Recent Search

Popular Searches

.jpg?la=en&h=457&w=800&hash=662C121AA2568E790E973D4060A855E7)

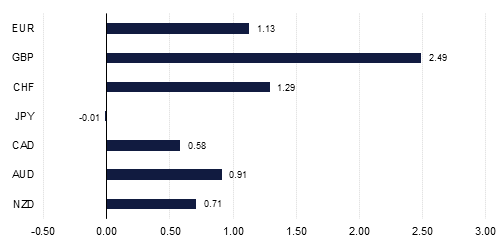

While the start of last week was characterized by optimism following the ‘partial’ trade deal between the U.S. and China and hopes of a resolution to Brexit, the beginning of this one is likely to be marked by disappointment. The ‘Super Saturday’ vote in the U.K. Parliament to withhold approval of the new Brexit deal until there is legislation to implement it, creates fresh uncertainty about the ultimate outcome of Brexit. The U.K. government will still seek to pass the legislation in time for the original October 31st deadline, but it is unclear if this will be allowed by Parliament, especially with the voting arithmetic weighted against the Prime Minister succeeding. The EU’s reaction to Johnson’s formal request for a delay is also not certain, leaving a high degree of uncertainty about whether PM Johnson’s Brexit deal will pass; whether there may still be a second referendum; or even whether the U.K. could still end up leaving the EU without a deal on October 31st. Against such a backdrop sterling is likely to give back some of the gains it made at the end of last week.

Uncertainty also remains over the U.S.-China trade talks, although weekend comments on the subject appeared to be encouraging. China and the U.S. made “concrete progress” in many areas and laid the foundations for signing of a “phased deal” at their latest round of talks to resolve the trade war, China's chief negotiator and Vice Premier Liu He said. China apparently intends to increase its purchases of US agricultural goods in accordance with the partial deal agreed last week, but Chinese officials also want the U.S. to cancel more of the tariffs imposed during the trade war. Also it does not seem as if the more substantive issues of intellectual-property theft, forced technology transfers, and complaints about Chinese industrial subsidies have seen much progress. U.S.VP Pence is due to give a policy speech on the administration's position on Thursday this week, which may shed light on some of these bigger issues. The U.S. Treasury’s bi-annual FX report will also be studied to gauge the U.S.Administration’s attitude towards China as a currency manipulator.

Central banks will likely remain accommodative in the current environment, with rate cuts possible in Turkey, China, Indonesia and Russia in the coming week. The ECB also meets this week, the final meeting with President Draghi at the helm, with the latest easing package likely to be left unchanged. The markets are pricing in about an 80% chance for a Fed rate cut at the end of the month, and it may leave the door open for further action in December. The USD will likely remain under pressure in anticipation of this, especially with U.S. economic data expected to be negatively affected by the ongoing GM strike which could see durable goods orders in September fall fairly sharply.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg