Recent Search

Popular Searches

Saudi Arabia approved a 2020 budget broadly in line with the pre-budget statement released last month. The budget makes provision for both lower revenues and expenditure, with the cuts expected to come mainly from current spending. While lower government spending poses downside risks to growth next year, this may be offset by increased domestic investment by PIF. The preliminary budget deficit for this year was estimated at -4.7% of GDP, wider than had been planned by the authorities but lower than our own forecasts, and this will be financed by foreign and local bond issuance according to Finance Minister Mohammed Al Jardaan. Next year the deficit is expected to reach -6.4%. Non-oil activity has been underpinned by fiscal spending this year with the IHS Markit PMI reading reaching 58.3 in November, the highest reading since August 2015.

Economic data out of the Eurozone was a little bit encouraging at the start of this week. Germany’s trade balance widened to EUR 21.5bn in October, up from EUR 21.2Bn the previous month, with exports unexpectedly rising by 1.2% m/m. The Eurozone also saw a slight increase in economic confidence, with the Sentix Investor Confidence Index rising to 0.7 in December, up from -4.5 in November and the second positive result in 2019.

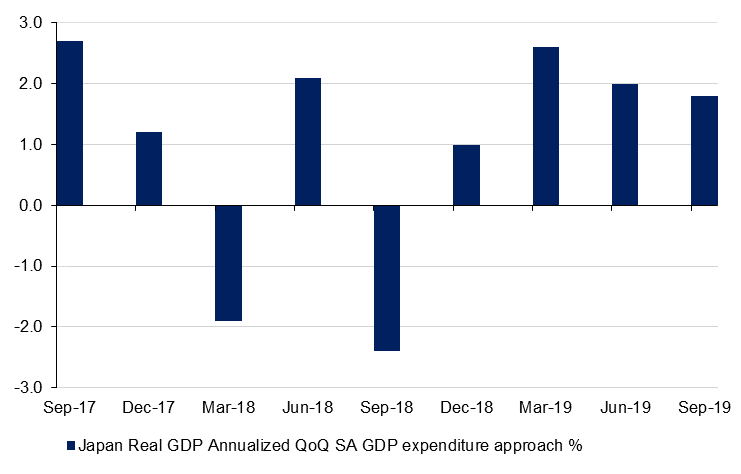

Meanwhile the final release of Japan’s Q3 2019 GDP was also a little more hopeful showing that GDP rose 1.8% annualized q/q, up from the previous estimate of 0.2% and higher than the market consensus for an upward revision of 0.6%. The faster than expected expansion can mainly be attributed to a stronger capital investments and greater private consumption ahead of October’s sales tax hike. The news came after the Japanese government announced a fiscal stimulus package worth USD121bn.

Source: Emirates NBD Research

Source: Emirates NBD Research

Treasuries closed marginally higher as investors moved to a holding pattern ahead of the Federal Reserve meeting and key trade deadline on 15 December. The curve flattened with yields on the 2y UST and 10y UST closing at 1.61% (flat) and 1.81% (-2 bps) respectively.

Regional bonds continued to remain in a very tight range as investors avoid taking position heading into the year-end. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped -1 bp to 3.23% and credit spreads tightened 1 bp to 146 bps.

The pound remained in the spotlight yesterday as two new polls showed the Conservative party extending its lead over Labour ahead of the general election on Thursday, helping GBP to extend its recent rally. The AUD and the NZD rose this morning after Chinese CPI inflation rose to a 7-year high in November, while producer prices continued to decline. The consumer price index rose 4.5% last month from a year earlier, following a 3.8% gain in October. The median forecast was for a 4.3% increase. Factory prices fell 1.4% on the year however, slower than the 1.6% drop in October.

Developed market equities drifted lower as investors exercised caution ahead of key events later this week. The S&P 500 index and the Euro Stoxx 600 index dropped -0.3% and -0.2% respectively.

Regional equities closed mixed. The Tadawul continued its positive run as it seeks to build on the momentum from a well-subscribed IPO of Saudi Aramco. Elsewhere, the DFM index dropped -0.4% on the back of weakness in Emaar-related names.

Oil markets weakened at the start of the trading week as trade war anxieties outweighed the impact of OPEC+ agreeing to deeper production cuts. Brent futures fell by 0.2% to settle at USD 64.25/b while WTI moved closer to a USD 59/b handle, down by 0.3%.

Suhail al Mazrouei, the UAE’s energy minister, said that OPEC + producers would be happy with prices in a range between USD 60-80/b and that the producer bloc’s objective was to create a balanced market.

Click here to Download Full article