Recent Search

Popular Searches

The third quarter and second half of the year will begin tomorrow with greater optimism now that U.S.-China trade talks are ‘back on track’, following the bilateral meeting between Presidents Trump and Xi at the G20 meeting in Osaka. This should be a welcome relief for financial markets which have oscillated since talks were suspended in May, with equities pausing, bond yields and the dollar falling and gold having the best month in three years as global uncertainty picked up.

However, a lot of work remains to be done and the implications are not wholly straight forward as the apparent ‘truce’ may still prove to be short lived. Fundamental differences have not gone away, and both the U.S. and China appear to have become more entrenched in their positions the longer negotiations have gone on. The U.S. is demanding fundamental changes to Chinese industrial practices, in effect challenging its sovereignty to provide subsidies to state owned enterprises, and over opening up its domestic market to U.S. goods. China on the other hand looks set to resist any resumption of restrictions on Huawei after some of these have just been eased.

Furthermore, with a more positive trade outlook potentially likely to boost economic sentiment and lift markets, it might also cast doubt on the likelihood of Fed interest rate cuts later this month. The Fed’s hint about lowering interest rates a fortnight ago by Fed Chairman Powell was seen as dependent on whether ‘uncertainties’ would continue to weigh on the economic outlook. With that outlook presumably lifting as a result of the decision to resume trade talks, it may not be necessary to cut rates, especially not as soon as this month which the markets have discounted. Contemplation of this could cause bond yields to hesitate, equities to lose ground and the dollar to recover. This could add further to tensions that are brewing in currency markets between the U.S. and the Eurozone, especially if the ECB proceeds with its own monetary easing in coming months.

At the very least with the trade tensions no longer dominating for the time being, fundamentals can come back into focus and a number of key economic releases are expected this week including U.S. inflation, PMIs, and most important of all employment. A recovery in non-farm payrolls in June is expected after the weak 75k reading in May which might cast further doubt on the inevitability of a July Fed rate cut. The RBA on the other hand is expected to cut rates this week, and the markets will also focus on the OPEC meeting that takes place.

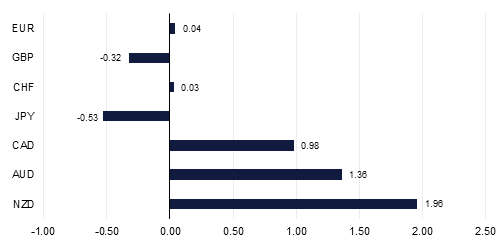

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research