Recent Search

Popular Searches

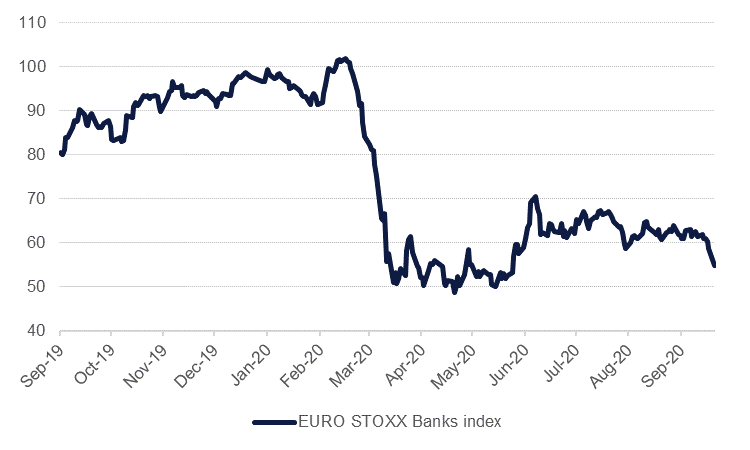

Financial markets were shaken overnight as investor concern over rising Covid-19 cases, particularly in Europe, weigh on the growth outlook while a report from a group of investigative journalists focusing on banks hit financial stocks in particular. New restrictions on the hospitality sector in England have been imposed which may choke off a nascent recovery there which had been benefitting from government support. So far the British government appears reluctant to impose another stringent nationwide lockdown but a rising number of Covid-19 patients may mean that more restrictions are on their way.

Fed Chair Jerome Powell provided his testimony ahead of his meeting with the House Financial Service committee, noting that the US economy had shown “marked improvement” but that employment and broader activity still was far below pre-pandemic levels. Powell also seemed to call again on fiscal policy to do some of the lifting for the economy, saying that policy actions needed to be taken at “all levels of government.” Powell delivers his comments to the committee today where he is likely to be challenged on what the Fed will be looking for as far as unemployment levels before it can begin normalizing policy.

Lebanon’s inflation continued to accelerate in August, according to the latest figures from the CAC. Headline CPI price growth rose to 120.0% y/y, up from July’s 112.4%, while food prices continued to rise at an alarming rate, hitting 367.2%, up from 336% the previous month. These latest figures will have captured the effect of the blast in Beirut on August 4, the disruption caused by which will have exacerbated the inflationary effects of the currency collapse ongoing through the course of the year.

Source: Emirates NBD Research

Source: Emirates NBD Research

Treasury markets rallied to start the week as investors swung heavily to risk-off positions. Anxiety over rising case numbers and a hit to banking stocks in particular helped USTs gain across the curve with yields on the 2yr UST holding roughly steady but bigger drops on longer dated bonds: 10yr UST yields fell almost 3bps to 0.6658% although did drop below 0.65% at one point.

High yield and EM bonds couldn’t escap the sell-off in risk assets with the EM USD bond index down 0.55% while spreads over USTs jumped to their highest level since July.

Risk aversion was the primary theme on Monday amid concerns about rising Covid-19 cases, particularly in Europe, driving demand for safe haven assets. The USD benefitted the most from this sentiment, as its DXY index advanced by 0.70% and trades at 93.570, a break above the 50-day moving average of 93.475. This helped USDJPY rebound from session lows of 104 swiftly, but remains largely unchanged from last week's closing price at 104.57.

Broad-based USD strength has had an adverse effect on major currencies. The EUR declined by -0.63% and trades at 1.1766, just below the 50-day moving average of 1.1772. GBP slipped by -0.78% to reach 1.2790 amid a dismal market mood in the UK. Both the AUD and NZD suffered heavy losses as well, declining by -0.96% and -1.28% to trade at 0.7220 and 0.6673 respectively.

Equities underwent significant pressure yesterday, with all major global indices closing lower on the day, and the rout extending to Asian markets this morning. European markets were amongst the worst-hit, as fears over renewed lockdowns, and the potential effect on demand, wiped 3.4% off the UK’s FTSE 100, 3.7% off France’s CAC, and 4.4% off Germany’s DAX. Travel stocks were particularly affected, while supermarkets and food delivery firms were among the only risers.

On both sides of the Atlantic, banking stocks were hit by the FinCEN investigation into illegal money transfers. In the US, the S&P 500 (-1.2%) and the Dow Jones (-1.8%) both saw greater losses yesterday than the tech-heavy NASDAQ (-0.1%) suggesting that it was primarily fears over renewed lockdowns driving the selling yesterday, with firms offering in-home entertainment having managed to secure gains.

Oil prices took a beating in the risk-off move, declining more almost 4% in Brent futures to settle at USD 41.44/b while WTI was off more than 4.3% to close below USD 40/b. Markets will also be increasingly pricing in the potential for Libyan crude to return to markets as some export terminals will reopen. However, Libyan has a long way to go to restore output back to its 1.2m b/d level from the start of the year: currently Libya is producing at around 100k b/d.