Recent Search

Popular Searches

Shorter dated government bonds sold off during the week as economic data remained strong and tone of major central banks turned less dovish. Though no rate hike is expected at the US FOMC meeting this week, yields on 2yr UST climbed 6bps to 2.12%. 2yr Gilts and Bunds yields also closed up to 0.62% (+6bps) and -0.56% (+5bps) respectively. UST curve gave up its steepening bias of the previous week as demand for 10yr USTs remained strong amid absence of higher inflation. Yields on 10yr and 30yr USTs closed at 2.66% (+1bp) and 2.91% (unchanged) respectively.

Economic growth in the world is in uptrend, positive outlooks on ratings are outweighing the negatives and default rates are falling. Oil prices have now spent more than a quarter at the above $60/b mark. In this environment, risk appetite for credit bonds remain high. CDS levels continued their grind tighter and are now 4bps lower over the month to 45bps for US IG and 2bps to 43bps for the Euro Main. Though cash corporate bonds suffer when benchmark yields rise, actual price of the global aggregate credit index rose over a point and half during the week as a result of tightening credit spreads.

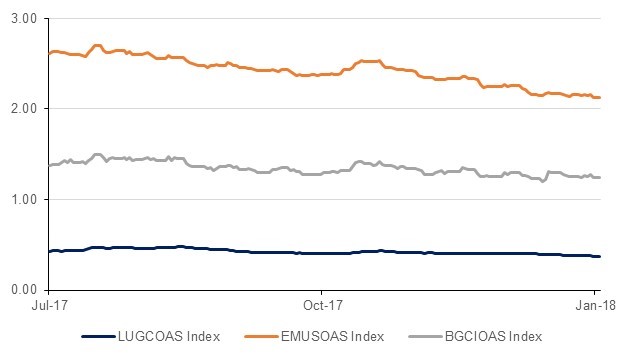

Regionally GCC bonds were stable with yield on Barclays GCC index range-bound at 3.87% and credit spreads tightening a bp to 145bps. CDS levels on the six GCC sovereigns tightened two to 6bps with 5yr CCS levels on Abu Dhabi, Saudi Arabia, and Qatar closing the week at 51bps (-2bps), 78bps (-6bps) and 91bps(-3bps) respectively as oil prices maintained strength.

Source: Emirates NBD Research

Source: Emirates NBD Research