- Saudi Arabia has hosted a virtual meeting of the G20 leaders’ summit where the inevitable focus has been on how to coordinate public health responses to the Covid-19 pandemic along with developing a plan to offset the economic damage caused by the pandemic, particularly among emerging economies. So far there has been an initial draft pledging members of the G20 to ensure ‘affordable and equitable’ access to any vaccines and public health responses for coronavirus.

- The IMF has reached staff-level agreement to pass Egypt on the first review of its new 12-month stand-by arrangement. The Fund noted that Egypt’s economy ‘has performed better than expected despite the pandemic.’ In the current fiscal year – ending June 2021 – the IMF forecasts real GDP growth of 2.8%, in line with our own forecast.

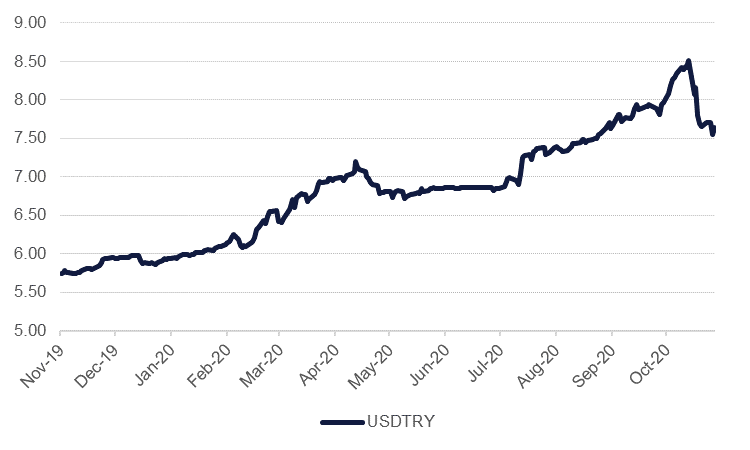

- Turkey’s central bank hiked the one-week repo rate by 475 basis points to 15.0% at its Thursday meeting, the first under new governor Naci Agbal. The MPC’s communiqué also pledged a simplification of monetary policy, with all funding set to be provided through the main policy rate. Markets reacted favourably to the decision, and the lira strengthened to a two-month high against the dollar on Thursday.

- The US Federal Reserve will return to the Treasury department funds used for emergency lending programmes that are set to expire at the end of this year. Several of the programmes, such as the main street lending programme or funds to buy up corporate debt actually had limited uptake and provide more of a confidence boost to financial markets than substantial liquidity. The Fed may now need to augment its existing programmes, such as asset purchases, in order to continually support the economy.

- The UK managed to clinch a trade deal with Canada, replicating the conditions the British economy had under a broader EU-Canada trade deal. The UK had previously secured a trade deal with Japan while negotiations are underway with many other markets to help offset the impact of the UK leaving the EU at the end of the year. Market expectations are high that a Brexit deal between the UK and EU will be secured soon, possibly before the end of the month.

USDTRY - 1yr

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Fixed Income

- Benchmark bond markets rallied last week as signs of weakening economic conditions for Q4 spread even as positive vaccine test results give some hope that the Covid-19 pandemic could be brought under control at some point 2020. Yields across the UST curve fell last week with the 2yr UST down by 2bps over the week to 0.1573% and the 10yr giving up 7bps to settle at 0.8243%.

- Emerging market bonds managed to rally even as there was a shift in risk appetite. US dollar denominated EM bonds gained 0.45% while spreads over comparable USTs closed slightly tighter.

- Saudi Arabia’s finance minister, Mohammed al Jadaan, said the country wouldn’t tap international bond markets again this year and would instead rely on domestic borrowing. The current Saudi 10yr USD bond rallied 0.14% last week with the yield slipping to just over 2%, roughly 122bps higher than comparable USTs.

FX

- Major currencies gained last week as the USD remained in a downtrend. The DXY index fluctuated with varying intraday volatility between 92 - 92.8 before settling at 92.392. Concerns surrounding Covid-19 cases and the US Treasury's refusal to extend the Fed's lending facilities weighed on the greenback. USDJPY recorded a much steadier decline, falling from highs of over 105 before closing at 103.86

- The GBP reached a two-month high of 1.3312 and closed at 1.3280, reacting to positive sentiment regarding Brexit negotiations. Both the EUR and the AUD closed moderately higher at 1.1857 and 0.7303 respectively, whilst the NZD reached a two-year high of 0.6951 before settling at 0.6931.

Equities

- The positive news regarding the Moderna vaccine development released on Monday pushed most global equity indices to another week of gains. This was, however, a more muted upwards move compared to the previous week following news about another vaccine being developed by Pfizer and BioNTech. In Europe, the CAC was the primary mover, gaining 2.2% w/w, while the FTSE 100 and the DAX added 0.6% and 0.5% respectively. In Asia, the Shanghai Composite gained 2.1%, the Hang Seng 1.1% and the KOSPI 2.4%.

- The picture in the US was more mixed, and while the NASDAQ gained 0.2% w/w, the Dow Jones (-0.7%) and the S&P 500 (-0.8%) both declined over the period. Many US states, including economically important California, imposed new restrictions on activity last week in the face of rapidly rising Covid-19 cases. In addition, moves by US Treasury Secretary Steven Mnuchin at the end of the week to end a number of Federal Reserve lending support programmes has raised liquidity concerns, and the bulk of the US equity losses came on Friday.

Commodities

- Oil futures rallied a third week running, bolstered by further successful vaccine results even as near term conditions worsen as more economies impose lockdown conditions. Brent futures for January rallied 5% and closed out at USD 44.96/b, the highest close for the front month contract since August. WTI futures (January expiry) also gained 5%, closing out at USD 42.15/b.

- The UAE’s energy minister affirmed his nation’s commitment to OPEC, after market reports indicated the UAE could threaten to leave the producers’ bloc. OPEC+ holds its next meeting on Nov 30 – Dec 1 to decide whether to proceed with production increases as planned from January or to rollover existing levels of output.

- Industrial metals were higher across the board on the hope that they deployment of a vaccine in 2021 could allow economic activity to get back to normal. Copper (3mth LME forwards) settled at USD 7,277/tonne, its highest level since mid-2018. Gold prices ended the week slightly lower despite a pop toward the end of trading on comments from Secretary Mnuchin that the Treasury still had “capacity” to support the economy. Spot gold settled at USD 1,871/troy oz, a w/w drop of around 1%.

Click here to Download Full article

Edward Bell

Edward Bell