Recent Search

Popular Searches

The April monetary survey showed M2 growth accelerated slightly to 9.7% y/y in April from 9.5% in March. The main driver was growth in narrow money (M1) as cash in circulation surged 21.9% y/y (16.6% y/y in March) and demand deposits grew 8.5% y/y in April (4.2% y/y in March). Government deposits increased m/m but were down -4.6% y/y.

Private sector credit growth declined -0.5% m/m and -0.4% y/y. Average private sector credit growth in the first four months of this year was -0.1% y/y, despite more liquidity being made available to banks to help mitigate the impact of the coronavirus on the economy.

The breakdown of domestic credit for all banks shows that 45% of domestic lending is to the business & industrial sector, where loan growth as averaged 1.3% since the start of the year. This is much slower than average loan growth of 5.7% y/y in the first four months of 2019. As expected, m/m loan growth to this segment did spike in March 2020, but surprisingly declined -0.5% m/m in April.

Credit to retail borrowers has been contracting on an annual basis since February 2019, and this trend didn’t change in March and April. In fact, lending to retail accounts declined m/m in both March and April despite widespread salary cuts, and some redundancies. Consumers have continued to deleverage.

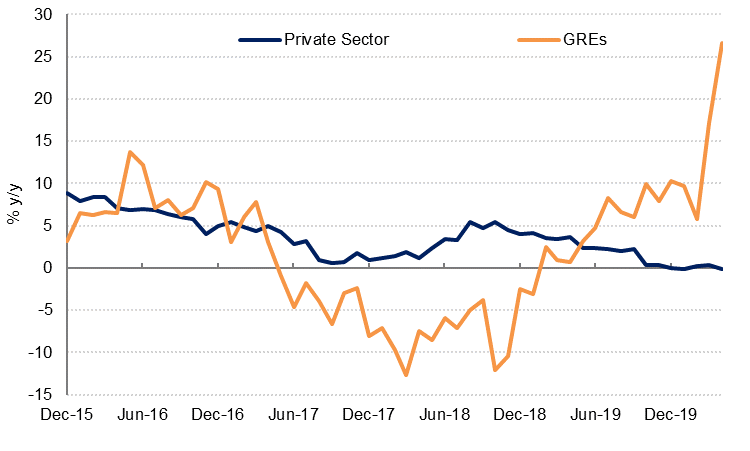

Loans to public sector entities (excluding government) have been the main driver of overall bank lending during the peak of the coronavirus disruption, rising 8.7% m/m in March and another 8.1% m/m (26.6% y/y) in April. Gross lending to public sector borrowers rose AED 32.5bn between end-February and end-April 2020, compared to a AED 3.6bn increase in loans to private all sector entities combined.

Growth in loans to government has slowed since the start of the year but remains significantly faster than loan growth to the private sector, at 14.8% y/y in April.

Source: Haver Analytics, UAE central bank, Emirates NBD Research

Source: Haver Analytics, UAE central bank, Emirates NBD Research