Recent Search

Popular Searches

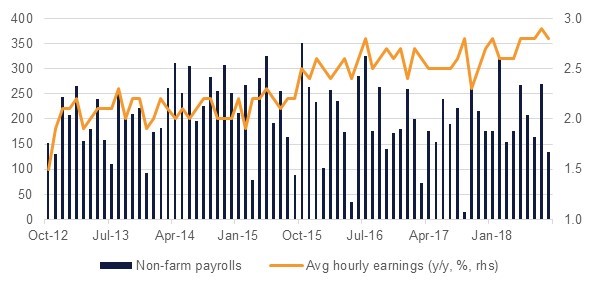

US consumer prices rose 0.5% month on month in September, helped by a spike in gasoline prices at the start of the month. The disruption to US oil refineries caused by hurricanes at the start of the month sent fuel prices higher but core inflation rose just 0.1% m/m, suggesting underlying prices remained muted. Overall core inflation has held steady at 1.7% y/y since May this year, giving some credence to the FOMC minutes out last week where some members were concerned that structural factors were at play in keeping price growth muted. However, the September report is a prime example of transitory factors that the Fed will be able to look past in their consideration of the health of the economy.

Retail sales and consumer confidence gave a much more upbeat view on the performance of the US in Q3. Retail sales rose 1.6%, largely driven by vehicle purchases as cars destroyed by hurricanes hitting the Gulf coast and Florida needed to be replaced. The University of Michigan’s consumer confidence survey surged for October to its highest level since January 2004 as consumers waved off the impact of hurricane damage. Good labour market conditions and a buoyant stock market all are playing into improved consumer sentiment going into the final months of the year.

Reports in the Financial Times over the weekend indicated Saudi Aramco was considering delaying the international portion of the company’s awaited IPO. Aramco has said that a ‘range of options’ was being reviewed which may include a private placement to strategic investors, possibly an Asian sovereign wealth fund. The Aramco IPO is meant to be the centrepiece of the National Transformation Program and a private placement may be an easier way for the company to provide finance for the NTP without the scrutiny needed by a full listing on the New York or London stock markets. There has so far been no announcement of delay to listing on the Tadawul, Saudi Arabia’s stock market, although the size and liquidity of the market is sharply lower than any of the main international markets.

The governor of Saudi Arabia’s central bank told the press the bank may raise the loan-to-deposit ratio at Saudi banks to help support the economy. The ratio was increased from 85% to 90% in February 2016.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

|

| Time | Cons |

| Time | Cons |

|

| Japan Industrial Production m/m | 08:30 | n/a | US Empire Manufacturing | 16:30 | 20.5 | |

Source: Bloomberg

US Treasuries ended the week on a positive note as the CPI data came in weaker at 2.2% y/y relative to expectations of 2.3%. Yields on the 2y USTs closed lower by 1 bps (w/w) at 1.49%, on 5y USTs by 6 bps (w/w) at 1.89% and on 10y USTs by 8 bps at 2.27%.

Regional bond markets continued the trend of following benchmark yields. The YTW on the Bloomberg Barclays GCC Credit and High Yield index dropped 2 bps on Friday to end the week 1 bps lower at 3.52%. However, credit spreads widened 6 bps to end the week at 157 bps.

Last week, the dollar index succumbed to its first decline in 5 weeks, falling 0.79% to close at 93.055. Of technical significance is that more declines were halted after support was found in the form of bids at the 200 week moving average (92.943), which the index has now closed above for a third successive week. While the weekly closes remain above this key level, the typical Q4 seasonality dollar strength has the possibility of re-exerting itself and we are more likely to see further gains, a theme which probably helped moderate dollar declines last week, despite the data being softer than expected. On the other hand, a break of this level could potentially catalyse a further retest of the one year low (91.011).

Elsewhere, sterling outshined all the other G-10 currencies last week with GBPUSD appreciating daily to end up the week 1.68% greater at 1.3286. Of note is that during the week, cable found supporting bids near the 50 day moving average (1.3142) prior to being hindered by and then ultimately overcoming resistance at the 76.4% one year Fibonacci retracement (1.3263). This development reaffirms our bullish sentiment on sterling and, unless UK information disappoints in the week ahead, we anticipate additional gains towards 1.34 in the short to medium term.

It was a subdued day of trading for regional equities with the average value traded lower by 25%. The Tadawul (-0.7%) led the decline as reports of a delay in international IPO of Saudi Aramco (see below) negatively impacting investor sentiment.

Almarai rallied +3.6% after reports that the PIF increased its stake to 16.32%.Elsewhere, Dana Gas closed lower by -3.8% as confusion over its participation the in arbitration proceedings continued.

Oil futures gained last week as geopolitical risk came back to oil markets. Brent futures closed the week up nearly 2.8% and WTI ended the week up nearly 4.4%. US president Donald Trump decided not to re-certify Iran as complying with the terms of the JCPOA, the international deal that has placed curbs on the country’s nuclear programme. The US Congress will now have to decide whether to impose new sanctions, a move opposed by the deal’s European partners and Russia and China, or to put other restrictions on Iran. In the immediate term there is no immediate change for Iran’s ability to export crude but the potential of sanctions being re-imposed could see buyers seek cargoes elsewhere.

Press reports that Aramco may delay the international portion of its IPO will create some volatility in oil markets as traders assess whether the Saudi ‘put’ in crude markets has been abandoned. Rightly or wrongly, the market was pricing in Saudi Arabia’s influence on OPEC supply management as being motivated by seeking a high valuation for Aramco. If that narrative begins to be questioned the market may begin to price in greater volumes of Saudi oil hitting the market, threatening the fragile rebalancing underway.

Futures market structures moved in opposite directions last week. The backwardation in Brent narrowed to USD 0.22/b while the WTI contango compressed to USD 0.28/b suggesting some improvement in the US market. Despite WTI rising at a faster rate last week, a gap of close to USD 6/b still persists between Brent and WTI.

Aditya Pugalia

Aditya Pugalia