Recent Search

Popular Searches

The official Saudi estimates for the 2017 budget put the deficit at -SAR 230bn or -9.0% of GDP. This is better than our -12.8% of GDP forecast and down from -13.6% in 2016. Both oil and non-oil revenues were higher than we had expected at SAR 440bn and SAR 256bn respectively. Expenditure came in at SAR 926bn last year, about 4% higher than the official budget and just 2.5% lower than our forecast.

Next year’s budgeted expenditure is 5.6% higher than in 2017 at SAR 978bn. Current spending (wages, goods and services, interest expenses) is forecast to rise by 3.6% to SAR 773bn (nearly 80% of the total budget). Capital spending is forecast to rise by nearly 14% y/y in 2018.

In addition, the government has announced a further SAR 133bn in ‘off budget’ spending that will be financed by the Public Investment Fund (PIF) and National Development Funds (NDFs). PIF will set aside SAR 83bn for ‘mega infrastructure, real estate and transportation’ projects; this is likely to include funding for the new city, Neom that was announced at the investment summit in November. NDF funds of SAR 50bn will be used for housing and other initiatives to stimulate private sector growth, create jobs and boost efficiency. Overall, public sector spending is expected to exceed SAR 1.1tn (USD 296bn) in 2018, making it the biggest ever fiscal stimulus in the Kingdom.

.png) Source: Bloomberg, Ministry of Finance, Emirates NBD Research

Source: Bloomberg, Ministry of Finance, Emirates NBD Research

In terms of the sector allocation of budget funds, the largest share of the SAR 978 budget will go to defence spending for the first time in 2018. Combined defence and security services spending is set at SAR 311bn (nearly one-third of the total budget) next year, down from actual 2017 spending of SAR 334bn but higher than was budgeted for this year. Health & social development and economic resources have also been given bigger budget allocations in 2018. Education and public programs have seen their budget allocations decline from 2017.

The budget makes provision for SAR 492bn in oil revenue and SAR 291bn in non-oil revenues, with total budget revenue pencilled in at SAR 783bn, up 12.6% y/y. However, we estimate the budget projections assume an average oil price of USD 50-51pb next year, which is lower than our USD 56pb forecast for Brent. Using our oil price forecast, we estimate oil revenue will be SAR 543bn and total budget revenue at SAR 806bn, up nearly 16% y/y.

As a result, we project a smaller deficit than the official budget at -SAR 172bn (excluding off-budget PIF and NDF spending). Based on our GDP estimates, this would see the deficit narrowing to around -6.3% of GDP next year, despite higher spending. If the PIF and NDF funds are included, we estimate the deficit would reach -11.1% of GDP.

We expect the budget deficit to again be financed through a mix of debt issuance and drawing down reserves. The budget statement indicates that 12% of the budget (SAR 117bn) would be financed by debt, and the balance from accumulated reserves.

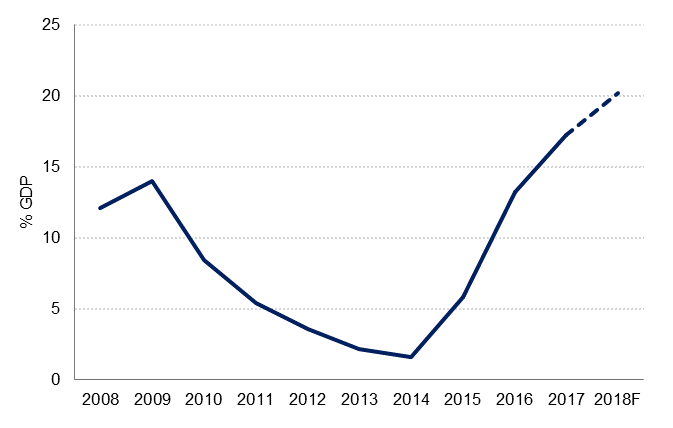

The stock of public debt stood at SAR 438bn at the end of 2017, below our SAR 470bn forecast. With an additional SAR 117bn of new debt issued next year, the stock of public debt would rise to SAR 555bn (20% GDP) by end-2018.

Privatisation proceeds could also be used to cover a portion of the financing requirement, which based on our revenue projections, would be around USD 45bn. Aside from the planned Aramco stake sale (where the proceeds have been earmarked for investment by PIF), there are number of other state assets that could be sold to raise additional funds. The economy minister indicated that assets in the utilities and grains sectors had made significant progress in terms of preparation for privatization, but there are other assets in the education, healthcare and transport sectors that could potentially be sold as well.

Source: Haver Analytics, Bloomberg, Emirates NBD Research

Source: Haver Analytics, Bloomberg, Emirates NBD Research

The authorities have presented the 2018 budget as an expansionary one that will boost growth in the non-oil sectors, create jobs and invest in the future productive capacity of the economy.

The strategy is commendable: following two years of subsidy reform and spending cuts, the government is using some of the fiscal room it now has (higher oil prices, substantial accumulated reserves) to slow the pace of further fiscal adjustment. The aim is no longer to achieve a balanced budget by 2019, which would potentially have meant another year of recession in 2018. By slowing the pace of deficit reduction, the authorities are able to boost non-oil growth next year and offset further subsidy reforms with cash grants to qualifying households, and also invest further in much needed infrastructure.

However, we have seen large budgets before. In 2014, total budget spending also exceeded SAR 1tn, with a significant chunk of this allocated to capital spending. We would argue that the effectiveness of public sector spending is just as important as the sum of money that is disbursed, and improving this will require structural changes in the way ministries and funds are administered and controlled. The crown prince has taken measures over the last 18 months to improve oversight and efficiency of government spending, but it will take some time to judge whether these measures have been sufficient.

We had already anticipated higher expenditure in 2018 as oil prices recovered, and we had pencilled in a 2.5% GDP growth forecast based on both higher oil (1.5%) and non-oil (3.5%) sector growth in the Kingdom. Given the higher than expected rise in public sector spending next year, we have revised our GDP growth forecast higher to 2.8%, with the increase coming entirely from non-oil sector expansion.

Click here to download the report.