Recent Search

Popular Searches

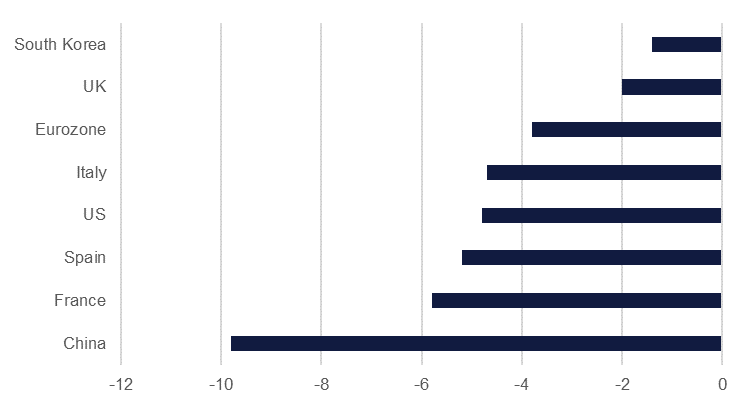

UK GDP contracted by -2% q/q in the first quarter (beating expectations of -2.6%), but this will likely deteriorate further in Q2 as the coronavirus pandemic-related shutdown only began in earnest towards the end of the period. March saw a 5.8% decline as the restrictions took hold late that month, boding ill for Q2 given that there has been only a very partial easing of the lockdown as of mid-May. While the UK’s first-quarter contraction was less severe than those seen in other major economies, they were largely affected by the pandemic earlier than the UK. Germany is set to release its Q1 growth figures tomorrow.

Fed Chair Jerome Powell reiterated his opposition to negative rates when speaking yesterday, culminating a week in which other Fed officials have also dismissed the strategy as inappropriate for the US at this juncture. There has been mounting speculation about the prospect of negative rates in the US as the market implied probability rate has dipped below zero for the first time, just, and there has been ongoing pressure from the White House via President Trump’s Twitter account. However, Powell confirmed that ‘the committee’s view on negative rates really has not changed. This is not something that we are looking at.’ The other key takeaway from the session was Powell’s call for additional fiscal support during the coronavirus pandemic crisis, saying it ‘could be costly, but worth it.’ However, the USD 3tn relief bill currently in Congress has been labelled ‘dead on arrival’ by President Trump, and is unlikely to make any headway in the Republican-controlled Senate.

Consumer prices in the UAE declined -0.9% m/m and -1.6% y/y in March, despite a 2.9% m/m (4.0% y/y) rise in food prices. This was offset by a broad decline in most other components of the CPI including a -19% m/m (-9.9% y/y) drop in recreation & culture. Housing & utilities costs fell -4.1% y/y while transport costs declined -3.1% m/m and -1.5% y/y with the latter largely due to the collapse in oil prices. Coronavirus has proved to be deflationary around the world, as demand for non-essential goods and services ground to a halt in March and April. Separately, the ruler of Dubai tweeted that some ministries may be merged and revamped to improve government’s agility and flexibility in a post-coronavirus world. Meanwhile, Oman has announced a further 5% cut to ministries’ budgets this year in response to much lower than expected oil prices further to a 10% cut in April. It also announced forced retirement for government employees who have served more than 30 years, and halved the salaries of board members in government organisations. If the additional spending cuts are fully implemented, total expenditure could be contained to OMR 11.5bn this year, yielding a budget deficit of -OMR 3.7bn or almost -15% GDP.

Source: Emirates NBD Research

Source: Emirates NBD Research

Treasuries closed marginally higher as rising US-China tension fueled risk-aversion in broader markets. Further, comments from the Fed Chair Jerome Powell had a mixed impact as he ruled out negative rates even as he acknowledged risk of medium term damage to the economy and the need to do more. The curve bull flattened with yields on the 2y UST and 10y UST closing at 0.16% (flat) and 0.65% (-1 bp).

Regional bonds shrugged off broader risk-off tone and extended their positive run. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped to 3.71% (-1 bp) while credit spreads widened marginally to 310 bps.

It’s been a volatile week for the dollar, yesterday again reversing a lot of its earlier moves to trade just around Monday's closing price at 100.245 on a DXY index basis. The DXY index, a measure for the dollar against a narrow basket of other major currencies, experienced an upturn after comments from Fed Chairman Jerome Powell. Powell dismissed the idea of negative rates, with some investors speculating that further quantitative easing could be ahead. USD JPY was largely unchanged, dipping by only -0.20% to 106.90, but other currencies were more affected.

The Euro retreated from highs of 1.0896 in the afternoon, falling to 1.0813. Sterling experienced similar movement to this, culminating in the currency dropping to 1.2210, its lowest point in five weeks. There was a slight glimmer of hope to come out of the U.K. however, as its GDP dropped by a less than expected 2.0%, against predictions of 2.6% during the Q120, but no doubt the Q2 reading will be much worse. The currency currently trades at 1.2215

The AUD also dropped against the strengthening dollar by over -0.50% to 0.6440. Meanwhile the NZD dropped dramatically after the nation's reserve bank stated that negative cash rates "will become an option in the future". The currency decreased over 1.40% to fall below 0.6000 at 0.5990.

Developed market equities closed lower as the Fed Chairman Powell reiterated his somber assessment of the US economy over the near and medium term. The S&P 500 index and the Euro Stoxx 600 index dropped -1.8% and -1.9% respectively.

Regional equities closed mixed with the DFM index adding +1.5% and the Qatar Exchange losing -1.0%. Investor sentiment in the UAE received a boost as the government eased restrictions further and allowed several activities to resume. First Abu Dhabi was a notable underperformer with losses of -3.8% after the bank disclosed an exposure of USD 73.2mn to Phoenix Commodities and related entities. The Tadawul (+0.6%) was dragged higher by Al Rajhi Bank (+1.1%). The bank reported Q1 2020 net profit of SAR 2.38bn, lower than Q1 2019 profit of SAR 2.57bn.

Oil markets weakened in line with other risk assets as Fed chair Jerome Powell gave a sobering assessment for the US economy. Brent futures fell by 2.6% to settle at USD 29.19/b while WTI was off by a little less than 2% at USD 25.29/b. Prices fell even though crude inventories actually declined last week, the first weekly decline since January. Production in the US fell by another 300k b/d last week while product supplied managed to tick higher.

OPEC revised its demand expectations for 2020, now anticipating a drop of around 9m b/d this year compared with 6.9m b/d previously. The new level brings it closer in line with assessments from the IEA. OPEC also brought down the call on its own crude to 24.26m b/d.

Daniel Richards

Daniel Richards