Recent Search

Popular Searches

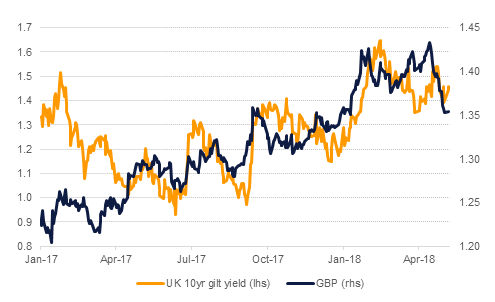

Most of the market’s attention will be on the UK where the Bank of England meets later today to announce its rate decision. Markets have virtually priced out any chance of a move at this meeting of the MPC and expect a rate hike later on this year. Recent data from the UK has been underwhelming and statements from Mark Carney, governor of the BoE, have not supported a case for rate hikes in the near term. Depending on his messaging the prospects for rate hikes in 2018 could be further weakened and also weigh on sterling.

The Reserve Bank of New Zealand kept interest rates on hold at 1.75%, as expected by the market. The new governor of the RBNZ Adrian Orr indicated the next move could be either up or down as the risks to the New Zealand economy are mixed. Inflation has been underperforming (just 1.1% in Q1) and the RBNZ cut its inflation forecast which the market has largely interpreted as a dovish move and the Kiwi dollar has sold off sharply.

Producer price inflation in China accelerated in April to 3.4% year on year from 3.1% in March. Higher commodity prices—particularly for oil and products—will have helped to push PPI up for the first time in seven months. Corporate earnings in China have been slowing as of late in response to increases in input costs but nevertheless higher PPI figures should send a reassuring message to central banks elsewhere that inflation in a core supplier to world economies is moving upward. Consumer prices (CPI) slipped slightly, however. CPI for April fell to 1.8% y/y from over 2% a month earlier. Core consumer prices—stripping out volatile food and energy prices—stayed level at 2%.

Producer prices in the US for April slipped to 2.6% y/y from 3% in March. Core PPI prices rose by 0.4% m/m, suggesting there is still some underlying upward cost pressures hitting US firms thanks to the softness of the dollar in the past year. While the dollar has appreciated in recent weeks it has come nowhere near close to erasing all of 2017’s declines. The recent spike higher in oil and other commodity prices will also help to keep PPI on the boil in the US.

Source: Eikon, Emirates NBD Research

Source: Eikon, Emirates NBD Research

Treasuries closed lower across the board amid concerns over supply and as investors positioned themselves ahead of the inflation data in the US. Yields on the 2y UST, 5y UST and 10y UST closed at 2.53% (+2 bps), 2.84% (+3 bps) and 3.0% (+3 bps) respectively.

Regional bonds continue to track moves in benchmark yields. The YTW on the Bloomberg Barclays GCC Credit and High Yield index gained +4 bps to close at 4.66% and credit spreads widened 1bp to 187 bps.

USDJPY continued to outperform on Wednesday supported by gains in U.S. Treasury yields. Of key technical importance as we approach the end of the week, are the daily closes of USDJPY which will give valuable insight on the most likely price action going forward. While the price remains above the 100 day moving average (108.62), daily closes above the one year 50% Fibonacci retracement (109.65) are likely to result in further gains towards the 200 day moving average (110.20). A break of this key level may prompt a retest of the 61.8% one year Fibonacci retracement of 110.85.

Should the 50 day moving average falter in the short term, the support at the 38.2% Fibonacci retracement of 108.44 may prevent further declines, however a breach and close of both these levels may result in further declines towards 107.20 (the 50 day moving average) in the coming week.

This afternoon, investors will be looking towards the Bank of England who are expected to keep interest rates at 0.50%, in contrast to a month ago where a 25bps hike was priced in by the market. Any dovishness or caution from the MPC may result in further pain for GBP which has fallen over 5% during the last month.

Developed market equities closed higher on the back of strength in energy sector stocks as oil prices rallied sharply. The S&P 500 index and the Euro Stoxx 600 index added +1.0% and +0.6% respectively.

Most regional markets closed lower as geopolitical tensions offset the sharp gain in oil prices. The DFM index and the Tadawul dropped -2.0% and -1.7% respectively. Banking sector stocks led the decline on the Tadawul with the Banking index losing -2.4%. On DFM, weakness in Emaar Properties weighed on the index as the stock lost -4.9%.

Spot prices soared yesterday in the first full day of market reaction to the US withdrawing from the JCPOA. Brent closed up 3.1% higher at USD 77.21/b while WTI followed and closed above USD 71/b. The backwardation in forward curves continued to widen for December spreads with the market now trying to assess exactly how tight it will be by the end of the year when the Iran sanctions have their full effect. OPEC messaging has been muddled in response to how they will deal with any shortfall in Iranian output with press reports citing an OPEC official that Saudi Arabia will not raise output alone.

EIA data for the week showed a decline in overall crude stocks of more than 2m bbl while US production rose to more than 10.7m b/d. The pace of gains in US output is accelerating, getting it closer to the EIA’s projections for this year.

Click here to Download Full article