Recent Search

Popular Searches

Deals are in the air, or at least the possibility of them. China is said to be proposing a USD 1 trillion budget to boost imports from the U.S. over the next six years to eliminate the US-China trade imbalance. President Trump has agreed to hold a second summit with North Korean leader Kim Jung Un at the end of February. Trump is also offering a deal to Democrats over the border wall to end the government shutdown. Meanwhile, Chancellor Merkel is apparently hinting that a compromise might be possible to avert a harmful Brexit, signaling that the responsibility for getting the best possible deal rests with both the UK and the EU. Markets are bracing for UK PM May’s Brexit plan B to be announced tomorrow, so any indication that the EU may soften its stance should be helpful. All in all there is a mood of compromise on some of the most intractable issues facing markets, which should on the surface provide support for risk appetite at the start of the week. Ordinarily this might be expected to cause the USD to soften, the JPY to weaken and GBP to strengthen. However, the reality may be very different from the headlines, especially when the details begin to be seen. So short term moves in response to these weekend developments should be viewed cautiously.

For example the Democrats already appear to have rejected Trump’s latest overtures over the government shutdown, which will maintain a growing sense of alarm about the fate of economic growth. New York Fed head John Williams warned that the shutdown will progressively darken the economic outlook, indicating that quarterly growth could be cut by between 0.5 and 1.0% per quarter depending on how long the closure lasts. This will no doubt have implications for Fed policy as well, and may even eat into global growth which is already weakening. In terms of Brexit there are grounds to be skeptical for a number of reasons about whether a soft Brexit is now more likely following the government’s loss in Parliament last week. Much of GBP’s rally to date is probably more related to a short squeeze than any material change in how Brexit will eventually happen, which is likely to remain unclear even after May’s update on Monday. One possible announcement that might be thought would provide more clarity is whether she will announce a delay to the article 50 process, kicking the Brexit can further down the road. However, even this cannot be guaranteed to provide more certainty about how Brexit will ultimately end, and may potentially lead GBP down false alleyways in the process. China is likely to announce that Q4 GDP growth slowed sharply in the coming week which will underscore the urgency for an end to the US-China trade impasse. Meanwhile the ECB meeting will likely show its policymakers finally starting to acknowledge the growing downside risks that are looming. So beyond the promising weekend headlines at the start of it, the actual developments of the week may turn out to be much less reassuring.

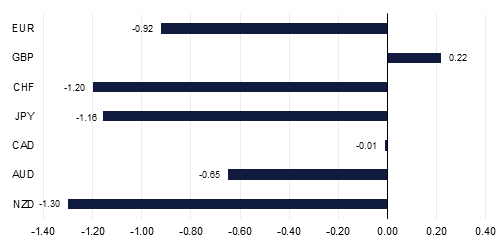

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

Click here to Download Full article