Recent Search

Popular Searches

Economic data proved softer than expected in the UK in October, with both GDP and industrial production falling short of expectations. Compared to expectations for 0.1% m/m growth, GDP data showed that the economy remained flat at 0.0% m/m during October, following a 0.1% m/m contraction in September. In the same month industrial production expanded by 0.1% m/m following a 0.3% m/m contraction in September. The data carries the risks that Q4 GDP will in turn be weaker than expected.

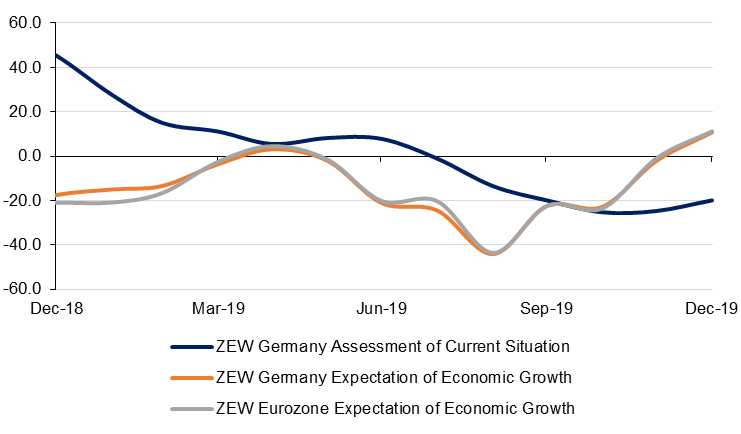

Elsewhere in Europe data was more positive with sentiment improving in the Eurozone’s largest economy, Germany. The ZEW surveys rebounded in December with the expectations component reaching 10.7 up from -2.1 in November, the highest reading since February 2018. Current conditions also improved but stayed in negative territory at -19.9 in December, but up from -24.7 previously. Following the stabalization of the IFO’s and PMI’s in previous months, it seems investors are becoming more confident that trade tensions and Brexit will be resolved at least enough to prevent the German economy from sinking into recession. However, the surveys do not have a strong correlation with GDP and probably overstate the the degree of actual improvement.

Headline inflation in Egypt rose to 3.6% y/y in November, compared to the 3.1% recorded the previous month. Despite the first acceleration in price growth in five months, real interest rates are still in strongly positive territory at 8.7%, reaffirming our expectation of another cut to the benchmark overnight deposit rate at the December 26 meeting.

Interstingly among the issues discussed at the GCC summit taking place in Riyadh yesterday was the need for legislation for proposed regional economic integration by 2025 including financial and monetary union, according to the summit’s communique. This has been an objective of the GCC since the 1980s, with various attempts to initiate it over the years, most recently in 2009.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

With few direct economic catalysts to affect markets, Treasuries oscillated around 1.82% on the 10yr ahead of the Fed meeting later today. Better than expected investor sentiment out of Germany helped to keep bunds flat while the prospect of a Conservative majority result in the UK’s general election helped gilt yields nudge higher.

Local bonds nudged higher and spreads over benchmarks compressed. However, pricing action is muted given how close the market is to year end.

Opinion polls continue to provide direction for GBP this time causing it to soften as the latest YouGov poll showed support for the Conservative party lessening in the final day of campaigning, projecting a 28 seat majority rather than a 68 seat one predicted a fortnight ago. Meanwhile the USD has lost a little ground as the dealine for the next tariffs due to be imposed on China approaches next week.

Wall Street was lower as nervousness is growing about the outcome of the US-China trade talks. White House acting Chief of Staff caused some concern, reminding that a delay will depend on how the talks go between now and the deadline. Meanwhile, earlier headlines said the U.S. and China are discussing ways to deescalate the tariff conflict such that there could be a delay to the imposition of more tariffs on December 15. White House adviser Peter Navarro cited no indication that President Donald Trump has made a decision either on a deal or on proceeding with the tariff hike.

Oil prices manage to settle higher after a choppy late session. Brent futures closed up 0.14% at USD 64.34/b while WTI gained 0.4% to close at USD 58.91/b. However, both benchmarks have given up more than those gains in early trading today as API data showed a modest build in US crude inventories (1.4m bbl). Trade anxieties remain forefront in the commodities market as the deadline for the US to impose new higher tariffs on Chinese goods moves closer.

The EIA lowered its 2020 supply forecast for US production to 13.18m b/d, from 13.29m b/d previously. US production will expand by 930k b/d in 2020, down from a forecast of 1m b/d in the prior report. While it is a downgrade, the pace of growth at nearly 8% is still enormously fast and will keep the US as by far the largest producer of crude oil.

Palladium continues its rally, gaining 14 sessions in a row as of this morning. At over USD 1,900/troy oz the metal could easily push above USD 2,000/troy oz as there is little sign of supply constraints easing.