Recent Search

Popular Searches

The main focus today will be on the ECB Council meeting which meets to set monetary policy. Although the ECB is unlikely to change its policy settings, it will be the comments of President Draghi that will be of interest in the context of the slowing growth in evidence in the Eurozone recently. Although some at the ECB are calling for an end to asset purchases, the recent economic data has been disappointing especially in Germany where the Bundesbank has been the most vocal voice against QE. For this reason it seems Draghi will be even less non-committal about the likely timeline for bringing QE to an end. Any perceived dovishness on his part will play in to the weaker EUR story that is underway at the moment.

A BOJ council meeting also begins today and concludes tomorrow, but here too there is not expected to be any change in monetary policy. Japanese March CPI last week came in at 1.1% y/y down from 1.5% in February, while the core rate eased to a 0.9% y/y rate from 1.0% y/y, taking it further away from the BOJ’s target. The JPY has been one of the biggest casualties of dollar strength in recent days and looks set to carry on softening. .

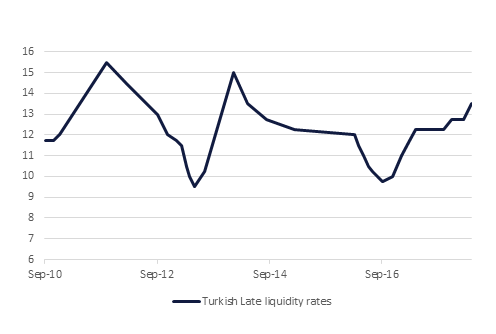

The Central Bank of the Republic of Turkey hiked its late liquidity rate by 75bps from 12.75% to 13.50% yesterday, exceeding expectations of a softer 50bps hike. The one week repo, overnight borrowing, and overnight lending rates were all unchanged at 8.0%, 7.25% and 9.25% respectively. The above-consensus move could be positive for the lira, which has sold off strongly against the dollar over recent months, as cheap credit has fueled a widening current account deficit and rising corporate debt levels – alongside real GDP growth that has been among the fastest in the world. Stabilising the lira could be positive for President Recep Tayyip Erdogan’s election prospects as the snap vote he called in June approaches.

Source: Markit, Bloomberg, Emirates NBD Research

Source: Markit, Bloomberg, Emirates NBD Research

US treasuries closed lower with the curve steepening. Yields on the 2y UST, 5y UST and 10y UST closed at 2.48% (+1bp), 2.83% (+1bp) and 3.02% (+2bps).

Regional bonds continue to follow moves in benchmark yields. The YTW on the Bloomberg Barclays GCC Credit and High Yield index gained +4 bps to close at 4.52% while credit spreads widened by 2 bps to 174 bps.

In terms of rating action, Fitch upgraded Ras Laffan to AA- from A. The outlook is negative, reflecting the negative outlook on Qatar.

USD continued to add to April’s gains on Wednesday, the Dollar Index rising 0.53% over the course of the day to close at 91.251. The most notable gains were against EUR and JPY with EURUSD falling 0.59% and USDJPY rising 0.56%. This move takes EURUSD below the 100 day moving average (1.2217) for the first time since December 2017. Currently trading at 1.2176, should EURUSD break below the 76.4% one year Fibonacci retracement of 1.2150, a test of the 200 day moving average of 1.2008 is a possibility.

This afternoon, markets will be looking towards the ECB policy meeting, where the central bank is expected to keep monetary policy unchanged. With that said, investors will be scrutinizing President Draghi’s speech for any changes in language and communication and further hints on when the asset purchased program may be tapered.

Developed market equities closed mixed with the S&P 500 index adding +0.2% and the Euro Stoxx 50 index losing -0.8%. Mixed corporate earnings weighed on investor sentiment.

Most regional equity indices drifted lower with the Tadawul losing -1.0% and the DFM dropping -0.3%. Weak corporate earnings and profit booking appeared to have led Saudi equities lower. Banking sector stocks took the most hit with Al Rajhi losing -0.8%, NCB -1.25% and Samba -2.9%.

DXB Entertainments lost -8.4% amid reports that the stock will be removed from the MSCI EM index. DSI dropped -9.4% after news that the company is looking to raise capital by AED 500mn.

Oil prices closed higher yesterday as French President Macron speculated that the United States may withdraw from the nuclear deal with Iran. NYMEX WTI Crude Futures gained 0.52% to close at USD 68.05/bbl while ICE Brent Crude Futures closed 0.19% higher to reach USD 74.00/bbl. This morning, further gains have been realized and as we go to print, NYMEX WTI Crude Futures are trading 0.53% higher at USD 68.40/bbl while ICE Brent Crude Futures are trading 0.55% higher at USD 74.41/bbl.

Click here to Download Full article