Recent Search

Popular Searches

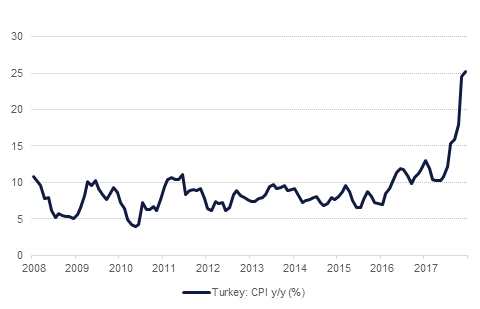

Turkish CPI inflation rose slightly to 25.2% y/y in October, from 24.5% the previous month. Core inflation rose from 24.1% to 24.3%. While this is the highest rate since 2003, the rate of acceleration has slowed, offering hope to policy makers that the worst may now have passed and reducing pressure on the central bank to take further action on rates before year-end. The lira has recouped some of its losses over recent months, and tax cuts on items such as cars, white goods and furniture introduced last week could also ease pressures in the near term. That being said, this move has raised concerns regarding fiscal prudence in Turkey and could also stimulate consumer demand, leading to greater inflationary pressure down the line.

Egyptian foreign reserves rose to USD 44.50bn in October, compared to USD 44.46bn in September. Although this is a record high, the pace of reserves accumulation has slowed dramatically in 2018 as compared to 2017; since February, reserves have grown only 4.7%, compared to an expansion of 38.0% over the February to October period last year. Portfolio inflows have come under pressure in 2018 in line with general EM aversion globally, while exports and FDI have not yet picked up to compensate.

The services sector PMI for the UK weakened in October to 52.2 from 53.9 a month earlier. The decline was larger than expected by market consensus and reflects concerns among businesses over the outlook for Brexit negotiations. Indeed the expectations component was at the lowest level since July 2016, the month after the UK voted to leave the EU.

The services sector in the US recorded another strong data print with the ISM non-manufacturing index coming in at 60.3 for October, down from 61.6 a month earlier but stronger than the market had been expecting. Components of the index all reportedly positively but the overall services sector may show signs of fading once the one-off impact of lower taxes is eliminated from the base next year.

Treasury markets were little changed ahead of the US mid-terms. Yields on 10yr Treasuries were just shy of 3.2% although they have regained that levels this morning. The 2yr-10yr spread compressed marginally by 1.5bps. While there is seeming consensus on the outcome of the election markets have been wrong footed on several major political events in recent years; hence investors may be waiting until results are out before taking a view on the direction of the rates market.

Locally GCC bond market had little idiosyncratic news to trade on. Average yield on GCC bond index rose a bp to 4.69% mainly as credit spreads had a widening bias on the back of recent softness in oil prices. Option adjusted credit spreads on GCC bonds rose 2bps to 168bps and CDS levels on GCC sovereigns were generally higher by a bp or two..

Fitch affirmed Abu Dhabi’s rating at AA/stable citing the emirate’s strong fiscal and external metrics and high GDP per capita, balanced by high dependence on hydrocarbons. Fitch sees fiscal surplus of 2.7% of GDP in 2018 vs deficit of 3.5% of GDP in 2017.

GBP began the week on a stronger note following a report in the Sunday Times that European Union had made a significant concession to allow the UK to avoid having a hard border with Ireland. Rumours about the resolution of this divisive point were constructive towards sterling and GBPUSD was able to climb above 1.3050, hitting a two week high in the process. As we go to print, GBPUSD is currently trading at 1.3054. A break and daily close above 1.3090 would be likely to result in further gains for the pound, however, the cross remains sensitive to geopolitics and Brexit uncertainties.

The Bloomberg Dollar Spot Index is little changed with Yen slightly softer against the dollar while Euro holding steady at 1.1409.

US equities ended the day positively as investors positioned themselves in ‘defensive’ sectors. The S&P 500 closed up 0.56% while the Dow gained 0.76%. European equities were more mixed although the FTSE managed a modest gain of 0.14%. Asian bourses have opened mixed this morning. Shares are climbing in Japan while Chinese shares are underperforming even as the country’s vice president said Beijing remained ready to discuss a trade solution with Washington.

Local markets were more mixed with a decline of 0.4% in the Dubai market while Abu Dhabi gained more than 1%. The Tadawul dropped by 1%.

Despite news that the US would be granting waivers to eight importers of Iranian crude, international oil prices settled higher to start the week. Brent futures closed up nearly 0.5% while WTI was about flat. The US will allow China, India, South Korea and Japan as well as four other smaller importers to continue importing Iranian crude for 180 days, delaying a tightening of the market. Other OPEC members may respond by cutting back on production to avoid pushing the market back into surplus over the coming months. Volumes of Iranian crude had already dropped ahead of the sanctions coming into effect and we don’t expect exports to recover much ground, even under the waivers.

Time spreads remain under pressure although Brent managed to regain a small backwardation at the front of the curve. In WTI, the 1-6 month spread is at around USD 0.5/b.

Edward Bell

Edward Bell