Recent Search

Popular Searches

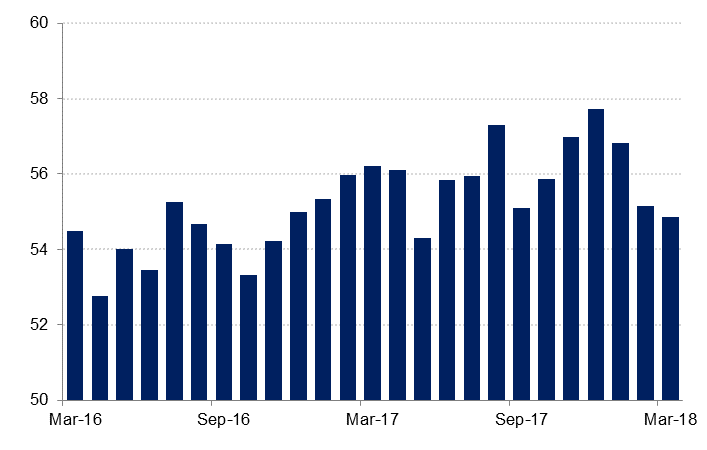

The Emirates NBD Purchasing Managers’ Index (PMI) for the UAE declined to 54.8 in March, from 55.1 in February. This marked a 10-month low for the index, indicating that while growth in the UAE’s non-oil private sector remains robust, it is slowing. The decline in March was in large part driven by a slowdown in output, which fell from 57.7 to 57.1, representing the lowest level since February 2016.

This slowdown was somewhat inevitable following the surge in activity recorded in the final months of 2018, as output was stepped up prior to the implementation of a new 5.0% value added tax which was introduced in January. Nevertheless, the PMI remains comfortably above the neutral 50.0 level which delineates expansion and contraction, and we retain a positive outlook for the year ahead. Higher oil revenues will bolster government revenues, which will support an expansionary budget with greater spending on infrastructure projects and public sector wages.

Our positive sentiment is shared by respondents, and the future output index rose to 63.8 in March, from 57.2 the previous month. Firms expect to benefit from an expected global economic upturn, given the UAE’s position as a major global trade hub, and 27.7% anticipate that output will be higher in 12 months’ time, compared to 14.5% in February.

Firms continue to make price discounts in a bid to support consumption, as evidenced by the 48.3 reading on output prices, the second consecutive month that the subcomponent has read under 50.0. Indeed, output prices have only come in above 50.0 once in the past 12 months. The squeezed margins firms with are dealing are the likely cause of stagnant staff costs, with 100.0% of respondents stating that average wages were the same as the previous month. New job creation is also slow, and the employment index fell to a 17-month low at 50.3. Only 0.6% of firms said that employment levels were higher in March than in February.

Daniel Richards

Daniel Richards