Recent Search

Popular Searches

After a week that began with talk of nuclear war and ended with Hurricane Irma, investors are not surprisingly struggling to deal with the deluge of risks that are now confronting them on an almost daily basis, and to price them correctly. With the summer behind us but with only ten days of September gone, the challenge of anticipating and calibrating the key factors that will define where markets go through the rest of this year is already immense. Geopolitical risks on the Korean peninsula and natural disasters across large areas of United States and the Caribbean may be at the extreme ends of the scale in terms of what markets usually think about, but it is perhaps no exaggeration to say that the most difficult challenge they face today is in making sense of events in Washington DC and what they will mean for fiscal policy, growth and interest rates.

Hurricane season will bring with it lower growth in the near distance, but this will arguably be followed by firmer growth once the recovery effort begins in earnest. Inflation may also get a temporary lift, but all of this adds to uncertainty about the appropriate level of interest rates. President Trump added his fair share to exacerbating market confusion, by overriding his Treasury Secretary Mnuchen and agreeing to a proposal from the opposition Democrats to extend the $19.3 trillion debt ceiling for a further three months.

While the avoidance of debt cliff at the end of this month might normally be seen as something to be welcomed, its postponement for just three months to the year-end is arguably a much worse scenario for markets and for the economy. Markets would rather get the issue over with now than have it hanging around for the rest of the year. It will only extend the period of uncertainty among investors, corporations and consumers; it will complicate the process of delivering meaningful tax reform; and it will reduce the chances of other key legislation being achieved this year and next.

All of this at a time when the Fed is going through its own institutional challenges, with the resignation of Vice Chair Stanley Fischer last week taking the number of vacant Fed Board positions to four. Not surprisingly the messaging from Fed officials of late has become more mixed leaving the chances of a year-end rate hike by the FOMC now much less certain.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

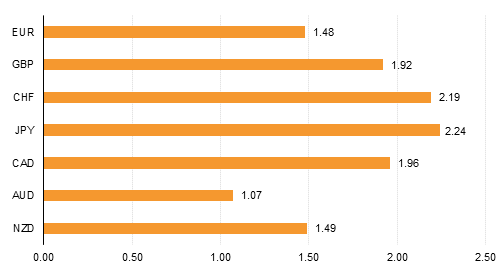

With bond yields falling this is not surprisingly taking its toll on dollar sentiment causing a decline against all the major currencies last week (see chart on front page).

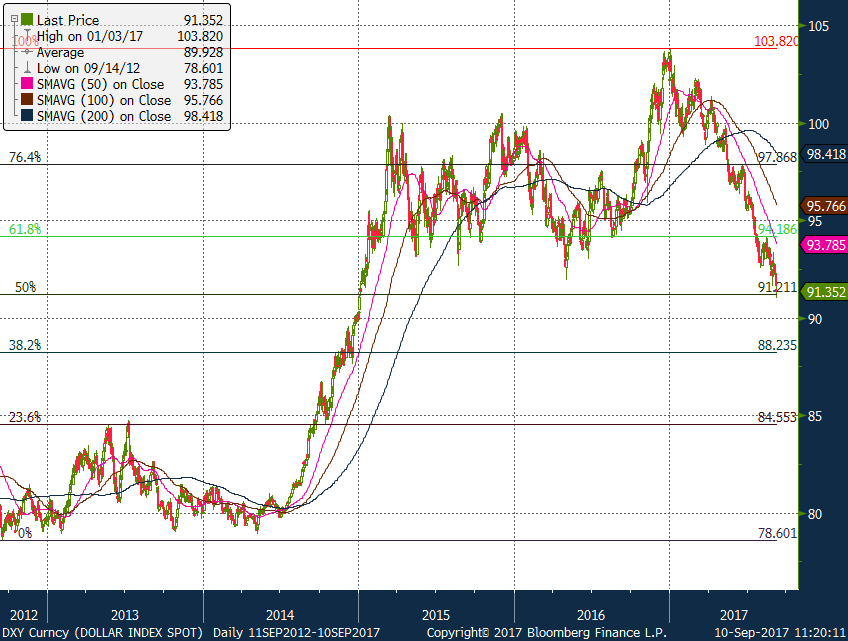

Indeed the Dollar Index fell 1.6% over the course of the week, falling from 92.81 to 91.33 and even falling as low as 91.01 during Friday’s trading session. These levels have not seen since 2 Jan 2015 and contribute to technical developments which leave the index looking vulnerable to greater declines. We had mentioned in our 20th August edition of the FX Week that despite earlier gains to 93.42, the daily downtrend that has been in effect since January 6th 2017 remains firmly intact and highlighted the risks of further declines towards the one year lows of 92.55 being a distinct possibility. The declines over the last week materialized into a sustained break of this level and with new yearly lows reached, the risks continue to remain to the downside. We would expect a break and close below the 50% five year Fibonacci retracement of 91.21 to lead to further declines towards 88.23, the 38.2% five year Fibonacci retracement.

Source: Bloomberg

Source: Bloomberg

During his press conference after last week’s ECB Council meeting, ECB President Mario Draghi said very little that could have been considered fresh news to the market. As expected, he communicated that the ECB will set out its plans to end its EUR60bn per month QE stimulus program next month and that the Eurozone economy was gathering strength. At the same time, acknowledgement was paid to the headwinds fanned by a strong Euro and inflation expectations were slightly lowered.

However, despite the lack of any new information, the Euro saw immediate gains following the press conference, and remained bid over the last two days of the week. All things considered, the main reason for EURUSD’s constructive response is probably more attributable to the uncertainty in the US markets and declining US yields, rather than just being a Euro phenomenon.

The latest rise in EURUSD not only reinforces the daily uptrend that has been in effect since 21 December 2016, but increases the risks of immediate short term gains. Having set a new 2017 high on Friday of 1.2092, levels not seen since 2 January 2015, the cross looks likely to test the 50% five year Fibonacci retracement of 1.2167. A break of this level would pave the way for further appreciation towards 1.2598, the 61.8% five year Fibonacci retracement, which remains a possible scenario, if the ECB do not have a “pain threshold” circa the 1.25 level. With this in mind, we have revised our forecasts for EURUSD appropriately (see page 6)

.png) Source: Bloomberg

Source: Bloomberg

Unsurprisingly the JPY was last week’s outperformer, benefitting from safe haven bids amidst widespread uncertainty. Over the course of the week, USDJPY fell to 107.32 from its 110.25 close the previous week, in a move that has been consistent with the daily downtrend that started 19 December 2016. This movement takes the cross back below the 50% one year Fibonacci retracement of 109.38, a level which acted as a support on 4 September 2017. Loses were initially greater before support was found at the weekly low of 107.32, not far from the 38.2% one year Fibonacci retracement of 107.18. The path of least resistance appears to be further softness for this cross and we would look for a sustained break of 107.18 to pave the way for further declines towards 105.

.png) Source: Bloomberg

Source: Bloomberg

GBPUSD closed the week at 1.3200, on the mark of our Q3 forecast for 2017. The move was a symptom of dollar weakness rather than being catalyzed by sterling strength. Indeed last week demonstrated a lack of progress with Brexit negotiations, as well as economic data showing that UK PMI activity slowed slightly in August, while production stagnated in July compared with the previous month. Over the following week, we expect the main guide of GBPUSD to be the Bank of England meeting on Thursday. While monetary policy is expected to remain unchanged, markets will look towards any change in tone in the MPC statement.

The Bank of Canada surprised the market on Wednesday last week after they unexpectedly raised the interest rate by 25bps. Before the meeting, according to the OIS, the markets were pricing in a 43.6% chance of a rate hike. As a result of the surprise, the CAD found itself the subject of aggressive buying, resulting in USDCAD closing the week at 1.2159, levels last seen in June 2015. With the markets currently pricing in a 79.8% chance of an additional hike by year end, CAD is likely to continue to be the subject of further buying interest and technical analysis argues that there is a case for further short term declines in USDCAD. Price movements of the last two weeks showed strong resistance and rejection at the 1.2758 level, the 61.8% five year Fibonacci retracement, followed by a weekly close below the 50% five year Fibonacci retracement of 1.2161. In addition the long term baseline that has been in effect since Q4 2012 was firmly broken. These technical developments make a case for further losses, as a break below 1.20 can trigger a further decline below 1.16.

.png) Source: Bloomberg

Source: Bloomberg

| FX Forecasts - Major | Forwards | |||||||

|

| 8-Sep | Q3 2017 | Q4 2017 | Q1 2018 | Q2 2018 | 3m | 6m | 12m |

| EUR | 1.2036 | 1.2200 | 1.1800 | 1.1500 | 1.1500 | 1.2093 | 1.2155 | 1.2283 |

| JPY | 107.84 | 110.00 | 114.00 | 116.00 | 118.00 | 107.40 | 106.88 | 105.82 |

| CHF | 0.9442 | 0.9600 | 1.0000 | 1.0400 | 1.0400 | 0.9388 | 0.9328 | 0.9211 |

| GBP | 1.3200 | 1.3200 | 1.3500 | 1.3800 | 1.4000 | 1.3237 | 1.3277 | 1.3354 |

| AUD | 0.8060 | 0.7700 | 0.7500 | 0.7200 | 0.7000 | 0.8051 | 0.8041 | 0.8019 |

| NZD | 0.7265 | 0.7100 | 0.6900 | 0.7000 | 0.7100 | 0.7253 | 0.7240 | 0.7216 |

| CAD | 1.2159 | 1.2200 | 1.2400 | 1.2500 | 1.2600 | 1.2155 | 1.2158 | 1.2171 |

| EURGBP | 0.9119 | 0.9242 | 0.8741 | 0.8333 | 0.8214 | 0.9136 | 0.9156 | 0.9199 |

| EURJPY | 129.79 | 134.20 | 134.52 | 133.40 | 135.70 | 129.79 | 129.79 | 129.79 |

| EURCHF | 1.1366 | 1.1712 | 1.1800 | 1.1960 | 1.1960 | 1.1354 | 1.1340 | 1.1316 |

| FX Forecasts - Emerging | Forwards | |||||||

|

| 8-Sep | Q3 2017 | Q4 2017 | Q1 2018 | Q2 2018 | 3m | 6m | 12m |

| SAR | 3.7502 | 3.7500 | 3.7500 | 3.7500 | 3.7500 | 3.7538 | 3.7580 | 3.7703 |

| AED | 3.6730 | 3.6730 | 3.6730 | 3.6730 | 3.6730 | 3.6743 | 3.6760 | -- |

| KWD | 0.3009 | 0.3050 | 0.3050 | 0.3050 | 0.3050 | 0.3035 | 0.3057 | -- |

| OMR | 0.3850 | 0.3850 | 0.3850 | 0.3850 | 0.3850 | 0.3859 | 0.3870 | 0.3908 |

| BHD | 0.3771 | 0.3770 | 0.3770 | 0.3770 | 0.3770 | 0.3776 | 0.3782 | 0.3795 |

| QAR | 3.6950 | 3.6400 | 3.6400 | 3.6400 | 3.6400 | 3.7090 | 3.7160 | 3.7365 |

| EGP | 17.6399 | 17.7500 | 17.5000 | 17.2500 | 17.0000 | -- | -- | -- |

| INR | 63.786 | 65.000 | 65.000 | 66.000 | 66.000 | 64.4600 | 65.0600 | 66.2800 |

| CNY | 6.4944 | 7.0000 | 7.1000 | 7.2000 | 7.4000 | 6.5365 | 6.5675 | 6.6320 |

Click here to download full publication