Recent Search

Popular Searches

Reduced anxiety over the US-China trade stand-off is allowing the rally in US equities to continue and the 10-year bond yield to consolidate above 3.0%. The dollar is also reversing the strength that was previously associated with trade tensions, with only USDJPY gaining slightly as it benefits from widening US-Japan yield differentials. Whether the market will remain quite so sanguine over trade remains doubtful however, as the imposition of new tariffs this week appears likely to be only the start of a deteriorating relationship. Markets appear to be taking heart from the fact that the US is ‘only’ imposing 10% tariffs on USD200bn of imports from China, with China responding with tariffs of between 5-10% on USD60bn of US imports. However, China is also likely to pursue ‘qualitative measures’ against US companies operating in China, applying more regulations on them, inspection requirements, and licensing requirements which will add to the burden of doing business in China for many US firms.

The Fed will be in the spotlight this week, with a near 100% certainty that it will raise interest rates by a further 25bps. Thereafter the market believes that another hike will be made in December, and it will be the communication around this that will be most important for the USD’s reaction. Thus the forward guidance will be key, including the dot plot, and whether the Fed continues to characterize policy as accommodative, especially the message conveyed in the press conference by Chairman Jerome Powell.

Meanwhile, pressure on GBP has resumed following the EU summit in Salzburg which saw the expectations of Brexit progress disappointed, with the pound having its largest fall this year in the aftermath. The EU rejected the British prime minister's proposals over trade and over the Irish border, and Theresa May said that the EU has to treat the UK with greater respect. She went on to emphasize that there will not be a second referendum and implied that a ‘no deal Brexit’ was very much an option. Even after GBP’s latest fall, however, the markets are still not pricing such an outcome, implying further downside risks as the tortuous negotiations continue to play out.

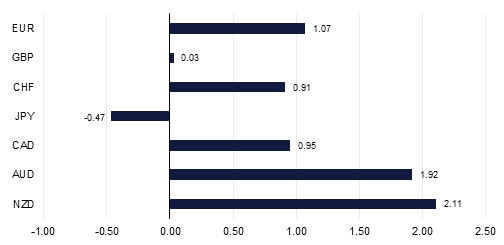

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research