8% in May. Producer inflation rose faster than expected at 4.7% y/y (from 4.1% in May), on higher commodity prices. Analysts expect PPI inflation to ease in the coming months. China’s FX reserves, released yesterday, increased in June to USD 3.1tn, surprising the market and boosting the yuan.

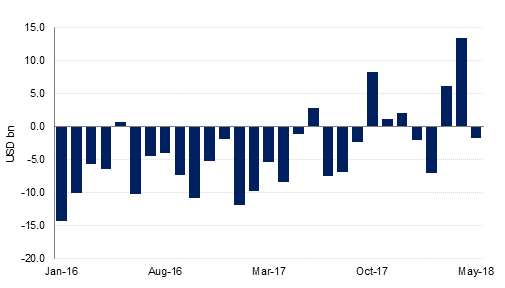

Saudi Arabia’s net foreign assets at the central bank declined –USD1.8bn in May to USD 497.1bn. Reserves had increased by nearly USD 20bn in March and April. The latest balance of payments data showed a sharp rise in the current account surplus in Q1 2018, to USD 11.1bn. Outflows on the financial account were lower than in Q1 2017 as well. Money supply and private sector credit growth remained weak however. M2 rose just 0.6% y/y while private sector credit growth slowed to 0.5% y/y in May.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

Treasuries closed lower as risk assets saw some strength. Yields on the 2y UST, 5y UST and 10y UST closed at 2.55% (+2 bps), 2.74% (+3 bps) and 2.85% (+3 bps) respectively.

Regional bonds continued to build on momentum from last week. The YTW on the Bloomberg Barclays GCC Credit and High Yield index dropped -3 bps to 4.46% and credit spreads tightened 6 bps to 177 bps.

Dubai Aerospace Enterprise Ltd said its board approved a bond repurchase program of up to USD 300mn. Repurchases will be conducted through open market transactions and pursuant to this approval the company has repurchased USD 43mn of bonds maturing in 2024.

USDJPY has broken the 111 handle (currently trading at 111.09) amid trade concerns being brushed aside and increased market risk appetite. A daily close above the May high (111.40) is likely to result in further gains in the short term and while the price remains above the 200-day moving average (110.07), short-term risks remain to the upside.

GBP continues to find itself under pressure amid Brexit turmoil, despite economic data showing an improvement in the UK's economy and an 80% chance of a 25 bps rate hike from the Bank of England in the next month. The pound continues to be the subject of selling pressure as Prime Minister May's stance on Brexit continues to put the survivability of her Government at risk. As we go to print, GBPUSD is trading at 1.3240, down from highs of 1.3361 on Monday.

Developed market equities closed higher as no fresh development on the trade front was construed as good news. The S&P 500 index and the Euro Stoxx 600 index added +0.9% and +0.6% respectively.

Regional equities continue to struggle to find a definite trend. The Tadawul was a notable exception in what was a weak day of trading for GCC equities. Drake & Scull rallied +10.6% following reports that an internal probe by the company has concluded that the former CEO owes the company as much as AED 1bn. The amount reported exceeds the current market capitalization of the company.

It was Brent’s turn to respond to idiosyncratic factors to start the week as the North Sea benchmark gained 1.2% to close above USD 78/b. Oil workers in Norway have been threatening to go on strike which could add to the already elevated number of unplanned disruptions affecting oil markets. WTI held roughly steady overnight at USD 73.85/b.

Suhail al Mazrouei, the energy minister of the UAE and president of OPEC, defended OPEC’s role in trying to return oil markets to balance, saying the producers’ bloc “alone cannot be blamed” for all the disruptions supporting oil prices. US president Donald Trump has repeatedly criticized OPEC for allegedly trying to manipulate prices.