Recent Search

Popular Searches

In April 2018, GCC equity market rallied for a second consecutive month with the MSCI GCC Countries index adding +3.0%. The DFM (-1.4%) was a notable exception in what was a broad-based rally. The Tadawul and the Qatar Exchange added +4.3% and +6.3% in April 2018.

The focus of investors’ since the start of 2018 has remained on the possibility of inclusion of Saudi Arabian equities in the EM index of FTSE and MSCI. While FTSE decided to include Saudi Arabian equities in their EM index, the MSCI decision is scheduled for mid-June 2018.

The Tadawul saw inflows from foreign investors for a fourth consecutive month. Foreign investors bought stocks worth SAR 2.9bn amid continued focus on potential upgrade to the EM status. At the end of April 2018, foreign ownership of Saudi Arabian stocks crossed 5%. This is the highest level of foreign ownership since we started tracking the data.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

In April 2018, the DFM index saw outflows from foreign investors for a third consecutive month. Non-GCC investors were net sellers to the tune of c. AED 206.1mn.

The Qatar Exchange saw inflows for a second consecutive month. Foreign investors bought stocks worth QAR 358.5mn in April 2018. The decision of various companies to increase their foreign ownership limit to 49% played a part in inflows.

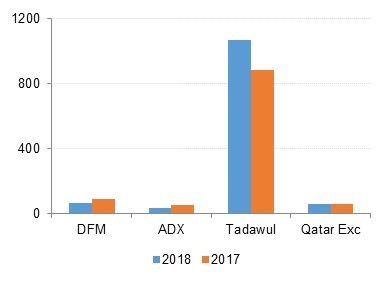

Trading volumes remained mixed across GCC equity markets. On a m/m basis the average daily value traded increased +18% on the Tadawul but declined elsewhere. The trend is similar on a y/y basis with turnover increasing +21% on the Tadawul.

Source: Emirates NBD Research

Source: Emirates NBD Research

Aditya Pugalia

Aditya Pugalia