Recent Search

Popular Searches

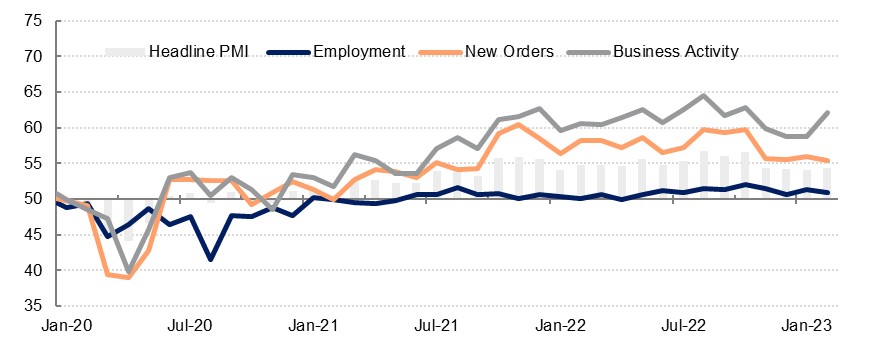

The headline S&P Global PMI survey for the UAE accelerated modestly in February, rising to a three-month high of 54.3, from 54.1 in January. Although this represents a modest slowing in momentum compared with the middle of last year when the PMI averaged 55.0 in Q2 and 56.1 in Q3, it is nevertheless a solid pace of expansion and well above the neutral 50.0 level. In comparison, the PMI surveys of the world’s major economies have been largely contractionary in recent months. We expect non-oil GDP growth to slow to 3.5% this year from an estimated 5.6% in 2022.

Source: S&P Global, Emirates NBD Research

Source: S&P Global, Emirates NBD Research

Drilling down into the survey’s components, output rose at the strongest pace since October, breaking a slowdown that had been in play over the preceding months, with only 2% of respondents noting a decline. New orders growth slowed but remained solid, with ongoing discounting underpinning the expansion – output prices declined for the 10th month running. The orders growth was driven by the domestic market, as new export orders fell for the third month in a row, albeit only marginally and at a far milder pace compared with January. New projects continued to drive new work, and firms were hiring to facilitate this as employment rose again. Hiring has seemingly not been rapid enough to cope with the higher levels of orders however, and backlogs of work continued to expand, if at a slower pace than seen recently.

Firms ramped up their purchases to fulfill new orders and delivery times continued to improve as bottlenecks ease, but firms were forced to pay more to do so as input prices rose once again after staying broadly stable in December and January, with higher raw materials costs driving the increase. Staff costs also rose, but only marginally.

Business optimism improved in February, rising to a four-month high, but it remains lower than 2022 levels, likely reflecting concerns around the global slowdown.

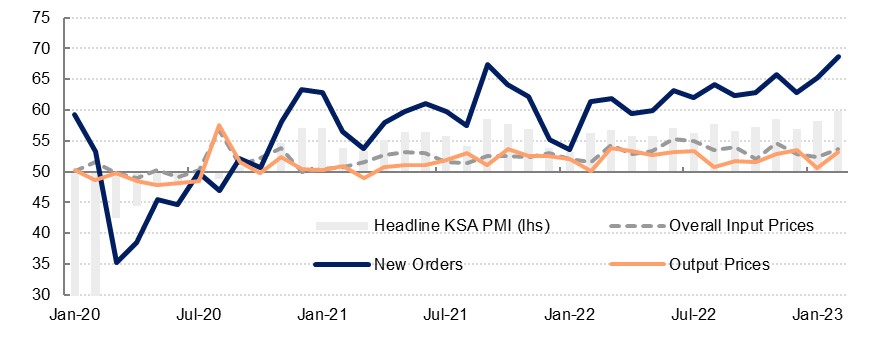

The Riyad Bank Saudi Arabia PMI survey came in at a near eight-year high in February as it rose to 59.8, from 58.2 the previous month. Output was at the highest levels since August 2015, with nearly a third of respondents declaring an increase in February. The outlook for output over the coming months is strong too, as new orders accelerated sharply, supported by price promotions and new clients. New export orders also saw robust growth, with Saudi Arabia’s export market seemingly impervious so far to the global slowdown.

Source: Riyad Bank, Emirates NBD Research

Source: Riyad Bank, Emirates NBD Research

Input prices rose at the fastest pace since November last year, with an acceleration in purchase prices driving the bulk of this as the cost of raw materials headed higher. Staff costs also accelerated, though at a milder rate, with firms from a range of sectors reporting a rise in staff wages compared to January. In contrast to the UAE, firms in Saudi Arabia are passing on their higher input costs to customers, and output prices accelerated again in February after slowing the previous month. The services sector saw the sharpest rise in prices charged.

Despite the robust performance in February, business optimism ticked down modestly compared to the January reading, and it remains below the long-run average. Firms were largely positive, however, and ramped up hiring in order to facilitate expansion plans.

Egypt’s S&P Global PMI survey improved in February, rising to 46.9 from 45.5 in January. Nevertheless, the index remained in contractionary territory for the 27th consecutive month. The private sector in Egypt has come under renewed pressure amidst Egypt’s economic reforms and the related high inflation rate. Output declined at a milder pace than seen in January, as did new orders as inflation weighed on demand. New export orders fell for the second month running, with the cheaper EGP not yet translating into a marked acceleration in exports.

The pound’s depreciation against the USD in recent months continued to feed through to higher prices, although this was at a softer pace, with overall input prices rising at the slowest pace since August. Purchase prices rose at a four-month low, although around a quarter of respondents still noted higher prices, attributing this to the exchange rate. Staff costs also rose as workers sought higher salaries in order to cope with their higher household expenditures.

Business optimism declined in February and was only modestly higher than the series low seen in October, as just 5% of businesses expected an improvement in conditions over the next 12 months. In this low-demand and high-cost environment, businesses cut their purchases once again in February, albeit at the slowest pace since October. Inventories continued to decline as well, and firms also cut headcount for the third month running.

Daniel Richards

Daniel Richards