Recent Search

Popular Searches

Last week was a good one for risk assets, with the major equity markets and oil prices steadily advancing on the perception that the global economic downturn might not be as bad as feared. The week started with the publication of the Chinese PMI data for March, which increased above the contraction-expansion breakeven level of 50. In conjunction with a recent increase in Chinese industrial production and retail sales growth, investors saw this as evidence that recent monetary and fiscal stimulus steps are starting to work. U.S. ISM manufacturing activity was also firmer rising to 55.3 in March, while the UK March manufacturing PMI rose to 55.1, a 13-month high and a strong rebound from February. China’s service sector PMI also improved and even Eurozone services PMI data were revised up.

U.S.-China trade talks are continuing and even though it might take more time before a deal is agreed, there is nothing to suggest that the talks will break down. On Brexit too there were signs that a ‘softer’ exit might be on its way, which reassured sterling even though the deadlines for decisions are again ominously close.

A constructive resolution to the U.S.-China trade dispute would remove a key downside risk for global growth that has been in place for over a year now at a time when world trade has slowed and export growth has fallen. The IMF’s Christine Lagarde warned about a ‘delicate moment’ for the global economy last week, and other global bodies like the WTO, OECD and World Bank have issued stark warnings about the outlook. Removing the US-China risk would provide a boost to economic activity and business confidence, helping both the US and Chinese economies and re-opening global supply chains and export links to the benefit of other parts of the world.

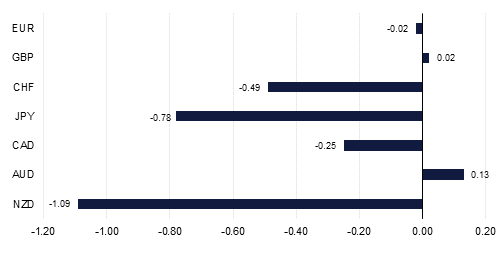

The USD enjoyed a firm week in this risk loving environment as markets embraced the more positive sentiment, which helped interest rates to rise. The bond markets eased up on their previous message of deflation and impending recession, with the yield curve steepening. US 2 and 10-year Treasury yields are now both above the lows posted in March and the effective fed funds rate.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg