Recent Search

Popular Searches

Markets received a reminder that beyond the economic damage wrought by the Covid-19 pandemic trade relations between China and the US remain fraught. US trade adviser Peter Navarro stated to the press that the trade deal with China was “over” only to have to quickly backtrack and say the deal remained intact. US president Donald Trump also affirmed the deal still stands. US equity futures sank on the comments as did the Shanghai equity index and highly-trade exposed currencies like the Australian and Singapore dollars. Hostility between the US administration and China has been amplified by the coronavirus and the threat of a break down in trade relations remains real. Both sides have reportedly retaliated against each other’s’ media organisations, classifying them as foreign missions, rather than press.

The multiple crises in Lebanon continue to escalate, as the recent collapse of the pound on the parallel market has seen price growth accelerate to levels last seen in the wake of the civil war. The headline CPI inflation figure for May was 56.5% y/y, but even more concerning for both citizens and the embattled government alike was the 189.8% rise in food prices which will likely prompt a continuation of recent protests. The coronavirus pandemic and the closure of global tourism exacerbated the economic and political crisis already ongoing in Lebanon since October, and the currency has fallen to current levels of around LBP 5,500/USD, compared to the long-held official rate of LBP 1,507/USD.

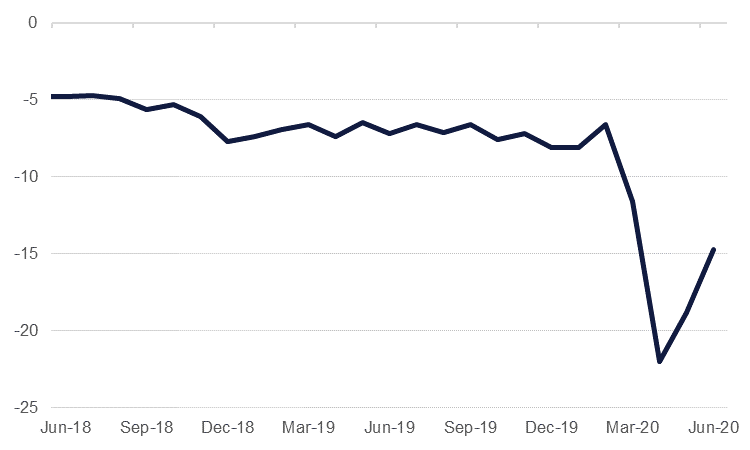

Consumer confidence improved this month in Eurozone economies as more and more countries eased their lockdowns. The index moved to -14.7 from -18.8 a month, the second monthly increase in a row. PMI data out later today will give a stronger sense of how strongly the improvement in the Eurozone has taken hold as consumption data for Q2 months still appears poor. As workers are protected by furlough schemes and the spread of Covid-19 comes under greater control, the chances for a boost in activity over the rest of the year appears strong, particularly if residents are reluctant to travel and instead spend more at home.

Source: Emirates NBD Research

Source: Emirates NBD Research

Treasuries closed lower as risk sentiment firmed up in latter half of the trading session. Yields on the 2y UST and 10y UST ended the day 0.19% (+1 bp) and 0.71% (+2 bps) respectively.

It is worth noting that the Federal Reserve’s overnight repo rate operations saw no takers for a second consecutive session and that Treasury bill supply was met with mixed results.

Regional bonds continued their unprecedented rally. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped from 3.07% to 3.05% and credit spreads tightened from 243 bps to 240 bps.

Moody’s assigned a Ba2 rating to the proposed benchmark sized instruments to be issued by DP World. The assigned rating is two notches below DP World’s Baa3 senior unsecured and issuer rating. Elsewhere, Fitch lowered the outlook on ratings of 9 Indian banks, including State Bank of India, to negative.

The dollar's advance at the end of last week has halted. The DXY index declined by over 0.60% to reach 96.995 off the back of a record increase in coronavirus cases in California. USDJPY traded sideways for the majority of the session, but has since made modest gains this morning and currently sits at 107.20.

The weakening dollar caused the euro to advance but the single currency met resistance at the 1.1270 level. Still the currency recorded gains of over 0.80% to trade at 1.1260. This comes despite Germany's coronavirus infection rate rising for a third day. Sterling was similarly positive, rallying to trade at 1.2475, marking an increase of over 1%. The AUD and NZD both made notable gains, increasing by over 1.20% and 1% respectively, with the former trading at 0.6915 and the latter trading at 0.6470.

Developed market equities closed mixed as investors returned their focus on green shoots popping over the economic outlook and largely shrugged off continued rise in new coronavirus cases. The S&P 500 index rose +0.7% and and the Euro Stoxx 600 index declined -0.8%.

Regional equities closed mixed. The DFM index added +1.6% after the government announced further easing measures. Air Arabia jumped +5.3% as restrictions were eased for inbound tourist traffic into the UAE. The Tadawul dropped -1.2% as investors remained cautious and markets lacked any local catalyst. Market heavyweights Sabic (-2.3%) and Riyad Bank (-2.7%) led the decline.

Oil prices extended gains to start the week with Brent futures up by 2.1% to settle above USD 43/b while WTI was up by 1.8% at USD 40.46/b. Contracts are mixed in early trade this morning but both showed their vulnerability to a resumption of the US-China trade war with Brent falling to nearly USD 42/b before recovering as US administration officials backtracked.

Edward Bell

Edward Bell