Recent Search

Popular Searches

Speculation about the next Fed Chair intensified further last week with John Taylor, a perceived hawk, believed to be leading the race. US Treasury curve steepened with yields on 2yr, 5yr, 10yr and 30yr all closing up at 1.58% (+4bps w/w), 2.02% (+7bps), 2.38% (+8bps) and 2.90% (+8bps) respectively. Still unsettled situation in Germany and on Catalonia front along with ongoing Brexit issues left sovereign yields in Europe following suit with the UST. Yields on 10yr Gilts and Bunds closed higher by 5bps to 1.33% and 6bps to 0.45% respectively.

Oil prices remained stable during the week, benefiting from OPEC’s reiteration that all options to rebalance the oil market were left open and that member state’s compliance with production cut targets were at its highest level. Nevertheless CDS levels on GCC sovereigns had a slight widening bias with international investors continuing to remain cautious about increasing new supply coming out of the GCC sovereign camps. Credit protection costs increased by three bps each on Bahrain to 240 bps and Qatar to 102bps during the week. However, Dubai – the most diversified economy in the GCC region – was an exception with 5yr CDS spreads reducing by 8bps during the week to 120bps.

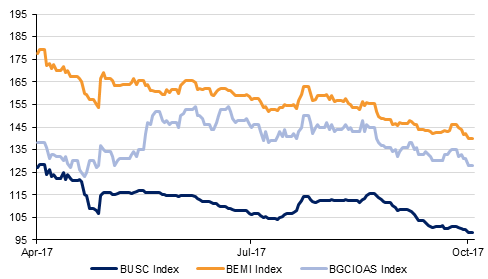

In the GCC cash bond space, average yield on regional Barclays GCC bond index rose 2bps to 3.42% even as credit spreads tightened 4bps to 128bps.

EAPART 20s and EAPART21s were the worst performing bonds in the local universe, as their issuer, EA Partners was downgraded by Fitch to ‘CC’, barely two notches above default. Fitch cited concerns about liquidity pool being insufficient to offset lost contributions from Air Berlin and Alitalia, even if Etihad and other affiliates keep up payments. Yield on EAPART 20s closed 30bps wider at 13% with bond price falling to $85.3.

Qatari banks have been reporting mixed quarterly results. CBQ’s 9m net income was 259m riyals while Ahli Bank of Qatar reported net of 518 million riyals vs 503 million last year. Qatar Islamic Bank reported net income of 610 million riyals vs estimate of 597 million riyals and ahead of last year’s 550 million riyals, however credit spreads on QIB bonds were largely stable with Z-spread on QIB22s closing 1bp lower at 150bps though yield widened 7bps to 3.44%.

News about increasing production at its Block 9 asset in Iraq, saw some sympathy getting attached to Kuwait Energy bonds. Yield on KUWAEI 19s tightened 123bps to 16.92% and bond price rose circa 2points to $88.95 during the week, easily making it one of the best performing bond during the week.

As is expected in times of rising interest rates, high yield bonds from Bahrain (BHRAIN, MUMTAK, INVBNK etc) recorded impressive credit spreads tightening. BHRAIN 22s closed with 8bps tightening in yield to 4.72% on the back of 16bps tightening in Z-spread to 266bps.

In the primary market, while Kuwait and Saudi Arabia government tapped their local currency markets to issue T-bills, the dollar denominated space was dominated by Bahrain’s Oil and Gas Holding issuing new bonds. OILGAS raised $1 billion in 10yr bonds at T+516.2bps which traded up by 2 points on its debut in the secondary market.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Click here to Download Full article