Recent Search

Popular Searches

Financial markets were rattled on Friday by the President Trump’s tweet that the US would impose a 10% tariff on USD 300 bn worth of Chinese imports from 1st September onwards. China in responses is believed to have asked its state owned enterprises to suspend imports of US agricultural products. Though a lot can change in the next month, the chance of further escalation with eventual rise in the tariff rate on all Chinese imports to 25% by early next year seems to be increasing by the day, particularly as China appears to be allowing currency depreciation to counter tariff threat as reflected in the CNY plunging beyond 7.0 to a dollar yesterday..

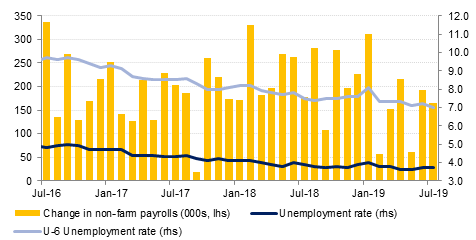

Meanwhile non-farm payroll report on Friday showed addition of 164k new jobs, clearly reflecting trend of slowing job gains albeit still well above the 100k new jobs per month required to maintain the unemployment level at around the 3.7% mark. While job gains in education, healthcare and financial services were solid, employment growth in the services sector was poor. Average hourly earnings grew at 0.3% m/m, indicating annualised gain of around 3.2% even though the six-month average gain in non-farm payrolls of circa 140k is at a seven year low. Also ISM manufacturing index fell again in July to a near-three year low of 51.2 from 51.7 in the previous month albeit still well in the expansionary territory.

Manufacturing in UK shrank for a third month with Markit UK Manufacturing PMI coming in at 48, validating the worst downturn in six years though partly reflecting unwinding of stockpiling at the start of the year before the original March Brexit date. Elsewhere, despite the heightened trade war concerns, Caixin China PMI manufacturing index in July showed a mild rebound from 49.4 in June to 49.9 though Services PMI fell from 52 to 51.6. Overall composite PMI still reflected an improvement to 50.9 from 50.6 in June.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

Fixed Income

US treasuries rallied and the UST yield curve flattened further last week after President Trump’s tweet about tariffs on Chinese imports fuelled fears of a full blown trade war. Yields on 2yr, 5yr, 10yr and 30yrs USTs closed the week at 1.71% (-15bps, w/w), 1.66% (-19bps), 1.85% (-22bps) and 2.38% (-21bps) respectively and are continuing to fall this morning. Sovereign bonds in the Euro area also rallied in response to weakening PMI data. Yield on 10 yr Gilts declined 10bps to 0.55% and those on 10yr Bunds also declined 10bps to -0.50%.

Though result announcements have generally been in line with expectations or better, credit protection costs increased during the week. CDS spread on US IG rose 6bps to 57bps and that on Euro Main increased 7 bps to 54bps.

Dipping oil prices are dampening risk appetite for GCC bonds. Falling USD benchmark yields were adequately balanced off by 18bps increase in credit spreads to 161bps, thereby leaving average yield on Bloomberg Barclays GCC Bond index largely unchanged at 3.40%

Sharjah Islamic Bank is in the primary market with a possible dollar denominated benchmark sized Tier1 sukuk.

FX

The dollar index softened slightly against its major trading partners as case for larger rate cuts builds up amid failing US-China trade talks. The Dollar Index (DXY) closed at 98.07 vs 98.04 earlier in the week.

The yen rose 0.6% against the dollar to 106.01 and the Euro was up 0.1% to 1.1117. GBP remained under pressure, closing the week at 1.2162 vs its opening of 1.2219.

However the main story in the FX markets is probably the steepest fall in CNY that closed at 7.0950 per dollar, possibly as chines regulators become tolerant of weaker currency to counter tariff threats from the US.

Equities

Global equities had one of the worst weeks of 2019 with most indices falling between 0 % - 4% last week in response to escalating trade wars. S&P 500 and Dow Jones closed down by 0.73% and 0.37% respectively and FTSE 100 fell 2.34%. Asian equities closed deep in the red on Friday and have opened weak this morning with Nikkei and Hang Seng trailing down by more than 2% each in early morning trades today.

GCC equities followed the direction of oil prices that fell over 3% to USD 61.89 (Brent futures) last week. Dubai index was down more than a percentage point, led lower by fall in the real estate and construction sector shares. Abu Dhabi index fell 0.96% and Tadawul closed down by 1.26%. Oman managed to stay marginally in the green amid low volumes.

Commodities

Oil prices fell last week thanks to a precipitous decline in response to news that the US will impose more tariffs on Chinese trade from the start of September. Brent futures end the week down almost 2.5% at USD 61.89/b while WTI fell by almost 1% to USD 55.66/b. Commodities generally were caught up in a broad risk off move with industrial metals tanking and only gold gaining among major markets.

Investors split their view on markets last week, adding net length to Brent positions while cutting net length in WTI thanks to more new short positions. Long-dated spreads weakened thanks to the tariff news with Dec spreads in both Brent and WTI showing a narrower backwardation.