Recent Search

Popular Searches

Markets will be preoccupied with political events today as the US House of Representatives will vote on whether to impeach President Donald Trump. A vote in favour of impeachment looks likely given the Democrat majority in the House but the president seems likely to be acquitted when he will have to face trial in the Republican controlled senate. While the immediate link to markets and policy isn’t explicit as a result of the impeachment proceedings, the process has riven parties in the US even further asunder and will make consensus on trade deals or non-political spending (defence, infrastructure) more challenging next year. Should Trump be acquitted by the Senate he will try to use the process as a way to motivate his base to win against a Democratic candidate in the 2020 election, keeping the current administration’s attitude toward trade entrenched for another four years.

Industrial production in the US rose by 1.1% m/m in November thanks to a spike in car manufacturing after strikes by GM workers came to a close. However, news from Boeing that it will cease production of one of its main product lines, the 737 Max, means industrial output is likely to dip in the new year. Elsewhere the JOLTS report showed that job openings increased even as the unemployment rate remains at historically low levels. There were 7.27m job openings in October, more than the market had been anticipating, while the quits rate remains near historic highs.

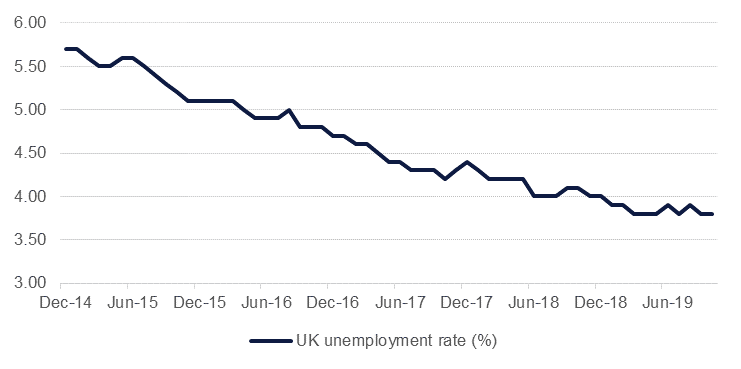

Labour markets in the UK continued to remain strong in the three months to October and actually showed an improvement in the unemployment rate to 3.8% compared with market expectations of 3.9%. Wage growth slowed, however, to 3.2% y/y from 3.7% although when stripping out bonuses wage growth was roughly level at 3.5%. The labour market figures are one area of strength for the UK economy—as high frequency PMI data has disappointed—and should help to keep the Bank of England from changing rates later this week. The market isn’t pricing in any change in rates imminently with only a 47.6% chance of a cut in November 2020.

Exports from Japan fell nearly 8% y/y in November, their 12th consecutive monthly decline. Japan has very much been caught in the China-US trade war cross fire as weakening demand in China in particular has weighed on Japan’s economy. Imports also plummeted—down by nearly 16%—meaning Japan’s trade deficit actually narrowed compared with market expectations.

Source: Emirates NBD Research

Source: Emirates NBD Research

US treasuries held within a narrow range as decent industrial production data weighed against news that Boeing would cease producing one of its main aircraft and tension builds ahead of the pending impeachment of US President Donald Trump. Markets generally look to be in a holding pattern until the end of the year with both equities and fixed income markets waiting for the other to move first and give a better signal on the direction for 2020.

Regional bonds continued to track moves in benchmark yields. Volumes continue to remain sluggish as we approach the year end.

Sterling remains in focus, having lost all of its post-election gains as the Conservative government is looking to be adopting a hardline stance on negotiating a trade deal with the EU. GBP has now moved back to a 1.30 handle against the dollar as Prime Minister Boris Johnson has made it clear that December 31 2020 will be the deadline to reach an agreement on trade with the EU, failing which the UK will move to WTO rules in its trading relationship. Most other majors were largely stable although AUD and NZD were weaker on the day.

TRY continued to weaken overnight, moving to within reach of 5.9 against the USD. Meanwhile, EGP NDFs held on to recent gains, having been bolstered by a positive shine to EM FX following the Phase One trade agreement reached by the US and China.

Developed market equities closed mixed as momentum from trade deal over the weekend faded. Further, reports of a possible 2020 hard deadline for a EU-UK trade deal also weighed on markets. The S&P 500 index closed flat while the Euro Stoxx 50 index dropped -0.7%.

Regional markets closed mixed as the focus remained on re-balancing of key broad indices over the next two days.

Oil prices kept their rally in place overnight, gaining a fourth day in a row. Brent futures settled up more than 1% at USD 66.10/b while WTI was just within reach of USD 61/b. Both benchmarks have slipped in early tade as the API reported a crude build of nearly 5m bbl. Official EIA is expected later this evening.

The new US energy secretary, Dan Brouillette, gave a strong endorsement of the country’s position as a new major oil player, saying the slowdown in production growth from the US was temporary. Brouillette also noted that OPEC producers aren’t as significant in determining global oil market conditions as they used to be thanks to the rapid rise in the US of both production and exports.

Edward Bell

Edward Bell