Recent Search

Popular Searches

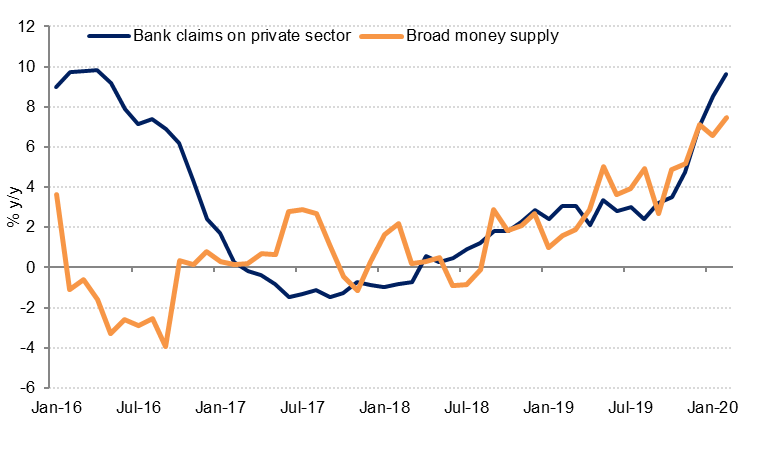

February monetary data for Saudi Arabia showed little impact from coronavirus-related disruptions to economic activity. Broad money supply growth accelerated to 7.5% y/y in February from 6.6% y/y in January, with demand deposits growing at the fastest rate since September 2015 at 9.5% y/y.

Private sector credit growth also accelerated in February, reaching 9.6% y/y, the fastest annual growth since April 2016. Government borrowing rose 3.5% m/m in February but the annual growth rate was steady at 20.8% y/y.

Source: Haver, Emirates NBD Research.

Source: Haver, Emirates NBD Research.

Net foreign assets at SAMA declined -USD 4.5bn to USD 492bn in February.

Point of sales (POS) transaction values declined -9.1% m/m, but monthly changes are volatile and seasonal. On an annual basis, POS transaction values were up nearly 35% y/y, the fastest rate of growth since 2012. However this growth was likely partly due to the 27.4% rise in the number of points where cards could be used for payments, and consumers opting for card over cash payments.

In our view, the recent rate of money supply and private credit growth is unlikely to be sustained as the full impact of the restrictions imposed on businesses and individuals are reflected in the data. Moreover, the recent sharp decline in oil prices will also have an impact on government deposits in the banking system as the government draws down existing deposits to meet its payment obligations domestically. While the government is likely to issue some external debt to finance this year’s wider budget deficit, the bulk of deficit financing will likely be through drawing on its reserves at the central bank and at commercial banks.

.png) Source: SAMA, Bloomberg, Emirates NBD Research.

Source: SAMA, Bloomberg, Emirates NBD Research.