Recent Search

Popular Searches

Saudi Arabia has lifted its ban on women driving, with women expected to be issued licenses from June 2018. This is a significant development not only on social liberalisation but also in terms of economic reform. Increasing female participation in the labour force is one of the aims of the Vision 2030 program, but this was always going to be difficult given the social norms in the Kingdom. The decision to allow women to drive indicates that the authorities remain committed to implementing their ambitious reform agenda, despite an apparent slowing of economic reform momentum in recent months. The government is expected to publish a revised version of its National Transformation Plan in October, which is likely to extend the deadlines for achieving some of its targets.

Overnight economic data releases out of the US were mixed. The Richmond Fed Manufacturing index rose to 19 vs expectations of 13 while New Home Sales came in at 560k vs 571k in the previous month. Conference Board consumer confidence index fell from 122.9 last month to 119.8. It still remains close to its sixteen year high even after Charlottesville, the nuclear threat from North Korea, and two major hurricanes. This underlines just how resilient the household sector is and augurs well for consumption growth in the rest of the year.

Federal Reserve Chair Janet Yellen said gradually raising interest rates is the most appropriate policy approach amid higher uncertainty about inflation and that it would be imprudent to keep monetary policy on hold until inflation is back to 2%. In addition, she said the Fed should also be wary of moving too gradually. In another news, President Trump’s upcoming tax plan is likely to propose a cut in corporate tax rate from 35% to 20% and highest individual tax rate from 39.6% to 35%. The implied probability of a rate hike in December has now crossed 70%.

|

| Time | Cons |

| Time | Cons |

| US Durable Goods Orders | 16:30 | 1.0% | US Pending Home Sales | 18:00 | -0.5% |

Source: Bloomberg

Yields on UST curve were lifted upwards in response to hawkish comments from the Federal Reserve Chair, Janet Yellen. 2yr, 5yr and 10yr treasury yields closed at 1.44% (+2bps), 1.86% (+2bps) and 2.24% (+2bps) respectively. Most of the sovereign bonds in Europe followed UST move with yields on 10yr Bunds closing a bp higher at 0.41% though Gilts were unchanged at 1.33%.

Credit spreads in the region were largely unchanged with CDS levels on GCC sovereigns moving sideways and option adjusted spreads on GCC bond index remaining stable at 138bps though total yield increased by a bp to 3.32% on the back of benchmark yield widening. On the corporate development front, Commercial Bank of Qatar plans to sell its 40% stake in Abu Dhabi listed United Arab Bank (mkt cap AED 1.99bn) as part of its restructuring.

In the primary market, KSA is expected to price its three-part bond offering before the end of the week. Guidance on March 2023 bonds is at T+130bps, on March 2028 bonds is at T+165bps and that on the October 2047 is at T+200bps. Also Emirates NBD is targeting to raise funds via 10 yr AUD denominated benchmark sized offering at circa MS+207bps.

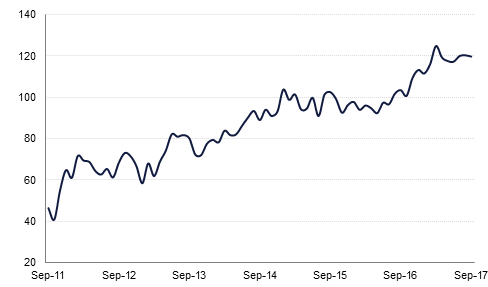

This morning USD trades firmer with the Dollar Index rising to 93.052 and testing the resistive trend line of the daily downtrend that has been in effect since 10 April 2017. Of significance is that the index was able to achieve a break and daily close above the 50 day moving average of 92.912 on Tuesday. If able to maintain above these levels, the opportunity to break out of the downtrend remains a possible scenario and the index could climb towards the 23.6% one year Fibonacci retracement of 94.03.

Absence of additional rhetoric on the North Korea issue and expected comments from the central bankers gave little impetus for change in the equity bourses. Wall street closed flat overnight and European shares showed little change. S&P 500 had slight bid bias, closing up by 0.01% while Euro Stoxx 50 closed down by 0.04%. Equities in Asia are also trading mixed this morning. Hangseng is up 0.43% amid declining Nikkei at -0.37%,

It was largely a dull day of trading for regional equities with the exception of Qatari equities. The Qatar Exchange added +1.4%, the largest single day gain in over two months. The rally was broad based with all stocks finding support at current levels.

Profit taking took some of the fizz out of oil prices yesterday after their sharp rise to begin the week. Brent futures are still trading with a USD 58/b handle while WTI is holding above USD 52/b. The backwardation at the front of the Brent curve continues to tell a sign of a tightening market while good levels for refinery margins are helping to support demand. EIA data will be released this evening which is expected to show another weekly build in crude stocks and draws across the rest of the barrel.