Recent Search

Popular Searches

The fourth quarter begins with the market’s focus turning to US tax stimulus plans and to the prospect of higher US interest rates. It is in this context that the USD is continuing its recovery which began in the middle of last month, while the EUR, GBP and JPY have all come off their Q3 peaks. Equity markets are benefiting from signs of improved global growth and of expectations that this will persist into 2018, with most regions of the world contributing to it.

Attention is turning back to policy stimulus plans in the US, with the Republican Party there last week proposing a package of sizeable tax cuts. So far the detail of such plans are fairly limited, but the likelihood is that they will entail increasing the fiscal deficit which will provide a further boost to the US economy. However, with the economy already performing strongly (Q2 growth was revised up to 3.1% annualized last week and August durable goods orders showed strength in capital goods orders) the question is what impact this will have on growth and inflation and by extension on the Fed’s monetary policy. Last week Janet Yellen gave an uncharacteristically hawkish speech in which she implied that the Fed is set on raising interest rates again this year, with more to follow in 2018. The Fed appears to believe that the current weakness in core inflation will not last as it is being caused by transitory factors. Accordingly the markets are now pricing a 70% likelihood of a Fed rate hike by the end of this year, up from around 30% only a few weeks ago. This is helping to drive US-Eurozone yield differentials wider to the benefit of the USD over other major currencies.

.png) Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

In the coming days speeches by other Fed officials will be watched closely to see if Yellen’s more hawkish stance will be repeated. To some extent policy communication will overshadow economic data from now on as the data is likely to be impacted by the recent hurricanes and is therefore likely to be an unreliable gauge of the economy’s underlying strength. This applies to the US employment report and to the ISM activity series to be released this week, which are expected to show jobs growth slowing to just 100k and the manufacturing ISM falling back from August’s 58.8 highs. However, any weakness in September is likely to be more than compensated for by strength in subsequent months as recovery efforts boost jobs, construction and manufacturing activity.

The dollar index broke and closed above the resistive trend line of the daily downtrend that has been in effect since April 10 2017. Further evidence for a reversal of the daily downtrend is that the index closed the week above its 50 day moving average (92.878) for the first time since April. Currently sitting at 93.076, while the index remains above this level, the risks remain for further rises with the 23.6% one year Fibonacci retracement of 94.034 being the next likely path.

.png) Source: Bloomberg

Source: Bloomberg

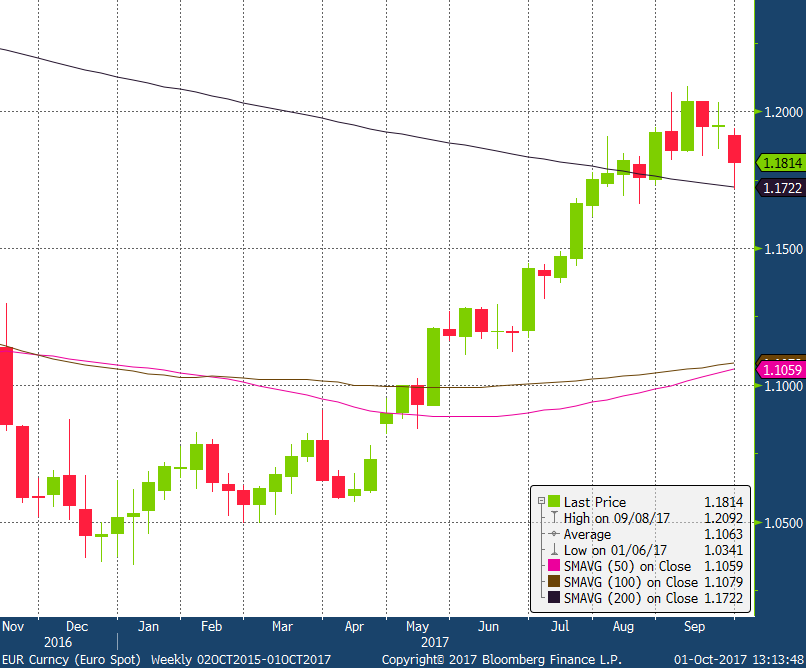

The EUR lost ground last week not only on the back of the resurgent USD but also because of the result of the German election, which returned Chancellor Merkel to office in a weakened position with the far right AFD party gaining ground at the expense of mainstream parties. The process of forming a new coalition will be a long one, with the potential for it to create business uncertainty both within Germany and in the broader EU. Although today’s referendum in Spain’s Catalonia is not an official one, its outcome could also remind markets that populist trends in European countries have not been quelled, maintaining separatist risks down the road. Also dampening EUR sentiment was data from the Eurozone that saw core inflation fall back to 1.1% in September from 1.2% in August, with the headline rate unchanged at 1.5%. Although this outcome is unlikely to divert the ECB away from announcing its tapering of QE later this month, it may cast a doubt on the speed with which interest rates will be raised in the single currency area. Eurozone retail sales data for August, to be released this week, are also expected to be soft, which could also dampen the prospect of any near-term ECB tightening, although unemployment data and final September PMI reports should provide contrasting reassurance about the state of the overall economy.

Last week’s 1.14% decline took the EURUSD below the 50 day moving average (1.1843) and below the supportive baseline of the former daily uptrend for the first time since April 2017. In addition, we saw EURUSD trade as low as 1.1717 before finding strong support near its 200 week moving average (1.1722). A sustained break of this key level in the next week ahead would nullify the former uptrend and indicate further losses lie ahead.

.png) Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

GBP has also given back a significant proportion of its September gains against the USD, on a combination of UK data showing a an unexpected downward revision in y/y GDP growth (to 1.5% from 1.7%), as well as a sharp rise in the UK current account deficit up to 4.6% of GDP from 4.4% in the previous quarter. The GDP downgrade was largely on account of historical revisions, whereas the q/q figure was unrevised at 0.3% but still showed UK growth to be half that of the Eurozone in Q2.

Markets believe this softness to be the beginning of the Brexit effect, although monthly activity data has provided a more positive contrast with the national accounts showing activity indices holding up. PMI data to be released this week should confirm this, although the ongoing Brexit negotiations impasse could threaten to cloud visibility about the medium term outlook. Also complicating the pound’s position is the uncertainty about UK interest rates with BoE Governor Carney indicating that a rate hike can be expected over the near term, whereas past experience leaves the market viewing such comments with caution.

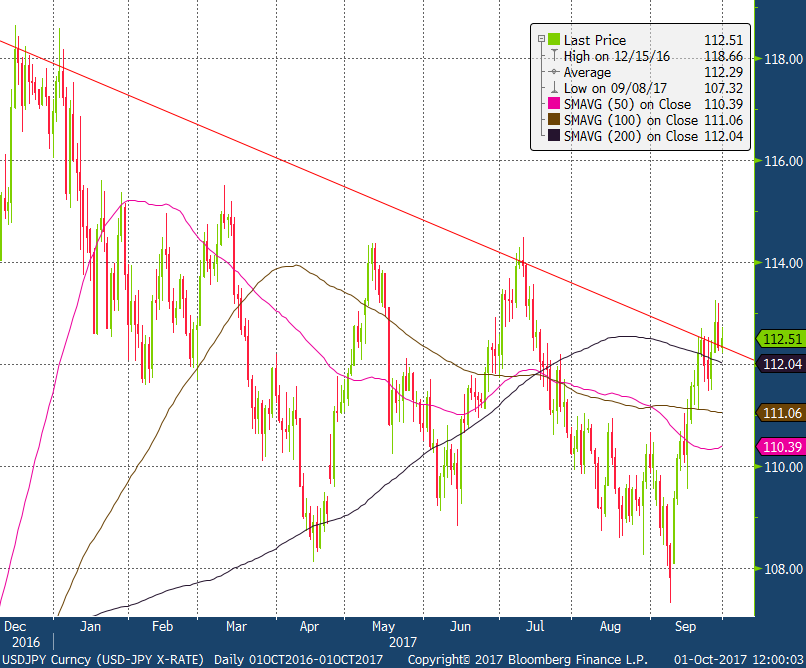

The main focus for the JPY at the start of the week is going to be the release of the Bank of Japan’s Tankan survey, which is expected to confirm the continued expansion of the manufacturing and non-manufacturing sectors in Japan. USDJPY has benefited from the widening in interest rate differentials between the US and Japan in recent days, as well as from the quelling of some of the geopolitical noise related to the US stand-off with North Korea. Meanwhile Japanese core CPI lifted in September to 0.7% y/y from 0.5% in August, and industrial production rose 2.1% m/m in August, but it is still probably a long way off before the BOJ can contemplate normalizing its monetary policy. In the meantime domestic political risk will probably be the main focus with expectations for a straightforward victory for the PM Abe in his snap October 22 election starting to look a little less assured.

Last week’s saw USDJPY gain 0.47% to close at 112.51, taking the price back above the 200 day moving average (112.04), which now acts as a support level. In addition, this movement resulted in a daily close above the resistive capping trend line of the daily downtrend that has been in effect since December 2016. Technically this argues that the short term risks are for further gains and while the price remains above the 61.8% one year Fibonacci retracement of 111.98, further gains towards 114.50 are possible.

Source: Bloomberg

Source: Bloomberg

Otherwise in Asia this week activity will be quiet with China and Korean markets closed for most of the week, and with other markets such as Hong Kong and India also seeing partial holidays. Of note India’s RBI meets on Wednesday and is likely to keep rates steady at 6.0% after a 25bp cut in August as inflation has picked back up even as growth has remained more sluggish.

In the absence of first tier Australian economic data, AUDUSD fell for a third consecutive week, finding strong resistance at the 200 week moving average (0.7946). The week ahead is rich with economic data which is likely to have mixed effects on the currency’s strength. While data is expected to show that the trade surplus widened to AUD 870m in August from AUD 460m the previous month, timelier data released on 30 September 2017 showed signs of a slowdown for their main trading partner. China’s Caixin Manufacturing PMI slowed to 51.0 in September from 51.6 the previous month and missing out on expectations for 51.5.

Furthermore the RBA meets this week to set monetary policy, and while expected to maintain the Cash Rate Target at a record low of 1.50%, the central bank is likely to communicate a neutral outlook to the market. While they will no doubt express concerns over the sharp decline in iron ore prices and currency strength being a headwind to growth, they are also likely to cite the continuing improvement in the labour market and improvements in the global economy.

Source: Bloomberg

Source: Bloomberg