Recent Search

Popular Searches

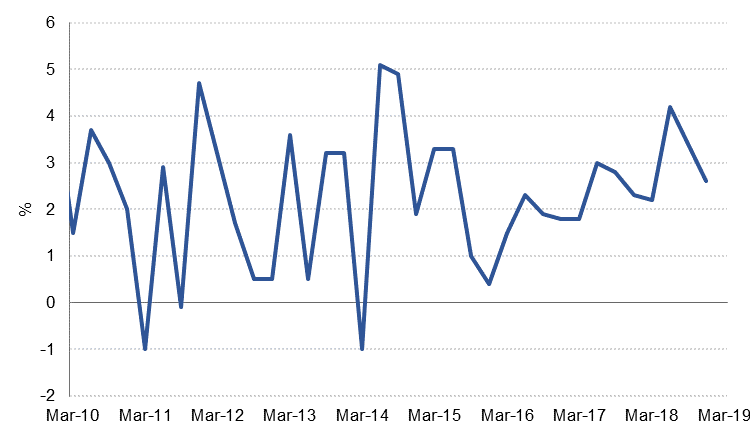

US President Donald Trump, in a speech on Saturday, called the US dollar too strong and blamed the Federal Reserve officials for not doing the right thing by continually raising interest rates and undertaking quantitative tightening. So far markets seem to have ignored the comment. On the data front, annualized GDP growth in the 4Q of 2018 came in at 2.6%, well below the average of over 3.2% in previous quarters but marginally better than expectations. The ISM manufacturing index in February fell to 54.2 from 56.6 in January. Based on the current weakness evident in personal spending as well as manufacturing and investments, GDP growth in the first quarter of 2019 is forecast to fall below 2% as it will also include the impact of the Federal government shutdown.

Halting the increase of U.S tariffs on Chinese goods that were scheduled to kick in on March 1st, President Trump has asked China to immediately remove all tariffs on U.S agriculture products, including beef, pork and soybean. China also seems to have stated that removing the duties on USD 200bn of Chinese goods was necessary to complete any trade agreement. However, the ongoing trade talks are believed to be nearing finalisation.

Chinese officials are scheduled to hold the National People’s Congress this week. Market expects downward revision to GDP growth forecast as well as announcement of some policy measures to stimulate economic growth.

In the Eurozone, headline inflation increased to 1.5% in February though core inflation actually fell slightly to 1.0% from 1.1% in January. The increase in headline inflation was almost entirely due to increase in energy prices and other volatile components. Also, while final February manufacturing PMI was confirmed to be in the contraction territory at 49.3, the unemployment rate fell slightly to 7.8% and services PMI is expected to be in the expansionary zone, thereby providing some comfort that domestic demand is holding up well. No policy change is expected at the ECB’s meeting on this Thursday, however, inflation and GDP growth forecast may be revised downwards again.

Stronger than expected GDP growth of 2.6% in Q4 last year and positive momentum in the US-China trade talks led the UST yield curve to steepen last week. Yields on 2yr,5yr, 10yr and 30yr USTs closed the week higher at 2.55% (+5bps), 2.56% (+8bps), 2.75% (+9bp) and 3.12% (+10bps) respectively. Across the pond, despite the weakening growth outlook, yield on Eurozone sovereign bonds also closed higher with 10yr Bund and Gilt yields closing the week up at 0.18% (+7bps w/w) and 1.29% (+12bps) respectively.

Notwithstanding the rising benchmark yields, GCC bonds had a constructive week with average yield on Barclays GCC bond index tightening 3bps to 4.27%, fuelled by circa 10bps tightening in credit spreads to 165bps on the back of stability in oil prices.

Primary market saw pricing of AA- rated Emirates Development Bank’s USD 750m 5yr bond at MS+98bps against order book of USD 3.4bn and pricing of Baa3/BBB- rated Almarai’s 5yr sukuk at MS+ 180bps, circa 45bps tighter than the initial guidance.

An increase of 0.27% resulted in EURUSD closing at 1.1366 last week, a second week of gains and the second time that the price has found support at the 200-week moving average (1.3338). Over the course of the week, the price has reached as high as 1.1420, before retreating lower. Support was consistently found at the 200-week moving average and while the price remains above this level, we expect further gains and maintain our Q1 2019 forecast of 1.15.

Last week’s 1.10% gain took USDJPY to 111.91, in a move that broke above many significant levels. Over the course of the week, the price broke above the 61.8% one-year Fibonacci retracement (110.73), formerly resistive 200-day moving average (111.34) and 100-day moving average (111.39) which is now acting as a support level. Furthermore, the 50-week moving average (110.67) which was broken last week has provided support and the 100-week moving average (110.79) was closed above for the first time in 2019. These developments are bullish for the USDJPY which finds itself close to many support levels. In the week ahead, a break of the 200-week moving average (112.37) and 67.4% one-year Fibonacci retracement (112.19) may trigger further gains towards the 113 handle.

Developed market equities closed mostly higher last week on the back of constructive tone of the US-China trade talks. S&P 500 and Dow Jones closed up by 0.69% and 0.43% respectively on Friday while FTSE 100 was up by 0.45%. Index provider MSCI announced its plan to include more of mainland Chinese equities in its EM index by including shares of some mid-caps and companies listed in the IT-heavy ChiNext Index. As a result, the weight of mainland Chinese shares in the EM Index will rise from about 0.7% to roughly 3.3%, thereby triggering possible capital inflows.

Regional equities had a mixed session yesterday, although the extent of the moves were relatively small. Dubai index closed marginally up and Abu Dhabi marginally down. Tadawul was circa half a percentage up.

Weak data out of both the US and China weighed on oil prices last week even as market surveys showed OPEC cutting production by more than required in February. PMI data in China showed a third consecutive month of contraction in the manufacturing sector in February while in the US the ISM index index fell to its lowest level since November 2016. Both benchmark oil futures fell last week with WTI losing 2.5% to close at USD 55.80/b and Brent closing at USD 65.07/b, down more than 3% over the five days.

OPEC achieved compliance of 101% with its production cut targets in February, according to a Reuters production surveys. Most of the heavy lifting was borne by Saudi Arabia (159% compliant), the UAE (123%), Kuwait (128%) and Angola (187%). However, Iraq remains an underperformer, achieving just 52% of its production cut target while compliance among other producers was less significant. OPEC came under pressure in the middle of the week when US president Donald Trump again targeted the producers’ bloc via tweet, calling on them to ‘relax’ and help to dampen oil prices. However, messaging from senior OPEC leaders, notably Khalid al Falih, Saudi Arabia’s energy minister, looks as though OPEC will keep cuts in place in the second half of the year as well. OPEC will message that it intends to keep cuts in place but as prices grind higher on a tightening market we expect to see output gradually increase by the end of 2019.

Click here to Download Full article