Recent Search

Popular Searches

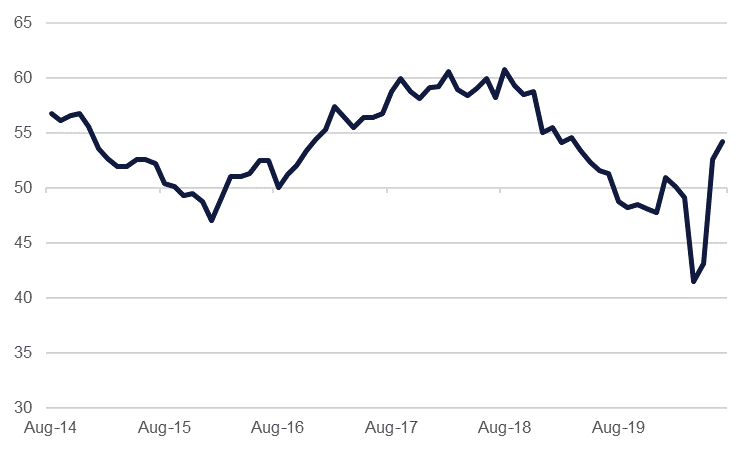

The US ISM manufacturing survey for July exceeded expectations, coming in at 54.2, compared to consensus 53.6. It was also up on June’s 52.6, signalling improving conditions in US factories. Particularly promising was the new orders component, which hit 61.5, the highest level since 2018. On the downside, however, employment remained sharply contractionary at 44.3, potentially implying that the US consumer will remain fairly weak for the time being, especially on the heels of the second consecutive weekly rise in initial jobless claims last week. Anecdotal reports accompanying the survey were also full of uncertainty. China’s July Caixin manufacturing PMI was also released early yesterday, climbing to 52.8 from June’s 51.2.

Tensions between the US and China continue to make headlines, with US President Donald Trump stating that China must cease operating social media application TikTok in the US by September 15. Whether or not a mooted sale to Microsoft goes ahead, China has threatened retaliations. The developments run the risk of a return to the strife and uncertainty which dominated 2019 headlines and could weigh on any nascent economic recovery in what is already a very volatile year.

Consumer prices in the UAE rose 0.3% m/m in June but were still down -2.4% y/y. However, the annual rate of deflation eased from -2.7% y/y in May. Housing & utilities costs, the largest component of the consumer basket, rose 0.5% m/m – the largest monthly increase since January 2018 when VAT came into effect. However, housing & utilities costs were still down -3.0% y/y. Food prices increased slightly m/m while the annual inflation in food prices slowed to a still high 5.7% in June from 6.2% y/y in May. The cost of most services have declined over the last year, except for education, which was up 1% y/y in June. We expect the overall rate of deflation to moderate further in H2, with average CPI forecast at -2.0% in 2020.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

A general risk-on tone to markets helped push bonds lower at the start of the week. Most major investment grade bond indices closed lower while riskier corporate and emerging market debt gained. Yields across the whole of the UST curve closed higher: the 2yr yield nudged back up to 0.1093% while the 10yr yield added more than 2bps to settle at 0.5543%. Both are tentatively going higher in early trade today.

Regionally the primary market is quiet with recent borrowing in local currencies.

The dollar managed to record a second consecutive day of gains overnight for the first time since the end of June. Pull-backs in the Euro was likely the main driver to send the dollar index higher while a risk-on tone to markets helped weaken both CHF and JPY against the USD. Despite the risk-on sentiment both the AUD and NZD closed lower ono the day.

Equities enjoyed a strong day yesterday, with most major global indices seeing gains in the region of 1.0%-2.0% as all regions enjoyed better-than-anticipated survey results. Europe was particularly strong as the DAX gained 2.7% and the CAC 1.9%, while the UK’s FTSE 100 rose by 2.3%. These were all buoyed by the positive final reading on their most recent PMI surveys, which confirmed the strongest pace of growth in years – even if only in m/m terms. The better-than-expected ISM manufacturing survey from the US also aided sentiment, and the S&P 500 closed up 0.7%. Meanwhile, the Caixin PMI survey in China, which also came in above expectations, helped push the Shanghai Composite up 1.8% on the day.

Oil prices rallied at the start of the trading week, buoyed by a healthy bounce in the US manufacturing ISM. Brent futures closed up just shy of 2% at USD 44.15/b while WTI closed at USD 41.01/b, up 1.8%.

Total production from OPEC rose by 900k b/d in July as Saudi Arabia, the UAE and Kuwait unwound the extra level of cuts they committed to during the OPEC+ deal. Output from Saudi Arabia was up by 900k b/d while the UAE and Kuwait added 20k b/d and 70k b/d respectively.

Daniel Richards

Daniel Richards