Recent Search

Popular Searches

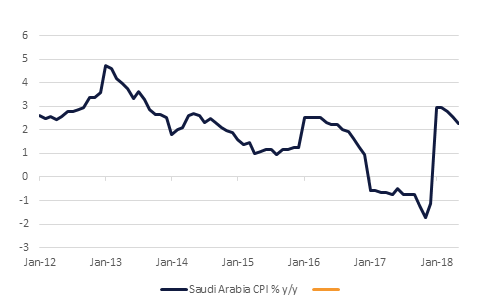

Inflation in Saudi Arabia eased to 2.3% y/y in May from 2.6% y/y in April. Housing and utilities costs declined m/m for the third consecutive month, while food prices also declined -0.7% m/m. Lower prices were also recorded in clothing & footwear, household equipment & furniture, transport and communication categories. Consumer inflation surged to 3.0% in January on the back of VAT and energy price hikes but has moderated since then.

The Central Bank of Egypt’s MPC will be announcing its monetary policy decision later today, with a hold of the overnight deposit rate at its current level of 16.75% the most likely scenario. There is room for another 100bps cut given the meaningful fall in inflation last month, the fact that upcoming inflationary pressures will be largely supply-side driven, and that private consumption growth has lagged to date. However, the committee has erred on the side of caution before and kept rates unchanged over concern about upcoming subsidy cuts, higher oil prices, and global tightening. These issues remain salient, and the pressure many emerging markets have been under over the past several months will also likely come into consideration, as the bank seeks to maintain portfolio inflows. Maintaining the backing of the IMF could also make a hold more likely, as it has been supportive of high interest rates in the past.

US durable goods orders fell by -0.6% m/m in May and excluding transportation they were down by -0.3%, both weaker than expected. In overnight news the Reserve Bank of New Zealand held interest rates steady at 1.75%, in line with expectations. However, the Governor did say that the RBNZ ‘are well positioned to manage change in either direction -- up or down -- as necessary’ in contrast to his last message that the rate would remain at its current setting ‘for some time to come.’, suggesting a softening of the bank’s tone. The European Council meeting and EU summit later today will focus on immigration and on the slow progress of Brexit negotiations.

Treasuries closed higher as the risk-off mood persisted. Yield on the 2y UST, 5y UST and 10y UST closed at 2.50% (-3 bps), 2.74% (-5 bps) and 2.82% (-5 bps).

Regional bonds closed higher as it received a boost from rally in Bahrain bonds following assurances of support from Saudi Arabia, UAE and Kuwait. The YTW on the Bloomberg Barclays GCC Credit and High Yield index dropped -8 bps to 4.60% and credit spreads tightened -3 bps to 195 bps.

S&P downgraded outlook on Dubai Investment Park to negative but retained the rating at BB+. The rating agency said the financial leverage has weakened following the company’s acquisition of remaining shares in Emicool and increasing capex.

USDJPY nudged higher overnight even as the rhetoric over trade became more heated again. The NZD weakened further to 2-year lows after RBNZ Governor left the option of cutting rates open after the Bank left monetary policy unchanged overnight. One of the main developments of the week has been the observation that the PBoC appears to have been guiding CNY lower, with Beijing thought to be viewing currency depreciation as a method for countering U.S. tariffs. The CNY has declined over the last week, and has now fallen by 3% over the last two weeks, returning USDCNY to 6.61 the highest levels since December 2017. This has coincided with steepening declines in Chinese equity markets and has given rise to softness in other regional FX markets.

Developed market equities closed mixed as trade fears continued to weigh on investor sentiment. The S&P 500 index dropped -0.9% while the Euro Stoxx 600 index added +0.7%. Sharp gain in oil prices have helped contain losses in equity markets.

Regional equities traded mixed with the DFM index losing -0.7% and the Tadawul adding +0.2%. Drake & Scull closed limit down for a third consecutive trading session and Emaar Properties (-1.8%) closed below AED 5.0. Union Properties gained +4.5% after the company said it has no exposure to Abraaj.

Oil prices got another lift from a strongly bullish EIA report. Total inventories in the US fell nearly 10m bbl while crude output held steady. Demand indicators, measured by refinery utilization, also look very healthy as we head into the seasonally stronger summer months. WTI continued its upward climb, adding more than 3% to close at USD 72.76/b while Brent gained 1.7% to move nearer to USD 78/b.